Monitor your business credit with Nav

Business credit monitoring helps you understand how lenders, suppliers and business partners view your business’s financial responsibility. With Nav, you can track the data that matters in real time so you can focus on maintaining good business credit habits.

Why you should monitor business credit

Business credit is a key indicator of your business’s financial health. Whether your business is new or well-established, here’s why monitoring your business credit matters:

1. Strong business credit

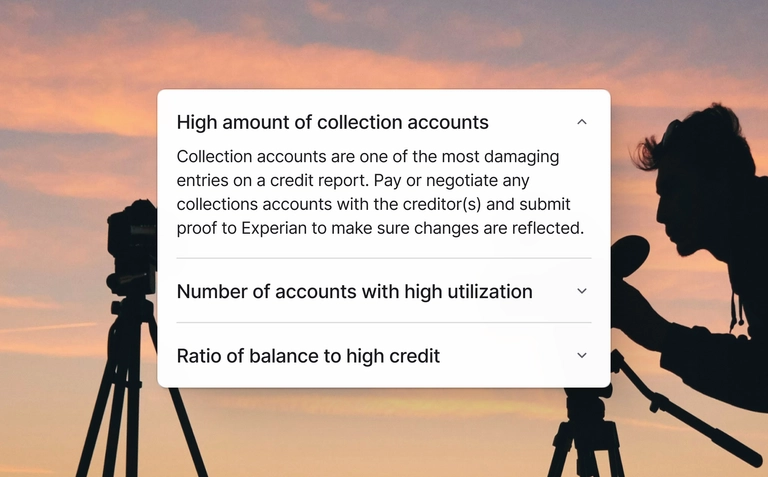

Business credit monitoring helps you understand if your business credit scores are moving in the right direction. Managing your business credit helps you correct mistakes — which happen more often that you might think — that could potentially impact your scores.

2. See what lenders (and others) see

Lenders may use your business credit reports whento decidinge whether to offer your business a small business loan or financing. Vendors use it to determine if your business qualifies for trade credit and on what terms (like net-30). Business insurance companies may also check it.

3. Protect against business identity theft

Business identity theft can be worse than personal identity theft because many business owners don’t learn about it for months or years. While you can’t prevent it completely, monitoring your business credit can help you catch it sooner to minimize the damage.