Small business credit statistics in 2026: Key trends and insights

Gerri Detweiler

Education Consultant, Nav

Summary

- Credit access remains tight. Less than half of small businesses received the full amount of credit the full amount requested.

- Shift toward alternative financing. More small business owners are turning to business credit cards and online lenders instead of traditional bank loans.

- Credit standards continue to tighten. Banks reported stricter lending criteria for the 13th consecutive quarter as of late 2024.

Editorial note: Our top priority is to give you the best financial information for your business. Nav may receive compensation from our partners, but that doesn’t affect our editors’ opinions or recommendations. Our partners cannot pay for favorable reviews. All content is accurate to the best of our knowledge when posted.

Starting or growing a small business often requires money. Even bootstrapped businesses often find they need funding to fuel growth or improve cash flow.

The small business credit statistics here highlight how U.S. small business owners fund their companies, the challenges they face, and why understanding business credit can play a critical role in long-term growth.

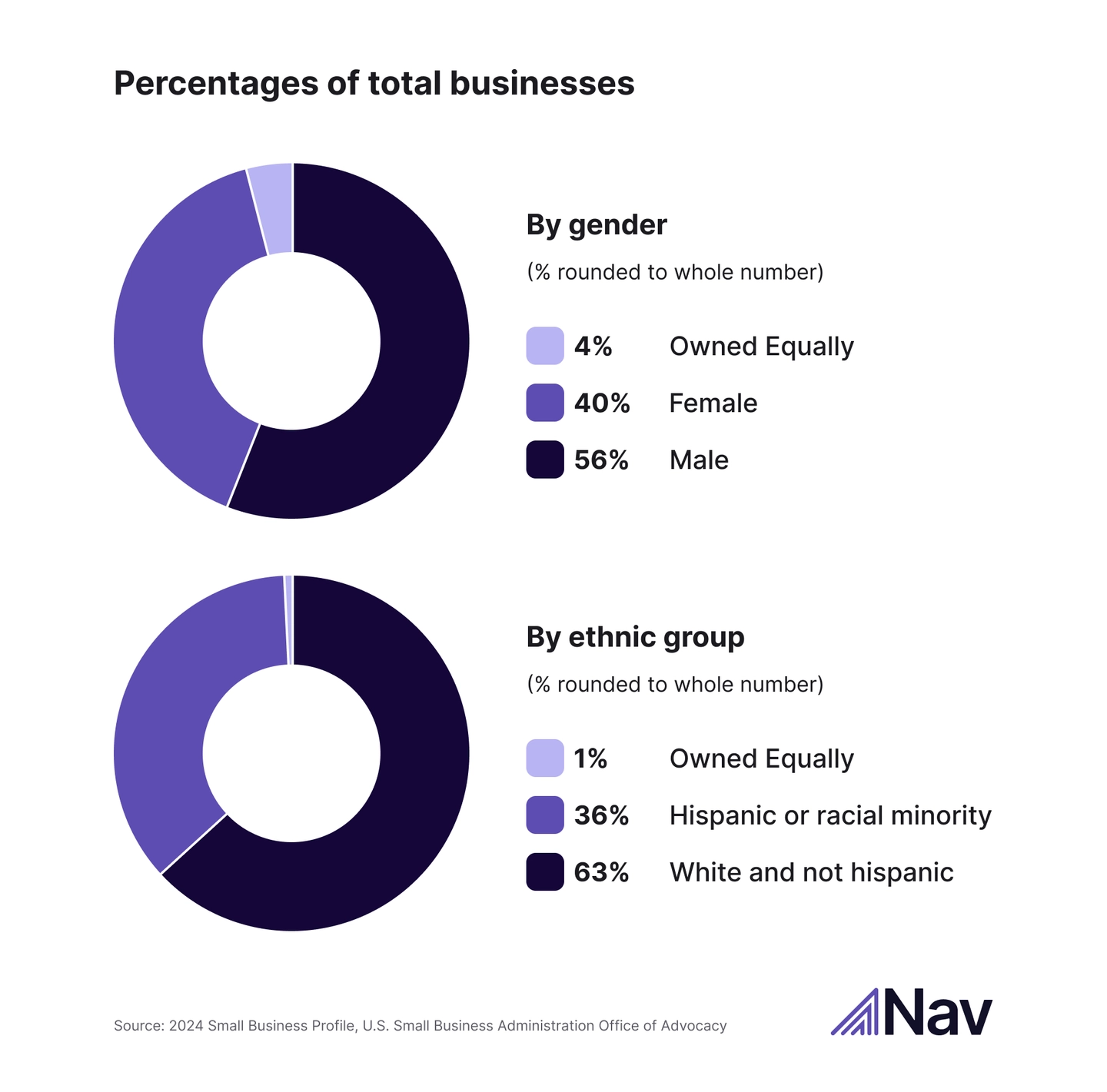

Who owns small businesses in the United States?

Women-owned firms represent about 44% of all small businesses in the U.S., as of 2024 according to the U.S. Small Business Administration Office of Advocacy.

Racial minority-owned firms account for roughly 22%, while Hispanic-owned businesses count for 15.8%, and veteran-owned businesses account for 5.5% (the only category where ownership is higher than workers.)

Small business financing statistics

Let’s look at who’s seeking financing:

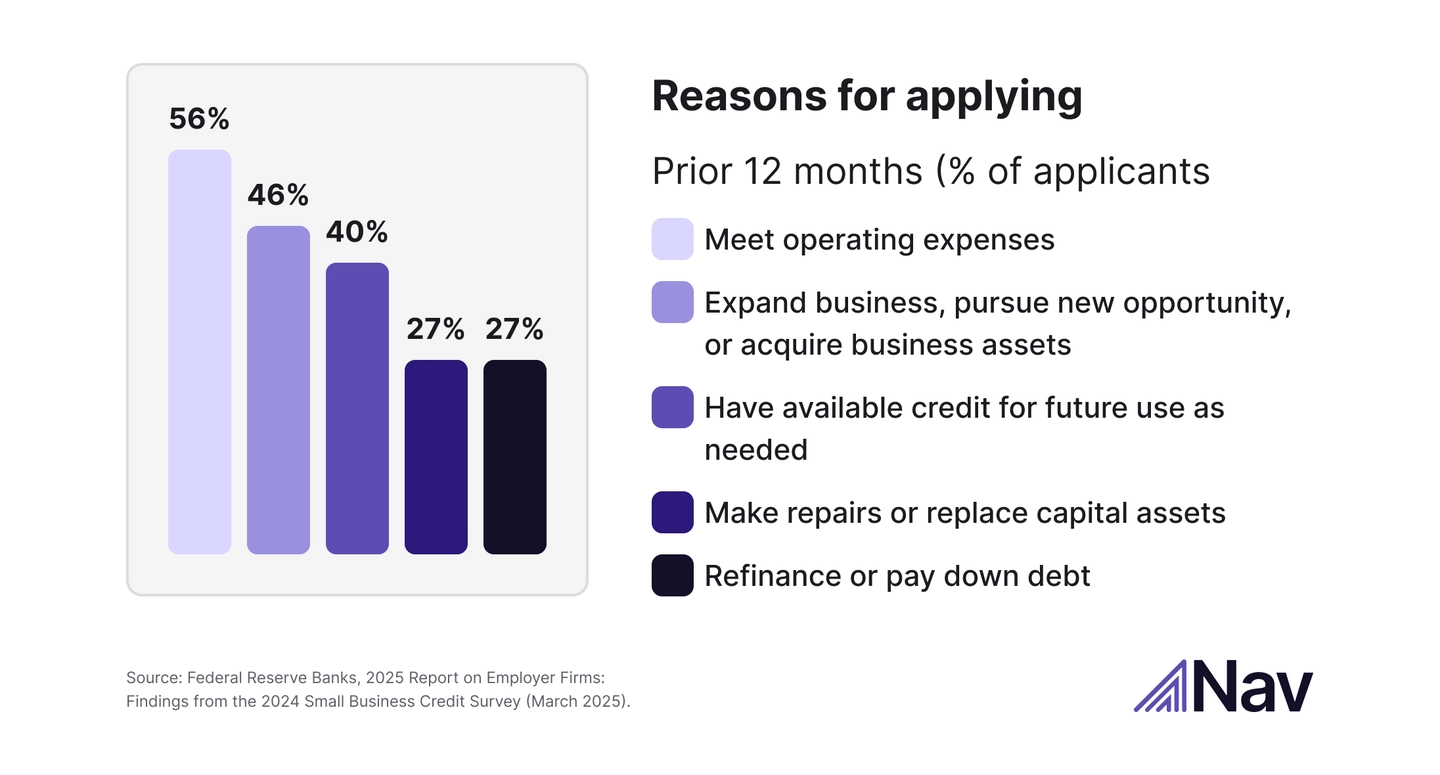

- 59% of employer firms sought new financing in the past 12 months, according to the Federal Reserve’s 2024 Small Business Credit Survey

- Among those, 41% received the full amount requested

- Nearly one-quarter of those were denied all financing

High-credit-risk businesses were more likely to experience funding denials or only partial funding. These businesses also had higher rates of loans from family and friends and equity investments from family and friends.

While commercial lending increased overall in the second quarter of 2025, commercial bankers report a continuing trend of poorer credit quality along with higher credit standards, according to results of a survey by the Federal Reserve Bank of Kansas City.

Sources of small business financing

Traditional bank lending remains important but isn’t dominating the small business financing landscape. Data from the National Bureau of Economic Research show that 55% of small firms used business credit cards in the past twelve months, compared with 26% that took out loans.

Although 2024 Small Business Credit Survey SBCS data from the Federal Reserve shows strong interest for credit cards, loans, and line of credit among businesses of all levels of risk, actual use of these products varies. A larger percentage of business owners (except those in the high credit categories) use credit cards than any other type of financing.

Types of financial regularly used by small businesses

The following chart shows the percentage of employer firms that report they regularly use or carry balances on various types of financing products, segmented by credit risk

Type of financing or credit | Low credit risk | Medium credit Risk | High credit risk |

Credit card | 60% | 68% | 52% |

Loan (includes mortgage) | 52% | 59% | 54% |

Line of credit | 38% | 39% | 27% |

Trade credit | 15% | 18% | 16% |

Lease | 14% | 16% | 15% |

Business does not use external financing | 9% | 7% | 16% |

Source note: Data from the Federal Reserve’s 2024 Small Business Credit Survey. Respondents were asked to identify the types of financing products they regularly use or carry a balance on. Multiple selections were allowed; percentages reflect the most common responses among employer firms.

Small business funding challenges

Access to affordable capital remains one of the most persistent small business funding challenges. In the 2025 Federal Reserve Report on Employer Firns, 75% of employer firms reported rising costs for goods, services, or wages as their top financial obstacle. Managing uneven cash flow and paying operating expenses followed closely behind.

The same survey found that among firms that were denied credit, 41% cited high existing debt as the main reason — up sharply from 22% in 2021.

Medium and high-risk firms were most likely to be approved by online lenders. Yet satisfaction with online lenders was less than 30%, and 75% of online lender applicants reported challenges including high interest rates and unfavorable repayment terms.

Cost of credit

Interest rates are starting to fall for new term loans and lines of credit, according to the Federal Reserve Bank of Kansas City, which is good for small business owners that are looking for this type of financing and are able to secure it.

But banks reported stricter lending criteria for the 13th consecutive quarter as of late 2024. And loan approvals are decreasing along with credit quality, while outstanding small business loans increase.

Startup and nonemployer firm statistics

Firms without employees are the majority of small businesses in the U.S. as of the 2024 SBA Advocacy report. There are more firms that employ 1-19 employees than firms that employ 20 to 499 employees, with the exception of the management of companies and enterprises industry.

The 2025 Report on Nonemployer Firms found that of those surveyed 70% of nonemployer companies used personal funds when faced with financial challenges.

It also found 45% of nonemployer businesses denied funding were denied on the basis of a low credit score. Credit cards were sought at a much higher rate than other financing and credit products mentioned in the nonemployer survey.

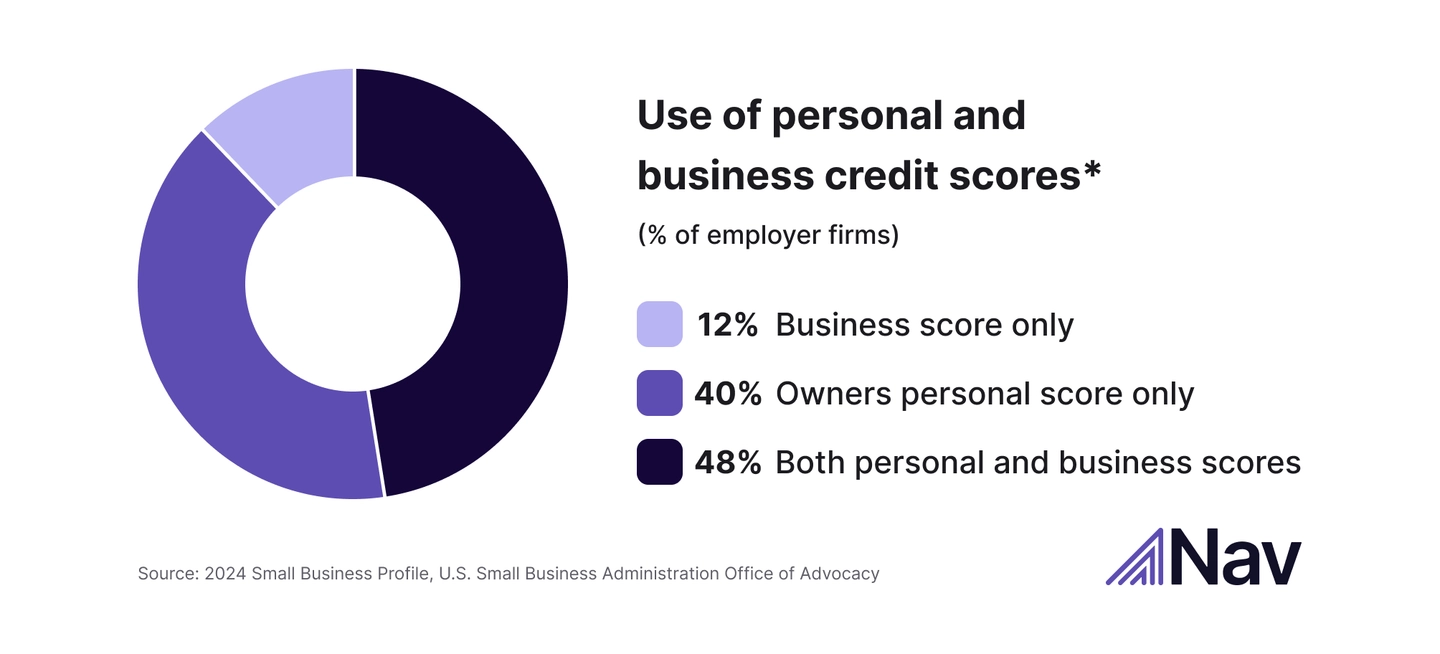

Business and personal credit scores

Both business credit and personal credit remain important for helping business owners access financing, as well as other opportunities for growth.

When asked what type of credit history they used to apply for credit, 12% of business owners said they used only business credit, 40% said they only used personal credit, and 48% said they used both.

Source note: Federal Reserve Small Business Credit Survey 2020, employer firms. This question has not been asked in more recent surveys.

Financial challenges among small employer firms (2021–2023)

Indicator | 2021 Survey | 2022 Survey | 2023 Survey | Trend |

Firms reporting financial challenges | 85% | 94% | 93% | ↑ Widespread but stabilizing |

Firms reporting financial condition as “fair” or “poor” | 59% | 57% | 55% | ↓ Gradual improvement |

Business owners using personal funds to address challenges | 61% | 53% | 53% | ↓ Steady reliance, but declining |

Source: Financing Trends: Employer Firms (2021–2023), Federal Reserve Main Street Metrics Report, 2024

Data sources

This article compiles small business statistics from federal and private research published between 2024 and 2025:

- “2025 Report on Nonemployer Firms: Findings on Hiring Plans from the 2024 Small Business Credit Survey.” 2025. Small Business Credit Survey. Federal Reserve Banks. https://doi.org/10.55350/sbcs-20251014

- SBA Office of Advocacy. (2024). 2024 Small Business Profile [Review of 2024 Small Business Profile]. U.S. Small Business Administration Office of Advocacy. https://advocacy.sba.gov/

- “2025 Report on Employer Firms: Findings from the 2024 Small Business Credit Survey.” 2025. Small Business Credit Survey. Federal Reserve Banks. https://doi.org/10.55350/sbcs-20250327

- “2025 Firms in Focus chartbooks on small business data.” 2025. Small Business Credit Survey. Federal Reserve Banks. https://doi.org/10.55350/sbcs-20250512

- Credit Cards and the Financing of Small Businesses. (2025). NBER. https://www.nber.org/digest/202507/credit-cards-financial-source-small-businesses?utm_source=chatgpt.com&page=1&perPage=50

- Harbour, Daniel , and Connor Jamison. “New Small Business Lending Increases as Most Interest Rates Begin to Decline.” Kansascityfed.org, 25 Sept. 2025, www.kansascityfed.org/surveys/small-business-lending-survey/new-small-business-lending-increases-as-most-interest-rates-begin-to-decline/. Accessed 20 Oct. 2025.

- Harbour, Daniel, and Nicholas Courtney. “Small Business Loan Demand Increases despite Year-Over-Year Decreases in New Small Business Lending and Tightening Credit Standards.” Kansascityfed.org, 27 Mar. 2025, www.kansascityfed.org/surveys/small-business-lending-survey/small-business-loan-demand-increases-despite-year-over-year-decreases-in-new-small-business-lending-and-tightening-credit-standards/.

- SBA Advocacy. FREQUENTLY ASKED QUESTIONS. July 2024. https://advocacy.sba.gov/wp-content/uploads/2024/12/Frequently-Asked-Questions-About-Small-Business_2024-508.pdf

Rate this article

This article currently has 18 ratings with an average of 5 stars.

Gerri Detweiler

Education Consultant, Nav

Gerri Detweiler has spent more than 30 years helping people make sense of credit and financing, with a special focus on helping small business owners. As an Education Consultant for Nav, she guides entrepreneurs in building strong business credit and understanding how it can open doors for growth.

Gerri has answered thousands of credit questions online, written or coauthored six books — including Finance Your Own Business: Get on the Financing Fast Track — and has been interviewed in thousands of media stories as a trusted credit expert. Through her widely syndicated articles, webinars for organizations like SCORE and Small Business Development Centers, as well as educational videos, she makes complex financial topics clear and practical, empowering business owners to take control of their credit and grow healthier companies.