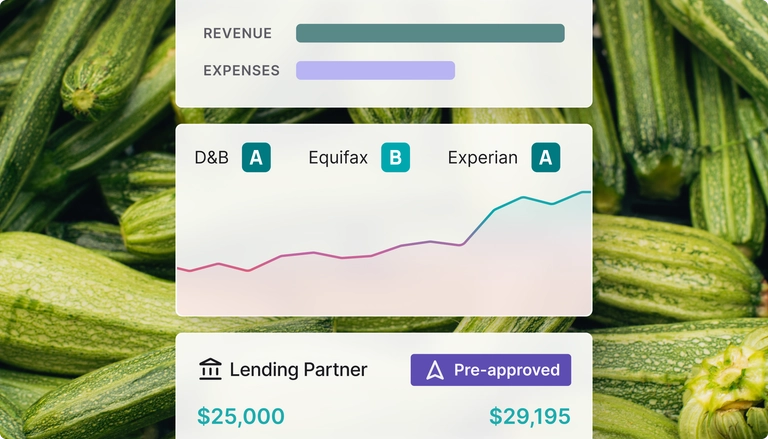

Get your business credit scores

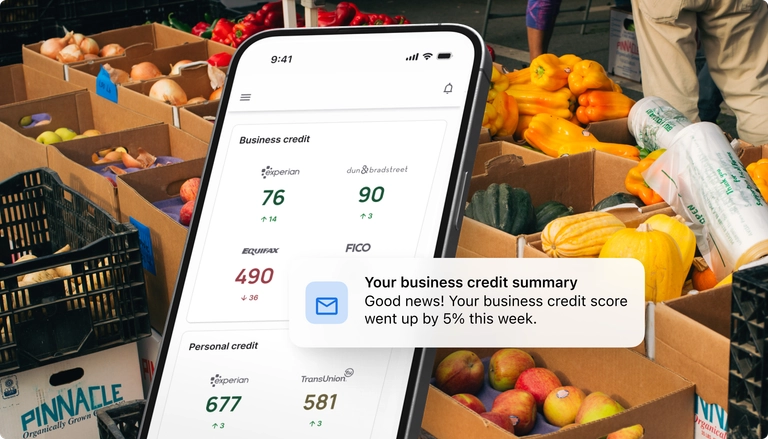

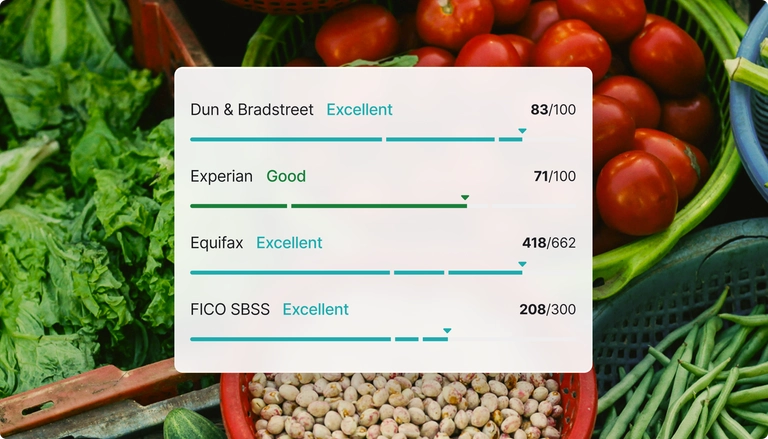

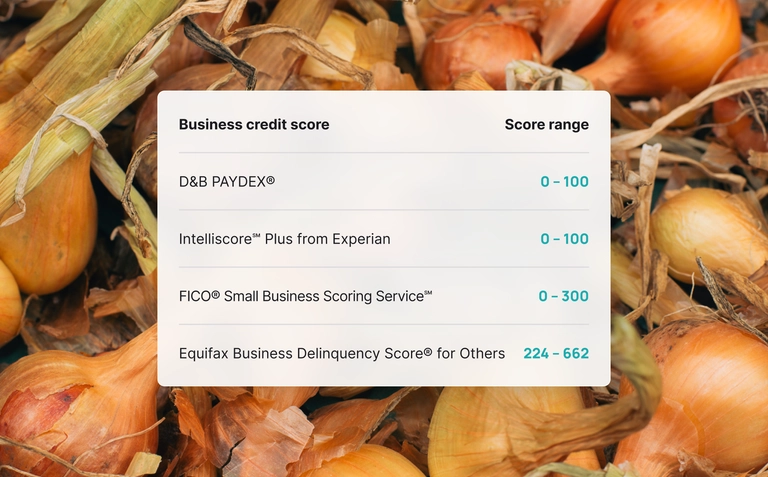

Nav is the only place you can immediately check your business credit across all 3 major bureaus: Experian, Equifax, and Dun & Bradstreet (D&B). To help you plan for tomorrow, check out where you stand today.

How can I get free business credit scores?

With Nav, you can get business credit summaries from Experian, Equifax, and Dun & Bradstreet. These include a grade and a score range to give you an overview of where you stand.

How can I improve my business credit scores?

Building business credit takes time. To set yourself for success, focus on the following:

• Add accounts you already pay to your business credit reports.

• Pay accounts that report on time or early.

• Keep debt under control. If possible, avoid maxing out credit lines.

Nav can help you monitor your business credit and track your scores.

Get your free business credit check

Building a strong business credit score can open up financing opportunities and partnerships that make it easier for you to run and grow your business.

With Nav, you can view your business credit and cash flow all in one place, and get next steps on how to make progress. Sign up today to check your business credit and take control of your financial health.