SBA 504 loan requirements, rates and terms explained

Written byGerri Detweiler

Reviewed by Robin Saks Frankel

Summary

- SBA 504 loans offer low down payments, long-term fixed-rate financing at competitive rates, and the ability to finance large projects.

- Businesses must meet SBA loan requirements to qualify.

- Recent changes will allow eligible businesses to combine a 504 and 7(a) loan for even more SBA-backed funding.

- Learn how these loans can help your business grow.

If you're ready to buy the building your business operates out of, renovate your commercial space, invest in major equipment, or you want to refinance current business debt, the SBA 504 loan program is worth a closer look. It can be an affordable option for real estate and fixed assets, with a competitive fixed interest rate, a low down payment, and large project sizes.

More than 6,700 businesses received 504 loans in FY2025, according to the SBA’s 7(a) and 504 segment report. The average loan size was just over $1.15 million for the SBA-backed portion of the loan.

Not all businesses will qualify due to SBA loan requirements, and it’s not necessarily the fastest source of small business financing. But overall, 504 loans are considered highly competitive small business loans.

This guide covers SBA loan requirements, costs, and steps to qualify so you can make an informed decision for your business.

How SBA 504 loans work

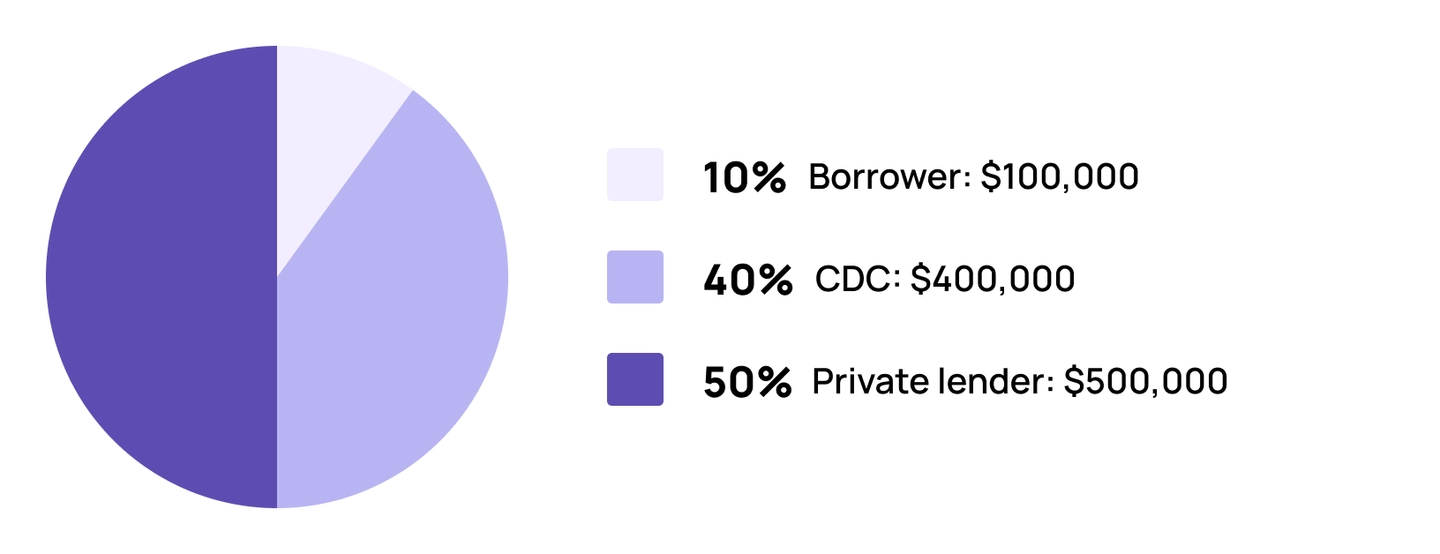

An SBA 504 project doesn’t involve a single loan from a single lender. It's a three-part arrangement between a private lender, a Certified Development Company (CDC), and you — the borrower.

- A Certified Development Company (CDC) provides up to 40% of the financing through a 504 debenture (guaranteed by the SBA)

- A third party lender (often a bank) provides 50% or more of the financing

- The borrower contributes at least 10% of the project cost (not necessarily all in cash)

Here's an example of how a $1 million project would typically break down:

Source | Minimum contribution | Amount |

CDC | 40% | $400,000 |

Private lender | 50% | $500,000 |

Borrower | 10% | $100,000 |

The 10% minimum borrower contribution is one of the program's standout advantages. Most conventional commercial loans require a significantly larger down payment. (And that doesn’t always have to come in the form of cash, as we’ll explain in a moment.)

Some businesses must make larger borrower contributions.

Specifically, businesses that are considered new businesses — operational for less than two years — or special purpose properties, each carry additional requirements. The SBA defines a limited or special purpose property as a “limited-market property with a unique physical design, special construction materials, or a layout that restricts its utility to the specific use for which it was built”. Examples include bowling alleys, hotels or motels, or wineries.

New businesses and limited or special purpose properties must contribute 15%, but if a business is considered both a new business and a special purpose property, then 20% will be required.

Here’s an example of the three party structure for new businesses and special use properties using our earlier $1 million project example:

New borrower | Contribution | Example for a $1 million project |

CDC | 35% (maximum) | $350,000 |

Private lender | 50% | $500,000 |

Borrower | 15% (minimum) | $150,000 |

Special use property | Minimum contribution | Amount |

CDC | 35% (maximum) | $350,000 |

Private lender | 50% | $500,000 |

Borrower | 15% (minimum) | $150,000 |

New borrower and special use property | Minimum contribution | Amount |

CDC | 30% (maximum) | $300,000 |

Private lender | 50% | $500,000 |

Borrower | 20% (minimum) | $200,000 |

The borrower's contribution may not have to be in the form of just cash. Equity in land your business has previously acquired – or in existing land and buildings that will be part of the project — may potentially count toward your contribution. You may even borrow some of the owner portion, depending on your qualifications and the specifics of the project.

SBA 504 loan requirements

In order to qualify for a 504 loan, your business must first qualify under SBA eligibility rules which include business size, type of business, ownership, and financials.

Business eligibility checklist

Your business must:

- Operate as a for-profit business in the United States

- Be owned 100% by U.S. citizens or U.S. nationals with a primary residence in the U.S. As of March 1, 2026, lawful permanent residents no longer qualify.

- Meet SBA small business size standards for your industry*

- Pass a credit elsewhere test — meaning similar financing can't be obtained on reasonable terms from non-federal sources

- Be current on all federal, state, and local taxes, including income taxes, payroll taxes, real estate taxes, and sales taxes**

- Be under a brand in the SBA Franchise Directory if it meets the SBA definition of a franchise

*A business may meet alternative size standards with a tangible net worth of less than $20 million and an average net income of less than $6.5 million after federal income taxes for the two years before your application.

**Delinquencies on federal debt may be considered with an eligible payment plan in place. See the SBA’s 504 50 10 document for more information.

In addition, anyone who owns more than 20% of the business:

- Must be willing to provide an unlimited personal guarantee

- Cannot be currently delinquent on any federal debt (including federal income taxes or federal student loan debt) without a payment plan in place

- May not have caused a prior loss to the government on a federal debt (for example, defaulting on a federal disaster loan to the business)

- Cannot be currently incarcerated, serving a sentence of imprisonment after being found guilty, or under indictment for a felony or any crime involving or relating to financial misconduct or a false statement

Ineligible types of businesses

Some businesses don't qualify for SBA 504 loans regardless of other factors. The following are generally ineligible:

- Businesses engaged in legal gambling

- Pyramid schemes

- Life insurance companies (though life insurance agents may be eligible)

- Private clubs that limit membership for a reason other than capacity

- Businesses primarily involved in lobbying

- Speculative businesses

- Apartment buildings and mobile home parks

Personal guarantee rules

Any individual who owns 20% or more of the business must provide an unlimited personal guarantee. This is a non-negotiable SBA requirement, and it means you're personally responsible for repayment if the business can't make good on the loan.

If a business owner's spouse holds at least 5% ownership and their combined ownership with their partner totals 20% or more, the spouse may also be required to sign a guarantee. Non-owner spouses must sign off on appropriate collateral documents.

Getting one of these loans is a serious commitment. Make sure you understand the agreements you’re signing and what happens if you can’t pay back the loan.

Credit score requirements

CDCs are required to obtain and review credit reports for the small business applying for the loan, all owners who are guarantors and affiliates who are guarantors. They must review the applicant’s credit history, including a review of business credit reports and any experience the CDC may have with the applicant.

The SBA doesn't set a minimum personal credit score for 504 loans. In practice, though, CDC lenders often look for a personal credit score of approximately 680 or higher.

Qualifying uses and restrictions

SBA 504 loans are built for businesses that need real estate or fixed assets they'll actively use in their own operations. There are clear rules about what qualifies — and what doesn't. If you're planning to buy or renovate a property primarily to lease it to others, this program is not available to you, regardless of your other qualifications.

Approved project types

504 loans can be used to:

- Acquire land (by purchase or lease) as part of an eligible project

- Improve a site, including grading, streets, parking lots, and landscaping; up to 5% may go toward community improvements like curbs and sidewalks

- Purchase one or more existing buildings

- Convert, expand, or renovate one or more existing buildings

- Construct one or more new buildings

- Acquire and install fixed assets (by purchase or lease)

- Refinance certain outstanding business debts

- Finance a lender's Other Real Estate Owned (OREO)

A 504 loan may also be used to refinance existing commercial property loans, including other SBA loans, for owner-occupied properties. You may even be able to refinance and take cash out (up to 20% of the appraised value), which some businesses have used to pull out funds for working capital or growth at the same time as locking in a fixed, long-term rate.

One thing to watch if you rent your location: If you're using a 504 loan to acquire fixed assets and those assets are tied to leased space, an assignment of lease and a landlord's waiver may be required. This can create complications or slow the process, as some landlords may not want to do that, so flag it early with your CDC lender.

Occupancy requirements

The property you're financing must be used primarily by your own business. This program isn’t designed to finance investment real estate or rental properties.

504 occupancy requirements

Project type | Minimum initial occupancy | Ramp-up requirement |

Existing building | 51% | None |

New construction | 60% | Must reach 80% within 10 years |

For existing buildings, your business must occupy at least 51% of the space. For new construction, you may start at 60%, but you must reach 80% owner occupancy within ten years — leaving room to lease a portion of the building while you grow into it.

It’s worth noting that hotels, motels, RV parks, marinas, campgrounds, or similar types of businesses are eligible if at least half of the business’s revenue for the prior year comes from stays of 30 days or less. Barber shops, beauty salons, and similar businesses are eligible whether or not they have employees or use contractors to provide services.

Ineligible uses

504 loan funds may not be used for:

- Investments in real or personal property acquired and held primarily for sale, lease, or investment

- Properties that will be primarily rented out rather than used for your own business operations

- Working capital or operating expenses

- Speculative real estate

Interest rates and fees

The fixed-rate structure of the 504 program is one of its most valuable features. The CDC portion of your loan locks in a rate at closing that doesn't change over time. This gives you predictable payments for 10, 20, or 25 years for that portion of the financing.

Current rate snapshot

Verify current rates with your CDC lender before applying

Term | Standard CDC rate | Refi CDC rate | Manufacturers (25-yr) |

10-year | 6.19% | 6.19% | — |

20-year | 6.20% | 6.20% | — |

25-year | 6.17% | 6.17% | 5.71% (accurate as of June 2026)* |

*The lower manufacturer rates reflect the FY2026 fee waiver for NAICS 31–33, and that rates are subject to change in future fiscal years

Rates are set monthly through a debenture auction and are subject to change before your loan closes.

CDC debenture rate

A 504 loan is funded through a debenture – an obligation issued by a CDC and guaranteed 100% by SBA, the proceeds of which are used to fund a 504 loan. In other words, it’s the funding mechanism for the SBA/CDC portion of the loan.

The interest rate on the CDC portion of your loan is determined at the time the debentures are sold to investors. It's tied to market conditions for long-term government debt and typically reflects 10-year U.S. Treasury yields, with fees from the CDC, the SBA, and the central servicing agent built into the effective rate.

Because the rate is fixed at closing for the full term, a 504 loan gives you certainty that variable-rate financing can't match. If you close in a favorable rate environment, that rate stays with you for the life of the loan.

Third-party lender rate

The private lender covering the (up to) 50% portion of the project sets its own rate, negotiated separately. This portion will vary based on your qualifications, industry, and market conditions at the time you apply.

Your CDC lender can often connect you with private lenders who have experience with businesses in similar situations, which can help you find competitive terms on that portion of the financing.

Typical closing costs

For FY2026 (loans approved Oct. 1, 2025 through Sept. 30, 2026), SBA fees are as follows:

- Upfront guaranty fee: 0.50% (50 basis points)

- Annual service fee: 0.209% (20.9 basis points) of the outstanding loan balance

For loans under the 504 Debt Refinance without Expansion Program, the annual service fee is slightly higher at 0.2115% (21.15 basis points).

Manufacturers — businesses with a primary NAICS code in sectors 31 through 33 — have both the upfront guaranty fee and the annual service fee waived for FY2026.

Beyond SBA fees, you'll also encounter processing fees, closing fees, and an underwriter's fee from the lender. These are generally reasonable relative to the size of the loan, and they're typically rolled into the loan — so you repay them over time rather than out of pocket at closing.

Repayment terms and prepayment

10-, 20-, 25-year amortization

SBA 504 loans are available in three term lengths: 10, 20, or 25 years. These longer terms keep monthly payments manageable for large real estate and equipment purchases. The term you're offered depends on what type of asset is being financed. The goal is to match the length of the loan to the useful life of what’s being financed.

Prepayment penalty window

You can pay off a 504 loan early if your situation changes, but there's a cost if you do it in the first half of the loan term. A prepayment premium applies only during the first half of the term, up to a total of ten years, even for 25-year loans. It goes down slightly each year. There is no prepayment penalty in the second half.

The premium follows a specific formula your lender can walk you through. The practical rule: The earlier you pay it off, the higher the cost. Once you've passed the midpoint of your term, early payoff comes with no penalty.

Step-by-step application process

Here’s an overview of the process for getting a 504 loan.

Find a CDC lender

You can't apply for a 504 loan directly through SBA.gov. Unlike SBA Disaster Loans, this isn't a direct government loan. Instead, you work through a Certified Development Company (CDC) authorized to make 504 loans.

CDCs are nonprofit organizations certified and regulated by the SBA, focused on economic development in their communities. Look for with one a lot of experience in 504 loans; the more experience they have, the stronger their lender networks and the more smoothly the process is likely to go.

Assemble your 504 package

The documentation package for a 504 loan is comprehensive. Your lender will evaluate:

- A pro forma balance sheet that includes loan proceeds, how they'll be used, and any adjustments such as your required borrower contribution

- Historical income statements and business tax returns for existing businesses (two years if using the Alternative Size Standard, or three years if using the Industry Size Standard)

- At least two years of financial projections

- A ratio analysis of your financial statements compared to industry averages

- A description of your management team's relevant experience in the business

- A collateral analysis, including valuation and lien position

- Personal credit history for all owners and guarantors

- Business credit history

The lender must verify the applicant is current on all federal, state, and local taxes at the time of application. If your business is delinquent on business income taxes, you may still be eligible if you have an approved payment arrangement in place with the IRS and are making those payments on time.

Timeline from prequalify to closing

Plan on 30 to 90 days from application to loan closing. The review process is thorough, and this program isn't designed for speed. If you need fast funding to cover operating expenses, respond to an urgent opportunity, or bridge a cash flow gap, you may need to look for other fast small business financing options.

Once you've found your CDC lender and submitted your documentation, your CDC manages most of the process. They guide the application through SBA review and serve as your partner on the loan.

SBA 504 vs, 7(a) comparison

The 7(a) and 504 loans are the two most popular SBA loan programs. They both offer competitive advantages. Here’s a simple side-by-side comparison:

SBA 504 vs 7(a) comparison

Feature | SBA 504 | SBA 7(a) |

Primary use | Real estate, fixed assets, certain debt refinancing | Working capital, inventory, equipment, real estate, debt refinancing |

Max loan amount | $5M with higher limits for manufacturers and green initiatives** | $5M |

Owner contribution/equity injection | 10%–20% | 10% for some businesses*** |

Interest rate | Fixed (CDC portion) | Variable or fixed |

Repayment terms | 10, 20, or 25 years | Up to 25 years for real estate; 10 years for working capital or inventory; 10 - 15 years for furniture or equipment |

Best for | Owner-occupied property purchases, equipment, refinancing | Flexible business needs |

** Manufacturers may be eligible for up to $5.5 million with no limit to the number of projects, while green initiatives may be eligible for $5.5 million per project, up to a total of $16.5 million.

*** Startups and change in ownership require a 10% equity injection. For others, there may be some flexibility.

You may want to choose the 504 program when you're buying or improving owner-occupied real estate or major fixed assets and want a competitive fixed rate with a low down payment.

The 7(a) is the better choice when you need working capital, or need more flexibility in how you use the funds. If you need a small amount of financing or you're in the early stages of building your business, a SBA Microloan (up to $50,000) or SBA Small loan (up to $350,000) may be the better choice.

One thing worth knowing: as of July 4, 2026, qualified borrowers can access up to $10 million in combined SBA financing by pairing a 504 loan with a 7(a) loan. The individual 504 program cap of $5 million (or $5.5 million for manufacturers) still applies, but if you need both long-term real estate financing and working capital, you may now be able to use both programs together. Under this structure, the 7(a) loan must be obtained first.

Here are the top ten 504 lenders for FY2025 based on the number of approved loans:

Lender name | Approval Count |

The Mortgage Capital Development Corporation (CA) (TMC Financing) | 548 |

Florida Business Development Corporation (FL) | 418 |

Florida First Capital Finance Corporation, Inc. (FL) | 349 |

California Statewide Certified Development Corporation (CA) | 308 |

Business Finance Capital (CA) | 303 |

Mountain West Small Business Finance (UT) | 264 |

Empire State Certified Development Corporation dba Pursuit CDC (NY) | 230 |

Granite State Economic Development Corporation (NH) | 194 |

WBD, Inc. (WI) | 184 |

Small Business Growth Corporation (IL) | 178 |

SBA 504 loan: Quick qualification check

Ask yourself the following questions to see if this program may be a fit for your business:

- Is your business a for-profit company?

Nonprofits, passive investment companies, and speculative businesses are not eligible. - Is your business located and operating in the U.S.?

The business must be U.S.-based. The project property must also be located in the U.S. - Are all owners U.S. citizens or U.S. nationals with their principal residence in the U.S.?

As of March 1, 2026, 100% of all direct and indirect owners must meet this requirement. Lawful permanent residents are not eligible. - Will your business occupy at least 51% of the property being financed?

For existing buildings the applicant must occupy at least 51% of the property. New construction requires 60% initial occupancy, reaching 80% within 10 years. Investment or rental properties do not qualify. - Has your business been operating for more than 2 years?

Businesses operating two years or less are considered "new businesses" and require a higher down payment (15–20% vs. the standard 10%). - Is your business current on all federal, state, and local taxes?

Tax delinquency — including unpaid federal tax liens not in a repayment plan — may disqualify your business

Six "yes" answers? You may be a strong candidate for one of these loans. Connect with a CDC lender to review your full application. Any "no" answer likely disqualifies your application, except for the two-year question, which affects your required down payment only.