How to check if a loan company is legitimate and avoid scams

Written byGerri Detweiler

Reviewed by Robin Saks Frankel

Summary

- Business owners with bad credit or in urgent need of a loan are prime targets for scammers, and AI-powered tools can make those scams harder to detect.

- Learn the specific steps to verify loan company legitimacy before sharing personal or business information.

- Know the warning signs of business loan scams — from advance fee requests to guaranteed approval offers — so you can walk away before losing money.

- If you've been scammed, act quickly to help prevent further damage.

Small business owners often need capital to start or grow their businesses. But startups, businesses with bad credit, and those facing cash flow problems frequently struggle to find funding — and scammers know it. They target entrepreneurs at their most vulnerable, stealing money that should be going into the business.

Nav works with small business owners across the country. Some small business owners have shared with us how loan scams often target businesses with thin or no credit file — making business credit monitoring a valuable early-warning tool for spotting suspicious activity before it becomes a bigger problem.

The threat is growing. Financial fraud against small businesses has increased by 70% since the start of the pandemic, according to the March 2025 Experian Commercial Pulse Report. Meanwhile, 31% of small businesses have encountered fraudulent lenders or scams during the lending process, and AI-driven scams are projected to cause $40 billion in losses by 2027, according to the report.

"With the broad adoption of AI, in addition to business email compromise, unsuspecting employees are wiring millions of dollars to criminals based upon deepfake audio and deepfake videos," says Adam Levin, author of Swiped: How to Protect Yourself In a World Full of Scammers, Phishers, and Identity Thieves.

Getting scammed is awful, no matter who falls victim. But it can be uniquely devastating for small business owners.

Business loans and payment methods don't always carry the same protections as consumer loans, leaving victims with little or no recourse. Taking a few minutes to verify loan company legitimacy before you apply can save you from losing money — and potentially your business.

Case study: business loan scam calls

I’ve received phone calls almost every day for the last several months stating that my business loan application is almost approved. These messages have told me I have supposedly been “approved for” a business loan ranging from $162,000 to $239,000.

I have not applied for any small business loans during this time period, but since I was a victim of both business and personal identity theft several years ago, I take calls like this seriously.

When I asked details about the name of the company calling, the person on the other end of the call offers vague answers about a “direct lender”. When I ask if she represents a loan broker, she hangs up.

How to verify a loan company

There are three main problems when it comes to verifying small business financing offers:

- Not all states require all business lenders or financing companies to be licensed or registered.

- Most states don’t regulate commercial loan brokers (individuals or companies that match borrowers to financing).

- Scammers will sometimes impersonate legitimate companies to gain your trust.

Still, if you are going to provide a company with sensitive personal or business information, make sure you are working with a legitimate business that will help protect your information, not exploit it.

The steps below can help you separate legitimate business lenders from fraudulent ones.

Verify the company website and domain

Before you enter any information on an online lender's website, do a basic internet search for the company name. You can also check the "News" tab in Google to see if the company has appeared in news articles.

Don't assume a professional-looking website means the company is real. Scammers often impersonate legitimate companies, and can build attractive websites to gain your trust. This is becoming even easier with AI tools that can create attractive websites quickly.

Go directly to the lender or loan company’s website and look for these things:

- A padlock icon in the browser's address bar and "https://" is used to indicate a site is secure. Click the padlock to check that the security certificate is current.

- A legitimate physical address and working customer service contact information.

- A domain registration date. You can look up when a website was registered using an online lookup tool such as the ICANN lookup tool. A brand-new domain — especially one registered in the past year — is often a red flag.

Never enter personal or sensitive business information on a website that is not secure.

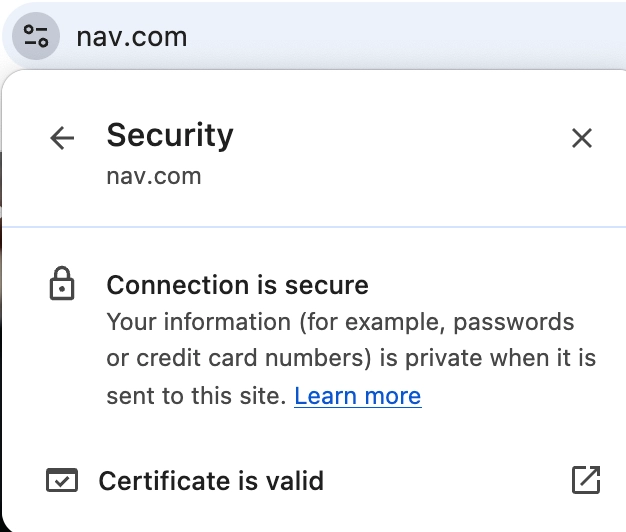

Here’s an example that shows a site that is secure with a valid security certificate. This is a screenshot from the Nav.com website using the Google chrome browser taken February 21, 2026.

In this example, when I clicked on the security symbol to the left of the website address (URL), a box popped up with the words “connection is secure”. I then clicked on that message to get the message you see above. It says the “Connection is secure” and the “Certificate is valid”. I can then click on the box with the arrow to the right of the words certificate is valid to learn more about when the certificate was issued and when it expires.

Check for phishing indicators

If a lender reached out by email, look closely before you respond or click anything. Scammers can create emails that look almost identical to those from legitimate banks and lenders.

Check for misspelled words in the email body or the email address itself. Hover over the sender's email address to see if it matches the company's official domain. If the email address ends in a generic domain like @gmail.com or @hotmail.com, there’s a serious risk that you are dealing with a scammer — even if the sender's name looks official.

Here are tips from the FTC about how to spot and avoid phishing scams.

Confirm physical business location

Look for a physical address on the lender's website, then search it on Google Maps. You may be surprised how many of these searches lead to a residential home or a completely unrelated business.

A P.O. Box as the only address provided doesn’t necessarily mean the company is not legitimate, but it should prompt you to do more research.

You may also want to do a reverse phone number search online. (Most of these sites are trying to sell paid services, though, so you have to decide whether it’s worth it.)

Review Better Business Bureau ratings

Check the Better Business Bureau website (BBB.org) to research the company. In many cases, you can also read customer reviews that give you a clearer picture of what working with the lender is actually like. The free BBB ScamTracker database lets you search for potential scams. Not every fraudulent company will appear, but it's a fast, free check worth doing.

Trustpilot is another option, though smaller or newer companies may not have reviews there.

Verify state and federal licensing

Lenders are typically required by law to register with state agencies before doing business. Contact your state attorney general's office — they can direct you to the agency that regulates lenders and loan brokers in your state.

With loan brokers, it can be tougher to verify their qualifications. In most states, there are no qualifications or licensing requirements for business loan brokers. Here’s a guide to state-by-state requirements for commercial financing. (The word commercial here refers here to lending to a business, rather than a consumer.)

Assess communication tactics

How a lender communicates with you says a lot. Most reputable financial institutions do not cold-call non-customers and immediately request sensitive information.

If you receive an unexpected call from someone claiming to be from a bank or lending company, don't provide information over the phone. Hang up and call the company directly using the contact information on their official website.

Legitimate lenders want your business, but they shouldn't be desperate for it. If you feel pressured to make a decision before you've had time to review the terms, step back.

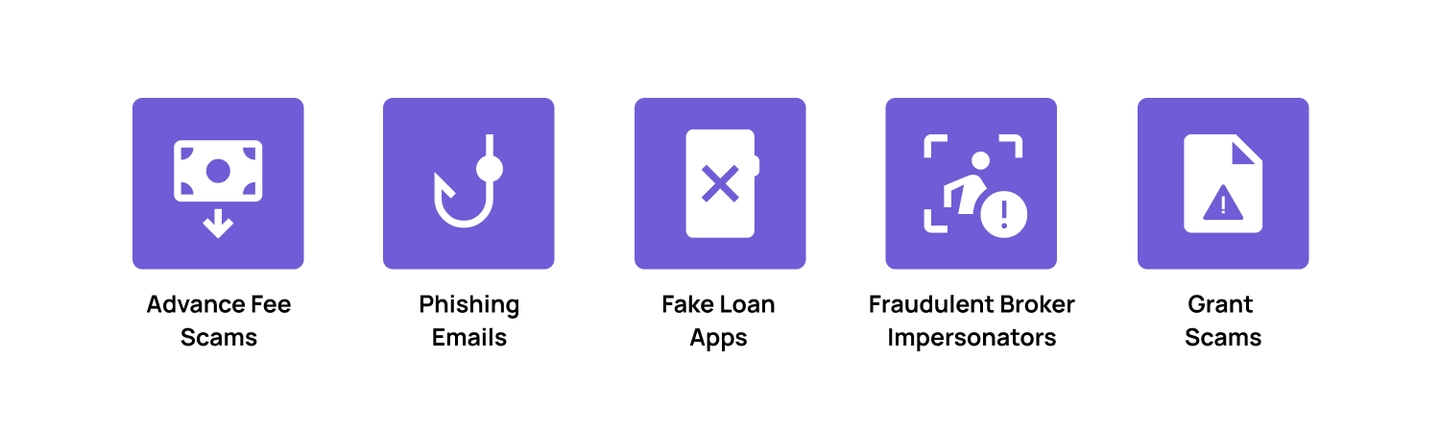

Common types of business loan scams

Knowing how scammers operate is your first line of defense. Here are the most common loan scams targeting small business owners.

Advance fee scams

These scammers promise you a loan but require money upfront. They may call it "insurance" for the loan, a "good faith" payment, or processing and application fees. Once you pay, they disappear — or keep asking for more.

They almost always request payment through methods that are hard to trace or reverse: gift cards, prepaid debit cards, wire transfers or money transfers through a service like Western Union, or peer-to-peer payment services like Venmo or Zelle. If a lender asks for any payment before disbursing funds, find another lender.

Phishing and identity theft scams

Here, someone poses as a lender to steal your sensitive information, such as your Social Security number, bank account details, employer identification number (EIN), or credit card numbers. Once they have that data, they can open new accounts in your name, drain existing accounts, or sell your information on the dark web.

As the FTC warns, identity thieves "can take out loans or obtain credit cards and even driver's licenses in your name" and cause financial damage that can take years to repair.

AI is making these scams more convincing. Deepfake audio and video technology can now be used to impersonate real bank representatives or business contacts, making it extremely difficult to tell a legitimate call from a fraudulent one.

More than eight billion records were found on the dark web in 2024, notes Experian. That’s more than double the amount reported in 2022, giving scammers an enormous pool of data to draw from.

TrendMicro’s Trend Research warns that “cybercriminals are using AI to supercharge scam operations, making them easier to run and harder to detect.”

A business credit monitoring service like Nav can alert you to unauthorized inquiries - often the first warning sign.

Business grant scams

Business owners often search for small business grants, which — unlike loans — don't need to be repaid. Scammers exploit this appeal by claiming you've been awarded a grant, often for thousands of dollars, and then ask you to pay a fee to receive it. There is no grant, and your money is gone.

Be very wary of any grant programs that require upfront fees to apply.

The U.S. federal government does not award grants to start a brand new business and will never contact business owners to ask for money if you haven't applied. While you can hire a professional grant writer, you don’t need to pay to apply for government grants. Learn how to spot government grant scams.

Fraudulent loan brokers and impersonators

These scammers pose as loan brokers and sometimes even impersonate legitimate, well-known lenders or brokers. They charge upfront fees to "find" you a loan, then either disappear or continue asking for more money without ever securing real financing. Before working with any broker, verify their credentials and check whether they are properly licensed in your state (if required).

Keep in mind that in some states it is difficult to identify fraudulent brokers.

Fake loan apps and websites

Fake loan apps are built to collect personal information and steal money from people searching for loans. When discovered, these apps may be removed from app stores, but scammers often create new versions. Be very careful about the apps you download and the permissions you grant them.

Trend Micro ScamCheck's Scam Check app will analyze phone numbers, URLs, emails, text messages, and screenshots to help identify scams. No tool is 100% effective, but it can provide another layer of support to help you avoid getting ripped off.

Red flags that signal a loan scam

By the time you notice pressure or discomfort in a lending situation, something is usually wrong. Here are the warning signs to watch for.

Upfront payment pressure

This is the most common loan fraud red flag. Legitimate lenders typically don't ask for money before disbursing your loan. Some loans do include fees — origination fees, document preparation fees — but these are almost always deducted from your loan proceeds after approval, not paid out of pocket before you receive any funding. Be especially wary if a lender insists on payment through wire transfers, gift cards, or prepaid cards.

Unsecured requests for sensitive information

Loan applications legitimately require some sensitive data — your Social Security number or employer identification number for credit checks, for example. But before you provide that information, verify that you're dealing with a reputable company and that the website is secure.

Look for the padlock icon and "https://" in the browser address bar. Research the lender independently before submitting anything.

Guaranteed approval without credit checks

Most legitimate lenders have minimum creditworthiness standards. While there are some financing options for business owners with poor credit, these come with higher costs and will likely require you to verify your business income.

Promises of easy approval regardless of credit history — especially if paired with pressure to pay fees upfront — are most often a sign of a scam.

Many traditional small business lenders evaluate factors such as good personal and/or business credit scores, at least one to two years in business, and verifiable monthly revenue of at least $6,000 to $10,000 or more.

High-pressure sales tactics

Scammers create urgency to push you into decisions before you can think clearly. Legitimate lenders understand you need time to review terms and make an informed decision.

If you feel rushed, pressured, or manipulated, that's your signal to stop and step back. Losing out on a fast-moving "opportunity" is far less expensive than losing money to a scammer.

If something feels wrong, trust that instinct. Business owners who've been scammed later often acknowledge they had doubts but pushed through because they felt desperate for funding.

Suspicious bank account access requests

Some online lenders legitimately request access to your bank account to verify revenues or facilitate fund deposits. Often facilitated through recognized third-party account verification services such as Plaid, MX, or Finicity — services designed to allow view-only access without the ability to withdraw funds.

Be extremely cautious if a lender asks for your actual bank login credentials or requests direct access in a way that isn't facilitated by a recognized third-party service.

Verify lenders: tools and resources

Here are a few resources that may help:

Federal regulatory databases

- OCC (Office of the Comptroller of the Currency) — occ.gov: Search for nationally chartered banks and federal savings associations.

- FDIC BankFind Suite — banks.data.fdic.gov: Verify whether a bank is FDIC-insured.

- Federal Reserve's National Information Center — ffiec.gov/nicpubweb: Look up bank holding companies and state member banks.

- CFPB (Consumer Financial Protection Bureau) — consumerfinance.gov: Search their complaint database for complaints filed against financial services companies.

State licensing agencies

Contact your state attorney general's office to find out whether your state requires lenders, financing companies or brokers to be regulated in your state. If so, use that agency's database to verify a lender's license. You can also check the state where the lender is headquartered if it’s different from your own.

Consumer protection agencies

- FTC (Federal Trade Commission) ReportFraud.FTC.gov: File complaints and search their Consumer Sentinel Network database for reports of fraud and identity theft.

- Better Business Bureau: Research business ratings and search the BBB ScamTracker database for reported scams.

- Your state attorney general's office: State AGs often have consumer protection divisions that investigate financial fraud and may be able to refer you to resources.

Credit monitoring services

When I was targeted by both personal and business identity theft, I caught it quickly because I was monitoring my credit.

Nav is a business credit monitoring platform that helps small business owners track their credit, monitor for fraud, and access trusted lenders, all in one place.

How to protect your business from loan scams

Prevention takes time, but it can save a lot of time and money when compared to getting scammed. These steps can help reduce your exposure before you ever submit an application.

Monitor business and personal credit regularly

By keeping an eye on your personal and business credit reports, you can spot unauthorized inquiries or new accounts you don’t recognize.

Business credit monitoring services like Nav can alert you to unauthorized inquiries or new accounts opened in your business's name, often the first sign of business identity theft.

Understand legitimate loan fees and timing

Fees aren’t uncommon in small business financing, but large upfront fees before you get funding are suspicious. Fees are typically deducted from your loan amount after approval.

When you’re asked to pay using a gift card or through a service like Western Union, Venmo, Zelle or Cash App, there is a good chance you are dealing with a scammer.

Recognize phishing attempts

Scammers often use emails or text messages that look like they're from legitimate companies. They may ask you to click a link or provide sensitive information.

Always verify the sender's identity before responding or clicking any links. When in doubt, contact the company directly using contact information from their official website — not from the email itself.

Safeguard business information and credentials

Legitimate lenders will need some details about your business, but be very cautious about requests for login credentials to your bank accounts or other systems. If a lender requests this level of access, make sure it's facilitated by a recognized third-party provider like Finicity, Plaid, or MX. Never share passwords directly with any lender. Legitimate lenders should not ask for your password.

Take time to review loan terms

Don't rush into any loan agreement. Scammers use false urgency to pressure you into fast decisions. Read all loan terms carefully before signing and get advice from a trusted advisor if you don’t understand them.

Research lender reputation and reviews

Before applying, search the lender's name online. Look for reviews from other business owners and check for any complaints filed with consumer protection agencies.

Every business will likely get some complaints at some time. Look for any concerning patterns: multiple complaints disappearing after fees are paid, unresponsive customer service, loans that never materialize — are serious warning signs. Be especially careful if you're in a financially vulnerable position. Scammers may cast a wide net, targeting lots of businesses, but they are more likely to get struggling business owners to share personal information or pay upfront fees.

What to do if you've been scammed

Falling victim to a loan scam can be stressful and financially damaging. No matter how embarrassed you are, take action. At a minimum, you may be able to help stop them from taking advantage of other business owners.

Secure your financial accounts

If you have shared financial information, like your bank account number or passwords, contact your financial institution and ask them to freeze your accounts or issue new cards to prevent further unauthorized activity. Act the same day if possible.

The very first thing I did was contact the banks and credit card companies listed as inquiries on my credit reports. Because I acted quickly, I was able to shut down several new accounts the scammers had opened.

Contact law enforcement

If you believe your information has been used for identity theft, file a police report. This creates an official record of the incident, which can be helpful if you need to dispute fraudulent debts or items on your credit reports.

This was one of the first actions I took when my identity was stolen, and the police report proved to be helpful when I contacted lenders and the credit bureaus.

Document everything

Keep copies of all correspondence, notes from phone calls, receipts, and any other relevant information. Write down dates, times, names used, and amounts transferred. This documentation can be critical if you pursue legal action, are sued for fraudulent debt, or need to work with law enforcement.

I kept written notes of all my conversations in a folder on my computer for future reference, along with scanned copies of my credit reports, my police report, and other documents. That came in handy as I had to make multiple phone calls to a couple of them.

Report to state and federal agencies

You may want to report the scam to your state attorney general's (AG’s) office. It can help establish a record against the company, and if enough people complain, your AG may investigate.

You can also file a complaint with the Consumer Financial Protection Bureau (consumerfinance.gov) and/or the Federal Trade Commission (reportfraud.ftc.gov). Both agencies use complaint data to identify patterns and potentially take action against scammers.

You may want to file a report with the BBB ScamTracker as well.

Monitor and protect your credit

You’ve seen this advice a few times in this article, and that’s because it’s crucial to helping you identify fraudulent activity. You're entitled to free weekly credit reports from the three major consumer credit bureaus through AnnualCreditReport.com. Look for suspicious activity or accounts you don't recognize.

Consider freezing your personal credit reports, or placing a fraud alert. You can’t freeze business credit, but Experian allows you to place a fraud alert on your business credit report.

Learn about the differences between fraud alerts and credit freezes here.

Seek legal and professional advice

If you lost a significant amount of money, you may want to consult a lawyer who specializes in financial fraud. They can help you explore options for recovery and advise you on next steps. Just keep in mind that some scammers are located outside the U.S., which makes pursuing legal action difficult.

Business loan company verification checklist

Use this checklist to help evaluate lenders.

- Search the company name plus "reviews" or "complaints"

- Verify the website uses "https://" and shows an active security certificate

- Check the Better Business Bureau rating and reviews

- Look up the company's address on Google Maps

- Verify state licensing through the official state regulatory website

- Confirm the phone number matches official records

- Check that company emails come from a business domain, not a generic one like @gmail.com or @hotmail.com

- Search for news articles about the company

- Cross-reference company details with the Secretary of State's business registry

Red flags to watch out for:

- Requests for upfront fees or payments before funds are disbursed

- Pressure to act immediately

- Guaranteed approval without credit checks or financial documentation

- Unsolicited loan offers

- Requests to wire money or send gift cards

- Non-secure website asking for personal or business details

- No verifiable physical business address

- Unusually low rates despite poor credit

- Requests for bank login credentials

- Unwillingness to provide licensing information (if required)