SBA loan calculator: Estimate your SBA loan payments

Written byGerri Detweiler & Robin Saks Frankel

Summary

- Nav’s SBA loan calculator can help you estimate your monthly payments by entering details including loan amount, interest rate, term length, and fees.

- Be aware that different SBA loan types — such as 7(a), 504, and Microloans — have varying costs and eligibility requirements.

- Qualifications including credit scores, cash flow, and business financial details can influence your loan approval and interest rates.

- Remember that while the calculator provides estimates, actual loan terms will depend on your lender's assessment and the specific SBA loan program.

Getting an SBA loan can be an effective way to finance your next big business milestone, whether you receive an SBA 7(a) loan, an SBA 504 loan, or microloan. Each program carries different interest rates and repayment schedules for your SBA loan payments.

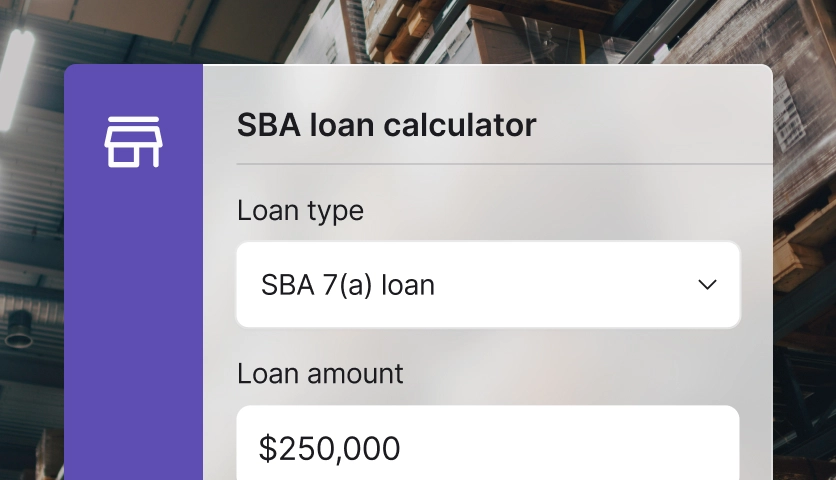

Figure out your SBA loan payment

You can estimate your monthly payment based on the loan type, amount, term, interest rate, and other factors where applicable. Results are estimates only and do not represent a loan offer or approval. Actual rates, fees, and payments depend on lender underwriting and SBA program rules.

Loan type

Loan amount ($)

Up to $5 million

Loan term (years)

Up to 10 years for equipment or working capital, or 25 years for real estate

Interest rate (variable)9.00%

These are variable rates based on the current prime rate of 6.75% as of December 2025. Fixed rates may differ.

- Up to $50,000: prime + 6.50% → up to 13.25%

- $50,001-$250,000: prime + 6.00% → up to 12.75%

- $250,001-$350,000: prime + 4.50% → up to 11.25%

- Over $350,000: prime + 3.00% → up to 9.75%

Maximum allowable SBA 7(a) variable rates (based on prime as of December 2025). Lenders may offer lower rates based on borrower qualifications.

Getting an SBA loan can be an excellent way to finance your next big business milestone, whether you receive an SBA 7(a) loan, an SBA 504 loan, or Microloan.

As a general rule, though, SBA loans often offer longer repayment terms than many other types of small business financing.

SBA loan inputs

To use this calculator, enter the following information:

- Choose the type of loan: SBA 7(a), 504 loan, Express, or Microloan

- Enter your loan amount (maximum $5 million for 7(a) loans or 504 loans, $500,000 for Express loans, or $50,000 for Microloans)

- Enter loan term in years (Up to 10 years for working capital or equipment, though equipment may be financed for up to 15 years if the life of the equipment supports it, 25 years for real estate)

- Interest rate: The SBA sets maximum interest rates. See current SBA loan rates.

- Optional: Choose the guaranty fee. Most lenders pass this cost to the borrower.

Understanding SBA loan payment results

This is a standard term loan calculator for an SBA loan with a variable rate based on the prime rate. To make the best use of this tool, you’ll need some information about your proposed loan:

- Loan amount

- Interest rate (as a percentage)

- Loan term (in months)

- Guaranty fee, if applicable

The SBA 7(a) loan is just one loan offered by the SBA, and this calculator takes the basic factors of your loan cost into consideration to help you generate an estimated SBA loan payment. It will give you an estimated monthly payment with details provided by you, such as loan term, loan amount, and interest rate. Keep in mind that with variable interest rates, your payments may change as rates change.

This calculator is not meant to provide an exact monthly payment for your SBA loan and should not be relied upon as such. For specific costs, consult your lender or the terms of your loan contract.

Types of SBA loans

There are a number of types of SBA loans. Here are SBA loans frequently used by small business owners:

- Standard 7(a) loan: $350,001 to $5 million

- SBA 504 loan: up to $5 million

- Express loan: up to $500,000

- Microloan: up to $50,000

- 7(a) Small loan: up to $350,000

- CAPLines: up to $5 million

- Export working capital (EWC): up to $5 million

- Export Express: up to $500,000

- Working capital program (WCP): up to $5 million

- Manufacturer's Access to Revolving Credit (MARC): up to $5 million

- International trade: up to $5 million

SBA loan payment by loan type

The calculator will help you estimate your payment for an SBA 7(a) loan, Express loan, microloan, or 504 loan. You will get an estimated monthly payment, total repayment amount, interest and guaranty fee. This is an estimate and your actual payments and costs will vary.

SBA 7(a) and Express loan fees

The SBA 7(a) loan program encompasses numerous loan programs including the two of the most popular loans: 7(a) standard and Express loans.

SBA 7(a) and Express loan guaranty fees*

Loan maturity | Gross loan amount | SBA guaranty fee (upfront fee) |

12 months or less | All loan amounts | 0.25% of the guaranteed portion |

Exceeds 12 months | $150,000 or less | 2.0% of the guaranteed portion* |

$150,001 to $700,000 | 3.0% of the guaranteed portion | |

$700,001 to $5,000,000 | 3.5% of the guaranteed portion up to $1 million, plus 3.75% of the guaranteed portion over $1 million |

*Fees for FY 2026 (Effective Oct. 1, 2025. Fees are subject to change by the SBA. Confirm current fees with your lender or the SBA. Note: For loans of $150,000 or less, the lender is authorized to retain 25% of this fee.

The lender may pass the cost of the upfront fee on to the borrower, and the borrower may pay it out of the proceeds of the loan.

Fee waivers

For SBA Express loans made to veteran-owned businesses, the upfront fee is $0.

For loans to manufacturers (NAICS sectors 31-33) of $950,000 or less (not including MARC loans), the guaranty fee is waived.

Other guarantee fees

Lenders may charge borrowers reasonable packaging fees for services such as preparing a business plan, cash flow projections, or other documents related to the application, broker fees, and consulting on the loan.

They can charge a flat fee of $2,500 for these services, or itemize them for the SBA. They may also charge borrowers the actual expenses for credit reports, appraisals, surveys, and attorneys fees, and these fees must be reasonable.

SBA 504 loan fees

CDC 504 loans offer attractive fixed debt loans for financing large purchases. These loans include three parts: a 10% downpayment from the borrower, a loan of up to 40% of the project cost through a Community Development Corporation (CDC) backed by a 100 percent SBA-guaranteed debenture, and a loan of up to 50% by a private lender.

SBA 504 Loan Fee Schedule

These fees apply to the CDC portion of the loan.

Fee type | Amount / rate | Description |

CDC processing fee | 1.5% of net debenture | Paid to the CDC for packaging and processing. You may pay this upfront or finance it in the debenture. |

Closing fee | Reasonable amount (max $10,000 financed) | Reimburses the CDC for legal counsel and miscellaneous closing costs. |

Underwriter’s fee | 0.4% (20/25-year term) | Paid to the underwriter for arranging the sale of the debenture. This is calculated on the gross debenture amount. |

Third party lender fee | 0.50% of senior mortgage | A one-time participation fee charged on the Third Party Lender's loan amount (the bank portion). This may be paid by the lender, CDC, or borrower. |

Funding fee | 0.25% of Net Debenture | Covers costs incurred by the trustee, fiscal agent, and transfer agent. |

CDC servicing fee | 0.625% to 2.0% per year | A monthly servicing fee based on the unpaid principal balance. Standard limit is 1.5% for rural areas and 1% elsewhere. Subject to SBA guidelines and CDC policies. |

SBA annual fee | Varies by fiscal year | An ongoing fee paid to the SBA, charged on the unpaid principal balance. |

Refinance fee | Varies by fiscal year | For "debt refinance without expansion" loans, the borrower pays a supplemental annual guarantee fee. |

Other fees: Borrowers may also be responsible for eligible administrative costs, which can often be financed in the loan. These include:

- Professional fees: Title insurance, title searches, surveys, and zoning costs.

- Appraisals: Required for real estate with an estimated value over $500,000.

- Environmental analysis: Costs for environmental impact fees, such as an environmental site assessment

SBA microloan fees

Fee type | Amount / policy |

Application & origination | Maximum 2% of the loan amount. |

Closing costs | Actual out-of-pocket costs only (appraisals, credit reports, recording fees). |

Technical assistance | $0 (Free). No fees permitted. |

Servicing fees | $0. Covered by the lender's earnings; not charged to the borrower. |

Financing limit | Fees can be financed if the total loan + fees ≤ $50,000. |

SBA microloan fees are simple and straightforward.

Is an SBA loan right for my business?

Whether an SBA loan is right for your business or not depends on factors like your:

- Purpose for the loan

- Creditworthiness

- Time in business

- Collateral availability

- Interest rates and terms

- Use of funds

- Loan size

- When you need the loan

SBA loans can be a good choice for businesses looking for longer-term financing options for purposes like working capital, equipment purchase, or real estate. However, business owners must meet eligibility criteria and be willing to navigate a detailed application process that may take several weeks.

Carefully consider your specific circumstances and financial needs to determine whether an SBA loan lines up with your business goals or not.

How SBA loan interest rates work

Of all the factors that determine your exact monthly loan payment, nothing has more influence than SBA loan rates. The SBA sets maximum loan rates but lenders may offer lower rates based on borrower qualifications.

SBA 7(a) loans may have fixed or variable interest rates. Variable-rate loans carry interest rates that may change periodically when base rates change.

For variable-rate loans, the acceptable base rates are:

- The prime rate (6.75% as of December 2025)

- SBA optional peg rate

Maximum rates vary by loan size. The calculator includes current rates for the loan types and sizes listed.

How to qualify for an SBA loan

To qualify for an SBA loan the main qualifications are:

- You must operate a for-profit small business based in the U.S.

- It may not be an ineligible type of business.

- Must be creditworthy and demonstrate the ability to repay the loan from cash flow.

Learn more about SBA loan requirements here.