Credit card balances: When to pay and when to hold for business

-480x480.webp)

Written byJason Steele

Reviewed by Robin Saks Frankel

Summary

- For small and medium-sized businesses (SMBs), managing a credit card isn’t just about spending; it’s a strategic balancing act. Understanding the nuances of your credit card balances is a critical component of cash flow optimization, credit score protection, and rewards maximization.

- When handled correctly, your business credit card becomes a powerful financial tool that provides float and flexibility. When misunderstood, it can lead to unnecessary interest costs and a damaged credit profile.

- In this guide, we will break down the different types of balances you’ll encounter, analyze when it makes sense to pay early versus waiting until the due date, and explore how these timing decisions directly impact your business’s bottom line.

This resource is intended for informational purposes only. Nav does not provide legal, tax or financial advice. If you have any questions or concerns, please consult with your own legal and accounting professionals.

What are credit card balances and why they matter for small businesses

At its simplest, a credit card balance represents the amount of money you owe the issuing bank. However, for a business, this number is more than just a debt; it is a real-time reflection of your current liabilities and your remaining short-term purchasing power. Maintaining a healthy balance is essential for business operations because it influences your ability to secure future financing and determines the cost of your current capital.

SMBs specifically must master these mechanics to ensure they always have access to bridge funding to manage cash flow for inventory or payroll, to build a robust business credit history that is separate from the owner’s personal credit, and to maintain the financial agility needed to respond to unexpected market opportunities.

Understanding different types of credit card balances

Navigating your online portal can be confusing when multiple dollar amounts are displayed. Understanding each one is the first step in strategic management.

Current balance

The current balance is the total amount of all posted transactions on your account up to the present moment. This is a real-time figure that changes as you make purchases or payments.

Example: If your statement balance was $1,000 but you spent another $500 yesterday, your current balance is $1,500. Note that pending transactions — purchases authorized but not yet fully processed by the merchant — are typically not yet added to this total but will be shortly.

Statement balance

This is the amount you owed at the end of your last billing cycle. The bank takes a snapshot of your account on the statement closing date, and this is the specific amount you must pay by the due date to avoid interest charges on new purchases.

Available credit

Your available credit is your credit limit minus your current balance. This tells you exactly how much more you can spend before hitting your limit.

Example: If you have a $10,000 limit and a $4,000 current balance, your available credit is $6,000. It is important to remember that pending charges — like a hotel hold — will temporarily reduce this available credit even before they appear in your current balance.

Minimum payment

The minimum payment is the smallest amount you can pay to keep your account in good standing and avoid late fees. While it may be tempting during tight cash flow periods, paying only the minimum is the most expensive way to use a card, as the remaining balance will begin accruing interest immediately, often at high double-digit rates.

Statement balance vs current balance: Key differences

The distinction between these two is the most common point of confusion for cardholders. To avoid interest, you generally only need to pay the statement balance, not the full current balance.

Feature | Statement balance | Current balance | Impact |

Definition | Snapshot at end of cycle | Total owed right now | Current is usually higher |

When it updates | Once per month | In real-time (daily) | Statement is static |

What to pay | Pay this to avoid interest | Pay this to maximize credit | Focus on statement |

How credit card balances affect your business credit

Your balance doesn't just affect your bank account; it's a primary signal to credit bureaus.

Credit utilization ratio explained

Utilization is the percentage of your total credit limit that you are currently using. A high utilization ratio — typically anything over 30%, though 10% is the gold standard for high scores — suggests financial stress to lenders. If you have a $50,000 total limit across cards and owe $25,000, your 50% utilization could lower your credit score even if you pay on time every month.

When balances get reported

Most issuers report your balance to the bureaus on your statement closing date. This means if you have a high balance on that day, it will be recorded on your credit report for the next month, even if you pay it off in full two weeks later on the due date.

Impact on business credit scores vs personal credit scores

Some business cards report only to business credit bureaus (like Dun & Bradstreet (D&B)), while others report to personal bureaus as well. If your business card requires a personal guarantee, high balances could affect your personal credit score, potentially impacting your ability to get a personal mortgage or auto loan.

When you should pay your credit card balance early

There are several strategic reasons to pay before the official due date.

Your credit utilization is too high

While there’s no specific credit utilization rate you must stay below to have good credit scores, but FICO® does note that consumers with the best credit scores tend to have very low utilization of less than 10% of their available credit, on average. If your balance is nearing 30% of your limit, making a mid-cycle payment will lower the balance that gets reported on your statement closing date, protecting your credit score.

You need available credit for upcoming expenses

Let’s say you only have $2,000 in available credit, but you want to make a larger purchase on your credit card. Perhaps you want to charge it to earn cash back or reward points (including a welcome bonus), or you want to take advantage of a low-rate balance transfer to pay that purchase off over time.

If you have a major inventory purchase coming up and your current balance is eating into your available credit, paying it down early clears the deck for that expense. If this is a recurring issue, consider requesting a credit limit increase to provide more permanent breathing room.

You're applying for business financing

Lenders look at your recent credit reports. If you are applying for a SBA loan or a line of credit, pay your balances down to near-zero at least two to three weeks before applying to ensure the lower utilization is reflected in the reports the lender pulls.

When you should wait to pay until the due date

In some scenarios the best business move is to hold onto your cash as long as possible. Here are some reasons you might want to do so.

Maximize cash flow during tight periods

Seasonal businesses or those waiting on large client payments (accounts receivable) can use the credit card grace period as a short-term loan. For example, businesses with seasonal income may need to hang on to their cash through the off-season, while others experience client payment delays and unexpected expenses. By waiting until the due date, you keep cash in your high-yield savings or operating account longer.

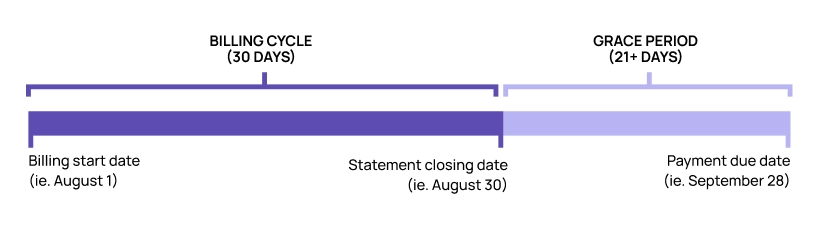

Take advantage of grace periods

If you pay your statement balance in full every month, you get an interest-free period on new purchases. Depending on when in the cycle you buy something, you could have up to 55 days of float before that money actually has to leave your bank account. For example, any charge made at the beginning of your statement period will not appear until your statement is generated 30 days later. And if your account has a 25 day grace period, which is typical, then you will have a total of 55 days to pay off that charge on the due date, and still avoid paying interest.

Use a 0% intro APR offer strategically

If you are taking advantage of a 0% introductory offer, you should only pay the minimum required and keep the rest of that cash working in your business. However, you must have a strict payoff plan to clear the balance before the promotional period ends and high interest rates kick in. For example, you can divide the total amount you owe by the number of months in the 0% APR offer and aim to make payments of at least that amount to knock out the balance before the intro offer expires.

Best practices for managing business credit card balances

Set up automation strategically

Autopay is a safeguard against late fees. Set it to pay the statement balance automatically to avoid interest. If cash flow is highly unpredictable, automate the minimum payment so you never miss a date, then manually pay the rest.

Monitor your balances throughout the billing cycle

Don't wait for the monthly PDF. Check your mobile app weekly to spot unauthorized charges and to see if you need to make a mid-cycle payment to keep utilization low.

Consider multiple cards for different purposes

One effective strategy can be to have separate cards that are best suited for different uses. For example, you could have a card with a promotional financing offer, or a low standard interest rate that you use for purchases that you need to extend payment on. You can then use a card with strong rewards for purchases that you pay in full to avoid interest.

Common credit card balance mistakes to avoid

Paying only the minimum

Paying just the minimum balance is better than paying late or missing a payment, but it can still cost you plenty. For example, a $5,000 balance with 20% APR, paying only the minimum of 2% ($100) a month could cost you an additional $5,992 in interest and over nine years to pay off. Paying $125 a month, just $25 more, reduces your interest charges to $3,361, and allows you to pay off the balance in 67 months, nearly half the time.

Missing the due date

Even one day late can trigger a late fee, which can run as high as $40 and, more importantly, can void your grace period, meaning all your current purchases start accruing interest immediately, often at a higher penalty rate. Delinquencies can also hurt your credit.

Confusing statement balance with current balance

Your statement balance is the balance you had when your statement period ended, while your current balance includes all charges since then. You only have to pay off your statement balance to avoid interest charges, not your current balance.

Ignoring utilization timing

Having a high statement balance will create high credit utilization and can lower your credit score, even when you avoid interest by paying your balance in full every month. By taking into account the timing of your monthly statements, you can manage your statement balances.