Compare top net 60 vendors and accounts right now

Written byGerri Detweiler

Reviewed by Robin Saks Frankel

Summary

- Net-60 vendor accounts give your business sixty days to pay for goods or services, which can help your business manage cash flow.

- If reported to business credit bureaus (and paid on time), these accounts may help build business credit.

- Many vendor accounts don’t involve a personal credit check or require a personal guarantee.

- Net-60 terms are much harder to find than net-30, but they offer greater flexibility if you qualify.

One of the biggest cash flow challenges you may experience as a business owner is the gap between when your business generates revenue and when you have to pay your expenses. Net-60 vendors can help bridge that gap by allowing your business to pay for items sixty days later.

The catch? Net-60 supplier accounts are limited, and programs change quickly. This guide covers accounts available in 2026, explains how to read the fine print on different net-60 term variations, and shows you how to negotiate extended terms with suppliers who don't offer them automatically.

Compare net 60 vendors and accounts

Note: True net-60 programs are limited, and terms can change without notice. The options below were verified as of May 12, 2026, but always confirm current terms directly with the vendor before applying.

Vendor or account | Best for | What you can buy | Terms summary | Who can qualify | Possible credit-building value | Fees or discounts | Biggest drawback |

Faire | Independent retailers buying wholesale inventory | 100,000+ brand products (apparel, gifts, home goods, food, beauty) — retail resale only | Net 60; 0% interest; free returns on first order per brand | Retail businesses; eligibility assessed at signup; may require bank, POS, or accounting link | No confirmed reporting to business credit bureaus | No buyer fees; 0% interest | Credit-bureau reporting or approval criteria not publicly disclosed |

Lowe's Commercial Account | Contractors, tradespeople, and construction businesses | All Lowe's products: lumber, tools, hardware, appliances, flooring, plumbing, electrical, paint, garden | Net 60; 0% interest if paid in full by day 60 | Registered business; credit check required; newer businesses benefit from 4–6 months of existing payment history | Reports to two business credit bureaus including Experian Business | 5% discount on eligible purchases; $1.99/month paper billing fee (opt into paperless to avoid) | Strict pay-in-full-by-day-60 rule — missed deadline can trigger 36.99% penalty APR |

Home Depot Commercial Account | Contractors and construction businesses | All Home Depot products: building materials, tools, hardware, appliances, lumber, plumbing, electrical | Net 60; 0% interest if paid on time; 2% early pay discount if paid online within 20 days | Registered business; ~620+ credit score; EIN required; personal guarantee required for most | Reports to Experian Business, Equifax Business and another bureau | No annual fee; 2% early pay discount if paid online within 20 days | Hard credit pull on application; personal guarantee may be required |

IKEA (via Slope) | Businesses furnishing offices or workspaces | All IKEA products: furniture, office furnishings, home decor, kitchen, storage, lighting | Net 30 or 60; up to $150,000; 0% financing fee | Business 1+ year old; $85,000+ annual revenue; FICO ~625+; no bankruptcies in last 5 years | Does not report to business credit bureaus — cash-flow tool only | 0% financing fee; ACH auto-debit on due date; late fees apply if payment is missed | $85,000 revenue minimum; no credit bureau reporting |

Good Neon | Businesses that need custom indoor signage | Custom neon signs and indoor business signage — B2B only | Net 60; $400–$4,000 credit limit | Active corporation in good standing; 2 existing net-30 accounts required; business credit check; no personal credit check; 30% deposit on first purchase | Reports to Equifax Business, SBFE, and other bureaus | $99/year, no minimum order | Narrow product category; requires prior net-30 history; credit details subject to verification* |

Guapaholics | Business owners focused on building a reporting tradeline | Business consulting services | Net 30, 60, or 90; $50,000–$250,000 credit limit | Qualifications vary by service; available through Nav | Reports to Experian Business, Equifax Business, SBFE, and other bureaus | $200 one-time + $50/month | Narrow service category; qualifications vary by service |

Amazon Business Enterprise | Larger or more established businesses with high Amazon purchasing volume | Virtually everything on Amazon Business: office, electronics, industrial, medical, IT equipment | Net 60 (Enterprise plan only); invite-only credit approval | Enterprise plan required; invite-only; typically 2+ years of established business credit | Reports to one major credit bureau | $10,099/year Enterprise membership; 0% interest if paid on time | Invite-only approval; very high annual membership cost |

Reporting practices, approval criteria, fees, and payment terms may vary and can change without notice. Always verify current terms directly with the vendor before applying.

Faire

Faire is a wholesale marketplace that connects independent retailers with more than 100,000 brands across apparel, gifts, home goods, food, and beauty. For qualified retail businesses (bricks-and-mortar and e-commerce), Faire offers net-60 terms with 0% interest and free returns on your first order from each new brand. That last perk is especially useful for retailers testing unfamiliar products: it can help you receive inventory, see how it sells, and pay the invoice before committing to a brand long-term.

Eligibility is evaluated at signup. Faire may require you to connect a bank account, point-of-sale system, or accounting platform to assess your spending history and set a credit limit. The full approval criteria aren't publicly disclosed, though, which makes it difficult to know in advance whether you'll qualify or what credit line to expect.

One limitation: Faire does not appear to report payments to any business credit bureau. If improving your business credit profile is a goal, Faire's net-60 terms help with cash flow, but won't likely move the needle on your credit reports.

Lowe’s

The Lowe's Commercial Account is a net-60 charge account, which means you're required to pay the full balance within 60 days of each purchase. There's no interest if you pay on time, and cardholders receive a 5% discount on eligible in-store and online purchases. That combination of an extended payment window and a consistent everyday discount makes this one of the more practical accounts for construction businesses, contractors, and tradespeople who already buy from Lowe's regularly.

On the credit-building side, Lowe's reports to Experian Business and another major business credit bureau, making it a solid option for establishing a payment history with two of the three major bureaus.

A few things to watch carefully: The 60-day payment deadline is strict. If you miss it, a penalty APR of 36.99% can apply to the unpaid balance. There's also a $1.99 monthly paper billing fee — opt into paperless billing when you set up your account to avoid it. If your business is under three years old, having at least four to six months of existing payment history on your business credit reports before applying is recommended.

Home Depot

You may have seen the Home Depot Commercial Account described as a "net-30" account, as that label circulates widely in search results. In fact, Home Depot offers several commercial cards and financing programs.

The Commercial Account offers a 2% early pay discount if the invoice is paid online within twenty days, or get sixty days to pay. (The 2% Early Pay Discount will be applied to the purchase subtotal (excluding sales tax) on invoices paid online within 20 days of the transaction date.)

Where Home Depot stands out among net-60 vendors is credit bureau coverage. Vendor materials indicate the account may report to multiple major business credit bureaus, including Experian Business and Equifax Business, making it one of the broader bureau-reporting retail accounts in this guide.

Qualification requirements are more involved than some alternatives. Most applicants need a personal credit score around 620 or higher and will go through a hard credit pull on their application. A personal guarantee is required for most businesses and is only waived if your business has an 80+ Paydex score, $2 million or more in annual revenue, three or more years in operation, and 10 or more employees. Use is limited to Home Depot stores and homedepot.com.

Ikea

IKEA partners with the financing platform Slope to offer net-30 or net-60 terms on purchases made in-store and online, with 0% financing fees and credit lines of up to $150,000. For businesses furnishing an office or outfitting a workspace, the combination of IKEA's product range and flexible payment terms is genuinely useful.

To qualify, your business needs to be at least one year old with $85,000 or more in annual revenue and a FICO® Score around 625 or higher. Businesses with bankruptcies in the last five years or revenues under $5 million may be required to provide a personal guarantee. Payments are collected automatically by ACH on the due date, so make sure funds are available.

The key limitation: IKEA's financing through Slope doesn't report to standard business credit bureaus so it won’t help build credit.

Good Neon

Good Neon offers net-60 accounts for businesses that need custom indoor signage, including neon script signs and wall art, B2B only. The application process requires that your business be an active corporation in good standing and that you have at least two existing net-30 vendor accounts on your business credit report before you apply. There's no personal credit check, but Good Neon reviews your business credit profile. A 30% deposit is required on your first purchase.

On the credit side, Good Neon reports to Equifax Business, SBFE, and other bureaus.

Guapaholics

Guapaholics is a business services provider specifically designed around credit building. It offers net-30, net-60, and net-90 terms with credit limits ranging from $50,000 to $250,000, and reports to Experian Business, Equifax Business, SBFE, and other bureaus, a broad reporting profile that covers more ground than most vendor accounts in this list. Pricing is $200 one-time plus $50 per month, with no minimum order requirement. Qualifications vary depending on the services requested.

Amazon Enterprise

Amazon Business offers Pay by Invoice with net-60 terms through its Enterprise plan, but this isn't an account most small businesses will choose early in their business journey. The Enterprise plan costs $10,099 per year, and net-60 terms through a Business Credit Account are invite-only, typically requiring two or more years of established business credit history.

For businesses that do qualify, the benefit is purchase flexibility. Virtually everything available on Amazon Business is eligible, from office supplies and electronics to industrial goods, IT equipment, and more.

On the credit side, Amazon Business reports to one of the major business credit bureaus only. For most small businesses, the membership cost and eligibility bar make this more of a long-term goal than a near-term option.

How to choose a net 60 vendor before applying

Before applying for a net-60 account, it's worth getting clear on what you're actually trying to accomplish. The right account depends entirely on your goal.

If your priority is cash flow: Look for vendors whose products you'd be buying anyway — where the 60-day window gives you time to sell inventory or collect from clients before the invoice comes due. Faire and IKEA via Slope both may serve this purpose well, for example, even though neither reports to credit bureaus.

If your priority is building business credit: Focus on accounts that report to at least one, or ideally more than one, major bureau. Home Depot, Lowe's, Good Neon, and Guapaholics all report to multiple bureaus.

If you want better terms and business credit: The accounts that deliver cash flow flexibility and bureau reporting can be the best long-term investments. Home Depot and Lowe's are the most established options for businesses in construction or trades, for example, and both offer products you'd be buying regardless.

A few practical questions to ask before you apply:

- Does this vendor sell something my business actually needs to buy on a regular basis?

- Does the account report to the bureau or bureaus where I most need to build history?

- Can I realistically pay the invoice in full within 60 days, given my current cash cycle?

- What are the consequences if I miss a payment, such as late fees, penalty APR, or negative credit reporting?

Net-60 terms are most valuable when they align with your natural cash cycle. Buying inventory on net-60 only makes sense if 60 days is enough time to sell that inventory and collect payment before the invoice is due.

Pros and cons of net 60 terms

Net-60 terms can offer real advantages over paying upfront or on shorter payment cycles, but they aren't the right fit for every business or every purchase.

Common net 60 variations to know

Term | What it means | When the payment clock starts* | What to watch for |

Net 60 | Full invoice amount due within 60 days | Invoice date | Confirm whether terms count calendar days or business days — most use calendar days |

2/10 net 60 | 2% discount if paid within 10 days; full amount due by day 60 | Invoice date | The discount is optional — skipping it doesn't trigger a penalty, but you lose the savings |

1/10 net 60 | 1% discount if paid within 10 days; full amount due by day 60 | Invoice date | Smaller incentive than 2/10; weigh whether early payment fits your cash position |

Net 60 EOM | Full invoice due 60 days after the end of the billing month in which the invoice was issued | End of the billing month | Effective payment window can be longer or shorter than standard net 60 depending on the timing of your purchase |

Net 60 ROG | Full invoice due 60 days after goods are received — not the invoice date | Date goods arrive | Useful when there's a lag between invoice date and delivery; confirm this is what the contract specifies, not assumed |

*While these are typical definitions, always check with the vendor to make sure you understand your payment terms and to avoid paying late.

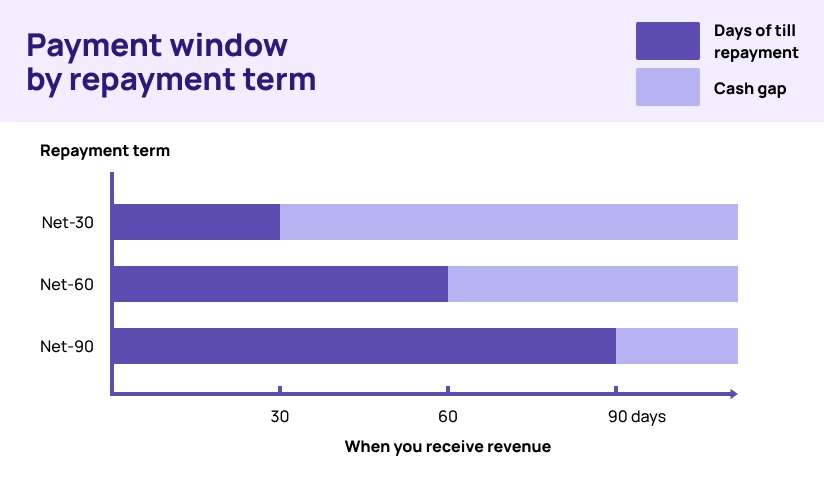

Net 30 vs. net 60 vs. net 90: What’s the difference?

Net terms describe the number of days from an agreed-upon start date (usually based on the invoice date) by which you must pay the invoice in full. Net 30 terms (or even shorter) are most common. Net 60 and net 90 are less common, and typically reserved for established business relationships with significant order volume.

Longer terms aren't automatically better. The right choice depends on your cash flow cycle, the nature of your work, and what the vendor's approval criteria require.

Payment window | Best for | Cash-flow benefit | Approval difficulty | Risk level | How common |

Net 30 | Fast inventory turnover or short project cycles | Moderate: 30 days to align inflows and outflows | Often low: more widely available | Lower: limited open exposure per invoice | Very common; industry standard |

Net 60 | Longer selling cycles, seasonal inventory, or project-based revenue | Strong: covers most selling and collection cycles | Moderate: more vetting than net 30 | Moderate: two months of open exposure | Less common; often requires stronger relationship or credit profile |

Net 90 | Larger buyers, established relationships, or extended production cycles | Highest: maximum float on cash | Highest: typically reserved for established accounts | Higher: 90 days of open receivables is significantly more risky for the vendor | Rare; usually negotiated, not offered upfront |

When net 30 makes more sense

This is the typical starting point for most vendors that offer payment terms. Some will offer net-10 or net-15 payment terms, but net-30 is quite common. It’s often a matter of qualifying first for net-30 terms before you can negotiate longer payment terms.

When net 60 makes more sense

While net-60 terms can give your business more time to generate revenue to pay these bills, there are very few vendors that advertise net-60 terms upfront. You may need to earn these kinds of payment terms.

When net 90 makes sense

Net-90 terms are rare and typically require a strong, established supplier relationship, significant order volume, or a long track record of on-time payments. It is often by invitation, rather than something you apply for.

Expect more scrutiny at the application stage and less flexibility if a payment is late. For most small businesses in the early stages of building credit, net 90 is an aspirational goal, but not a starting point.

Which net 60 accounts can help build business credit

Bureau reporting policies are difficult to verify independently, can change without notice, and aren't always disclosed publicly by vendors. The information below reflects Nav’s independent research as of May 2026. Always verify a vendor's current reporting policy directly before opening an account with credit building as your goal.

- Home Depot Commercial Account: reports to multiple bureaus including Experian Business, and Equifax Business.

- Lowe's Commercial Account: reports to Experian Business and another major business credit bureau.

- Guapaholics: reports to Experian Business, Equifax Business, SBFE, and other bureaus. Designed specifically for credit building.

- Good Neon: reports to Equifax Business, SBFE, and other bureaus.

A few principles worth keeping in mind as you build your credit strategy:

- Get multiple accounts if you want to build business credit. No single vendor reaches all three major bureaus. You may need multiple accounts that report, and pay on time, to establish a solid business credit history.

- Consistency matters more than volume. One account with consistent monthly payments can help your business credit profile more than several accounts with spotty histories. Don't take on more vendor credit than your cash flow can reliably support.

- Late payments can appear even one day past due. Set up auto-pay or payment reminders well before each invoice deadline. Some vendors may report late payments quickly, including accounts only slightly past due.

- Nav Prime gives you up to three reporting tradelines (two business, one personal) that report to major business credit bureaus. It can give you a foundation to build on if you're starting from scratch or supplementing vendor accounts.

How to qualify for net 60 vendor accounts

Net-60 accounts carry more risk for the vendor than net-30 accounts, since they are extending sixty days of interest-free credit. That means they tend to come with higher qualification requirements than shorter-term programs. Here's what to expect across most programs.

- A registered business entity. Most net-60 vendors require a formally registered business, such as an LLC or corporation. A sole proprietorship may not qualify.

- An employer identification number (EIN). A valid EIN is required by most programs and is the primary identifier used to pull your business credit file. If you don't have one, you can apply at IRS.gov at no cost.

- A D-U-N-S® number. Some vendors require or prefer that you have a D-U-N-S® number on file before you apply. You can register for a D-U-N-S® Number through Dun & Bradstreet (D&B).

- Time in business. Many net-60 programs require at least one to two years of operating history. IKEA via Slope, for example, requires a minimum of one year with $85,000 in annual revenue. Newer businesses may need to start with net-30 accounts and build from there.

- Existing vendor payment history. Some programs require at least two net-30 accounts on your business credit report before they'll consider a net-60 application. This is a common threshold: vendors want evidence that you can handle trade credit before extending a longer window.

- Purchase history with the vendor. Some programs won't offer net-60 terms on your first order. You may start on cash terms or shorter net terms and only unlock net-60 after a documented track record with that specific vendor.

- A credit review. Expect a business credit review at minimum. Home Depot, for example, conducts a hard pull on personal credit for most applicants. Know what kind of pull to expect before applying so you're not caught off guard.

How to ask an existing supplier for net 60 terms

Not every net-60 account is a program you apply to: some are terms you negotiate. If you already have a supplier relationship, this may be an option. The key is to ask at the right time, in the right way.

When to make the request

You’ll have the most leverage to ask for extended terms if you've built a track record with a vendor, including consistent on-time payments, growing order volume, and a relationship that spans at least several months. Paying ahead of terms whenever possible can also strengthen your case when you ask.

Don't bring up payment terms if you’re having trouble paying on time, or if you have a large outstanding invoice.

What to say to a supplier

You don't need a formal script to ask for better terms. You just need to make a direct, brief request. For example:

"We've been working together for [X months/years] and I'm looking at ways to keep growing our orders with you. To support that growth, I'd like to discuss moving from net-30 to net-60 terms. Our payment history has been [on time/ahead of schedule], and we're planning on [increasing order volume / a larger project coming up]. Extended terms would help us plan more predictably on our end. Would you be open to talking through that?"

Keep it brief, lead with your track record, and tie the request to continued — or increased — business for the vendor. Suppliers value reliable buyers, and framing the ask as a growth conversation rather than a financial request changes the dynamic.

If you’re only making small, occasional purchases you may not get far. But if you regularly purchase from the vendor and are making larger purchases, you may be able to get longer payment terms.

When to make the request

You’ll have the most leverage to ask for extended terms after you've built a track record with a vendor, including consistent on-time payments, growing order volume, and a relationship that spans at least several months. Paying ahead of terms whenever possible can also strengthen your case when you ask.

Don't bring up payment terms if you’re having trouble paying on time, or if you have a large outstanding invoice.

What to say to a supplier

You don't need a formal script to ask. You just need to make a direct, brief request. For example:

"We've been working together for [X months/years] and I'm looking at ways to keep growing our orders with you. To support that growth, I'd like to discuss moving from net-30 to net-60 terms. Our payment history has been [on time/ahead of schedule], and we're planning on [increasing order volume / a larger project coming up]. Extended terms would help us plan more predictably on our end. Would you be open to talking through that?"

Keep it brief, lead with your track record, and tie the request to continued — or increased — business for the vendor. Suppliers value reliable buyers, and framing the ask as a growth conversation rather than a financial request changes the dynamic.

What else to negotiate besides the due date

The due date is a point of negotiation. If the vendor isn't ready to go straight to net-60, you may be able to consider negotiating other terms that improve your position:

- A staged transition: Ask for net-45 first, with an explicit understanding that net-60 can be revisited after another quarter of on-time payments.

- Early pay discounts: If the vendor won't extend terms, a 2/10 or 1/10 structure can reward you for paying early on your existing terms and give the vendor something in return.

- A higher credit limit: If you've been bumping against a low ceiling on an existing account, a larger limit may give you the breathing room you need without changing the payment window.

- Partial deposits on large orders: Some vendors are more willing to extend longer terms on big purchases if you put a percentage down upfront, which reduces their risk exposure.

Alternatives if you cannot get net 60 vendors

If net-60 vendor accounts aren't accessible yet — or don't cover the types of purchases your business actually makes — there are financing other tools that can provide similar benefits.

Business credit cards

Most business credit cards offer a grace period — typically 21 to 25 days after the statement closing date. If you time a major purchase to fall just after your statement closes, you can effectively get almost 60 days to pay before interest accrues. Cards that report to business credit bureaus (many do) can also build your credit profile if you pay on time.

Business loans and lines of credit

A business line of credit works like a revolving account: you draw from it as needed and repay over time. Unlike vendor accounts, a line of credit can be used with any supplier, whether or not that supplier offers trade terms.

The trade-off is that most lenders require documented revenue, a minimum of one year in business, and an acceptable credit score (personal and/or business credit). Interest will be charged on the balance.

Nav Prime

If your primary goal is building business credit while managing cash flow, Nav Prime provides up to three reporting tradelines (two business, one personal) that report to all major business credit bureaus.