What is a FICO SBSS score? And how to raise this business credit score

Written byGerri Detweiler

Reviewed by Robin Saks Frankel

Summary

- The FICO® SBSS℠ score is designed to help lenders make credit decisions about small businesses. It ranges from 0–300.

- This score can evaluate personal and business credit data, as well as application and financial data.

- It is used by financial institutions, and by some SBA lenders.

- Learn how you can check, understand, and improve your business’s SBSS score.

What is a FICO SBSS score?

FICO® Small Business Scoring Service℠ (SBSS) is an application risk score that can impact whether your business gets approved for certain small business loans and credit limits.

Created by the FICO, which creates the popular consumer FICO scores, SBSS uses the FICO® LiquidCredit® Service, an analytics platform, to deliver information that helps lenders predict the likelihood of major delinquencies, charge-offs, or bankruptcy. The score helps them evaluate loans for amounts up to $1 million, including term loans, lines of credit, and commercial credit cards.

Many entrepreneurs have never heard of this score, partly because it's traditionally been hard to access. Unlike consumer credit scores available through myFICO.com, FICO doesn't sell this score directly to business owners.

What’s changing with FICO SBSS scores

For years, the U.S. Small Business Administration required lenders to use FICO SBSS scores for certain SBA loans. As of March 1, 2026, the SBA will sunset this requirement. However, it’s expected that many lenders who use FICO SBSS will continue using it, since it's a tested and validated scoring model.

If you're considering a small business loan through a traditional lender such as a bank, understanding this score could make the difference in your approval odds and loan terms.

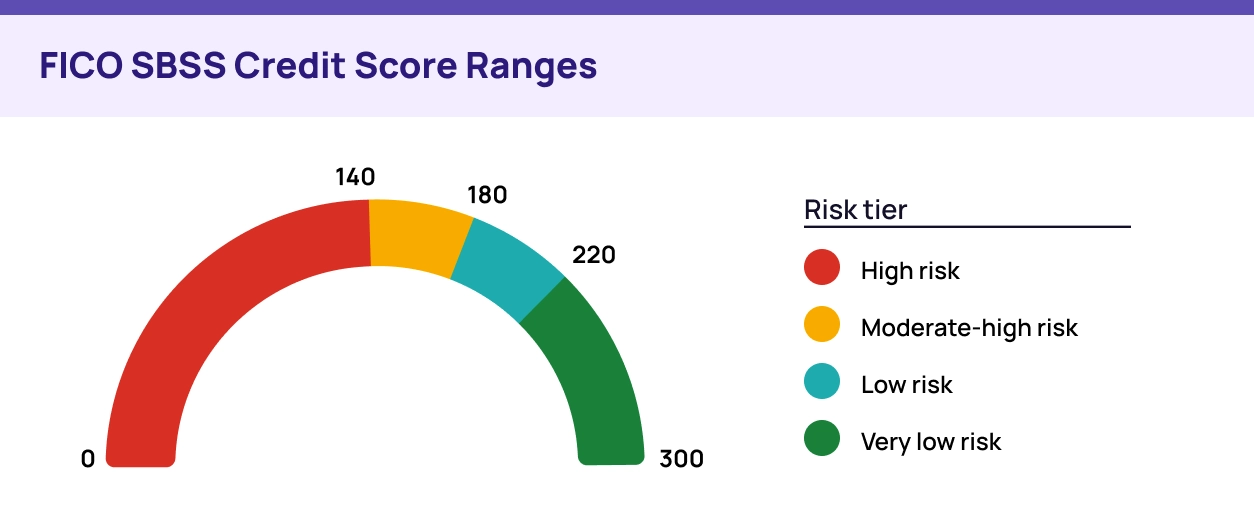

SBSS score ranges and risk levels

The FICO SBSS score ranges from 0 to 300 and a higher score indicates lower risk to lenders. Every lender is different, though, and has its own standards, so there is no specific score range that is “good” or “bad” to all lenders or for all purposes.

Score range | Risk tier | Observations |

0–140 | High | High risk, and more likely to result in rejection |

140–180 | Moderate- high | Higher risk, and many lenders will reject application |

180–220 | Low | Lenders may consider this score range low risk |

220–300 | Very low | Often very low risk, and higher scores may result in lower rates and terms |

What is a good FICO SBSS score?

Again, each lender decides what scores are acceptable, and that’s not information lenders typically reveal.

We can look at SBA 7(a) Small Loan requirements to get an idea how lenders have used the FICO SBSS score in the past.

Lenders have been required to prescreen these applications using a FICO SBSS score, with a minimum score of 165 or more required. (That minimum was raised from 155 in June 2025).

Some lenders will accept scores in the 160–180 range, while others will require scores of 180 or higher.

SBSS scores of 220 and above are often considered low risk, depending on the lender, and may result in expedited underwriting and may help you qualify for better rates and terms.

If you apply for traditional small business financing, your FICO SBSS score may influence whether you get approved, how much you can borrow, and what terms you'll receive.

Why the SBSS score matters

Several types of lenders and financial institutions may use FICO SBSS scores:

SBA lenders

The SBSS score was developed by the SBA working with Dun & Bradstreet. The National Association of Government Guaranteed Lenders points out that “the model has been validated and tested based on SBA loan performance, and the Agency has indicated its strong confidence in it as a tool for determining creditworthiness for 7(a) small loans.”

Again, for SBA Small Loans (loans of $350,000 or less), lenders have been required to prescreen applications using a FICO SBSS score, with a minimum score of 165 required. Although the SBA will no longer require this score be used in this way as of March 1, 2026, it’s expected that many lenders will continue using it as they’ve done in the past.

Banks and credit unions

Banks, credit unions, and financial institutions nationwide may use FICO SBSS scores for small business loans, lines of credit, and commercial credit cards. The score can help these lenders quickly evaluate applications for amounts up to $1 million.

Equipment financiers

Equipment financing companies and agricultural lenders may use FICO SBSS scores to assess risk when financing equipment purchases or leases up to $250,000.

Other commercial lenders

Various commercial lenders may use this score among other factors as part of their underwriting process for term loans and revolving credit facilities.

A strong FICO SBSS score may open doors to better financing options, while a lower score may limit your choices or result in higher interest rates or stricter terms.

How is the SBSS score calculated?

The SBSS score is one of the more complex business scores because it can evaluate multiple types of data to assess a business's creditworthiness.

What information does FICO use?

FICO doesn't have any credit information about how consumers or businesses pay their bills; it simply creates the formulas used to calculate credit scores. The information it uses to calculate this business score comes from multiple sources including business and consumer credit reporting agencies, the lender, or other data sources.

SBSS scorecards can use up to four types of information:

1. Consumer credit data

This data can come from one of the consumer credit reporting agencies: Equifax, Experian, or TransUnion

2. Business credit data

The score can pull business credit data such as:

- Dun & Bradstreet (D&B)

- SBRI (Small Business Risk Insights)

- Experian Business

- Equifax (blended with SBFE data)

3. Application data

Application data includes information typically found on loan applications:

- Time as owner

- Business checking account (DDA) balance

- Percentage of ownership

- Owner's net worth and income

4. Financial data

Financial data can include basic business financial information:

- Business net worth

- Total assets and liabilities

- Cash and equivalents

- EBITA (earnings before interest, taxes, and amortization)

- Annual interest expense

How lenders may use the FICO SBSS score

In addition to using this score for small business loan applications for credit cards, small business term loans and lines of credit, and equipment financing, lenders may use it for specialized decisions, such as:

- Start-up business models: Designed specifically for new businesses with limited credit history, making it easier for lenders to confidently serve this market

- Bankruptcy scores: Focus specifically on bankruptcy risk assessment, used alongside standard SBSS risk scores

- Credit offer index: Helps lenders evaluate whether a loan request is reasonable based on what similar businesses have requested

How can I improve my SBSS score?

Since the FICO SBSS score can evaluate personal credit, business credit, application data, and financial information, you may have multiple paths to strengthen your score.

1. Strengthen personal credit

Personal credit data is an important factor in FICO SBSS score calculations. If your personal credit is not strong, consider steps to raise your scores, such as:

- Pay down credit card balances: High credit utilization may hurt credit scores. Aim to use less than 20%-25% of your available credit limits across your personal credit cards.

- Make payments on time: Payment history accounts for 35% of your personal FICO score. Set up automatic payments or payment reminders to avoid missing due dates.

- Address negative items: If your credit report lists late payments, collection accounts, or other negative information, work to resolve these issues. As negative information ages, it can have less impact on your scores, and most negative information is not reported after seven years.

- Avoid opening unnecessary credit accounts: New credit inquiries and recently opened accounts may temporarily lower your scores.

2. Strengthen business credit

A solid business credit history can boost your SBSS score, especially when combined with solid personal credit. If your business doesn’t have many accounts on your business credit reports, you may find you have what’s called a “thin credit file”. You may need to get accounts that report to business credit bureaus so you can build a good payment history. These are often called “tradelines.”

- Open accounts with vendors that report to Dun & Bradstreet, Experian Business, or Equifax

- Pay invoices on time or early to establish a positive payment pattern

- Consider using Nav's list of net-30 vendors that regularly report to business credit bureaus

3. Maintain up-to-date business financials

Since SBSS can evaluate business financial data, accurate financial records are important.

- Track business net worth, assets, and liabilities

- Monitor cash and equivalents

- Calculate EBITA (earnings before interest, taxes, and amortization)

- Keep records of annual interest expenses

Having this information readily available and up-to-date may help strengthen your SBSS score when financial data is included in the calculation.

4. Dispute errors proactively

Review both personal and business credit reports regularly and dispute any inaccuracies:

- Check your personal credit reports from Equifax, Experian, and TransUnion

- Review your business credit reports from Dun & Bradstreet, Experian Business, and Equifax

- Dispute any errors directly with the credit reporting agencies

- Provide documentation supporting your dispute, such as payment records or account statements

- Follow up within 30 days if you don't hear back

If your credit reports aren’t accurate, your scores won’t likely be either.

5. Maintain low utilization on business lines

Keep credit card balances low relative to credit limits on business accounts. Business credit reports don't always list credit limits; instead, recent high balance may be used for this calculation. Keeping balances low demonstrates good credit management.

6. Build a strong business checking account balance

Your business checking account balance may be included in the SBSS calculation as application data. Maintaining a healthy balance in your business bank account can positively impact your score.

7. Consider your business partners' credit

If you have multiple business owners, remember that an SBSS can evaluate personal credit data from multiple owners and will use the lowest score for the final FICO SBSS score. Always discuss and review the credit of potential or current business partners.

If you have derogatory or no credit history, it can take several months or more of positive credit activity to move your SBSS score significantly higher. Work on your credit early to help ensure it's healthy before you need it.

How to check your SBSS score

FICO does not sell a FICO SBSS product directly to business owners, like it does with its MyFICO products for consumers.

Currently, Nav is one of the few places you can see a FICO SBSS score. Nav provides access to one version of your FICO SBSS scores through its credit monitoring platform.

How long does it take to build an SBSS score?

How long it will take you to build an SBSS score depends on your starting point.

Keep in mind there isn’t a single FICO SBSS score for each business. Like all FICO scores, there are different versions (scorecards). In addition, banks and other lenders can set up the SBSS model they use in different ways, deciding which business credit bureau to get

It’s also considered a “smart” business credit scoring model because it can automatically go from one consumer and/or business credit bureau to another, in whatever order of priority the lender prefers, until it’s able to generate a score.

Let’s say a lender prefers using Experian for business credit data as the default. If a credit report from Experian doesn’t provide enough information to generate a score, it can automatically get business credit data from Dun & Bradstreet. If there’s not enough business credit data available, it may just use the personal credit data to calculate the SBSS score, potentially along with business financials.

If you are starting the process by scratch, then, this is an outline of a timeline. Because your credit and financial data is unique, your results may vary.

Weeks 1–4: Setup phase

- Form business entity and get EIN

- Open business bank account

- Secure tradelines that report to business credit bureaus

- Make first purchases and pay on time

Months 1–3: Reporting phase

- Vendors report first invoices to credit bureaus (can take several weeks)

- New accounts begin appearing on business credit reports

- Make on-time payments to help establish positive payment history

Months 4–12: Score growth phase

- Business credit scores start to appear when sufficient tradelines report (days 90–120, varies)

- Credit scores may improve with consistent on-time payments

Learn how to build credit for your business with Nav’s free guide, Smart Credit Strategies for Small Business Owners.