SBA loans

Small Business Administration (SBA) programs range from short-term working capital to long-term financing, and some SBA loans can even be used to refinance debt! SBA loans carry attractive terms. Learn how to qualify and apply.

SBA loan details

- Loan Amounts: $5,000–$5.5 million

- Interest rates: Varies depending on type of SBA loan

- Repayment terms: 6–25 years

- Turnaround time: About 60 to 90 days

SBA loans pros and cons

What are SBA loans?

SBA loans may help you start or grow your business with loans that carry lower interest rates, low down payments and favorable terms. Except for Disaster Loans, the SBA doesn’t make small business loans. Individual lenders make SBA loans, which are typically guaranteed in part by the U.S. Small Business Administration (SBA), a federal government agency.

SBA loan payment calculator

What is the SBA?

The SBA was created in 1953 and is a U.S. federal government agency tasked with providing access to capital, along with counseling, exporting and contracting expertise for entrepreneurs. SBA loans are just a part of what it offers. Small business owners can also get free counseling through resource partners such as Small Business Development Centers, SCORE, Veterans Business Outreach Centers and Women’s Business Centers. It also provides assistance and expertise for businesses that want to qualify for government contracts or export to other countries. It is funded by taxpayers through Congressional appropriations. That means your tax dollars help it help small business owners, so be sure you take advantage of what it has to offer.

Benefits of SBA loans

Why consider an SBA loan? In short, because it’s probably going to be one of the best business loans for small businesses you can get. SBA loans are considered good business loans, with small business-friendly terms. Here, you’ll learn about the types of SBA loans and why you should consider this popular type of funding for your small business.

How the SBA helps small businesses get loans

The SBA helps small businesses get loans, either directly through the Disaster Loan program or indirectly by guaranteeing a significant portion of an SBA loan made by a participating lender. The guaranty helps reduce the risk to the lender. The SBA sets detailed standards that these loans must meet. If the lender has followed SBA guidelines and the borrower defaults, the SBA will pay the guaranty amount to the lender. (The SBA then may try to collect from the borrower, and being a federal agency it has some significant collection powers.)

SBA loan interest rates

The biggest draw: SBA loans offer low interest rates. “The rates are amazing,” says Bob Coleman, publisher of The Coleman Report, the leading SBA intelligence report for lenders. “For a patient entrepreneur who has her ducks in a row and is willing to go through the process, it’s a lot cheaper capital,” he explains. Interest rates may be fixed or variable, and are pegged to the prime rate, the LIBOR rate, or an optional peg rate. The SBA sets a maximum interest rate that may be charged, but beyond that, interest rates on SBA loans can often be negotiated between the borrower and the lender. SBA loan interest rates vary by program.

Types of SBA loans

1. SBA 7(a) loans

The most popular type of SBA guaranteed loan. These loans may be used for a variety of purposes including new construction, expansion or renovation, or to purchase land or buildings; to purchase equipment, fixtures, leasehold improvements; working capital; to refinance debt for compelling reasons; for a seasonal line of credit, inventory or starting a business.

The Paycheck Protection Program (PPP) fell under the 7(a) program and was created by The CARES Act to help businesses impacted by the coronavirus crisis. These loans were fully forgivable if funds were spent on certain expenses, primarily payroll. The PPP loan program is now closed to new applications.

2. SBA Express loans

These are smaller loans (up to $500,000) with a faster turnaround for approval. They are currently the most popular SBA loan program in terms of total amounts funded. Both term loans and lines of credit are available under this program. These loans may be used for the same purposes as 7(a) loans.

SBA Express Bridge loans were offered under a pilot program during the pandemic. This program allowed SBA Express lenders to deliver expedited SBA-guaranteed financing on an emergency basis for disaster-related purposes to eligible small businesses, while the small businesses applied for long-term financing. This program expired March 13, 2021.

3. SBA 504 loans

The SBA CDC 504 loan program provides small businesses with long-term, fixed-rate financing used to acquire fixed assets for expansion or modernization. Loans are made through partnership with a non-profit Certified Development Company (CDC) and a private lender. They are typically structured where CDC provides 40% of total project costs (and the SBA guarantees that portion of the loan), the lender covers up to 50% and the borrower contributes 10-20%. These loans can be great for acquiring owner-occupied real estate. (The owner must occupy 51% or more of the property depending on the type of loan.)

4. SBA microloans

SBA microloans are smaller loans made primarily by non-profit community-based organizations. Loan proceeds may be used for working capital, supplies, machinery and equipment, fixtures, etc. They may even be used to refinance debt to improve cash flow. (And some lenders make SBA Microloans to startups.)

5. SBA disaster loans

The SBA Disaster Assistance program offers loans to qualified businesses to help them recover from a federally declared disaster. Business Physical Disaster Loans can be used to repair or replace disaster-damaged property owned by the business, including real estate, inventories, supplies, machinery and equipment. Note businesses of any size may be eligible. Economic Injury Disaster Loans (EIDL) are working capital loans to help small businesses and nonprofits meet financial obligations that can’t be met as a direct result of the disaster.

The Economic Injury Disaster Loan program was extended nationwide in March 2020 to help businesses impacted by coronavirus pandemic. These loans were available to qualified small businesses including certain nonprofits and agricultural businesses. The CARES Act added the EIDL grant or advance of up to $10,000 (implemented as $1000 per employee) and later legislation added a Targeted EIDL grant for up to $15,000. EIDL advances (grants) do not have to be repaid, but EIDL loans are not eligible for forgiveness. This program is closed to new applications.

6. SBA international trade loans

SBA international trade loans are designed for U.S. small businesses engaged in or preparing to engage in international trade, as well as those hurt by competition from imports. The borrower must demonstrate they will use this financing to significantly expand an existing export market or develop new export markets, or that the business has been hurt by import competition and proceeds will be used to improve its competitive position.

7. SBA export working capital loans

SBA export working capital loans are short-term, working-capital loans for exporters, typically in the form of a revolving line of credit. Proceeds from export loans may be used for a variety of purposes, including to purchase inventory for export or to manufacture items for export, working capital directly related to export activities, and even refinancing.

8. SBA Export Express loans

SBA Export Express loans, which come in the form of term loans or revolving lines of credit, can be used for “any export development activity” including fixed assets, refinancing and working capital. Designed to be more streamlined with reduced documentation requirements, the SBA provides an answer in 36 hours or less. (Funding will take longer.)

9. Community Advantage

The Community Advantage loan program is a loan program that offers loans through mission-oriented lenders, which are usually nonprofit financial intermediaries focused on economic development. There is a focus on business owners in under-served markets.

The Biden Harris administration has recently announced that the maximum loan amount will increase to $500,000 for most lenders who participate in the CA program. These loans carry a maximum term of 10 years for working capital; 10 years or the useful life of equipment; and 25 years for real estate.

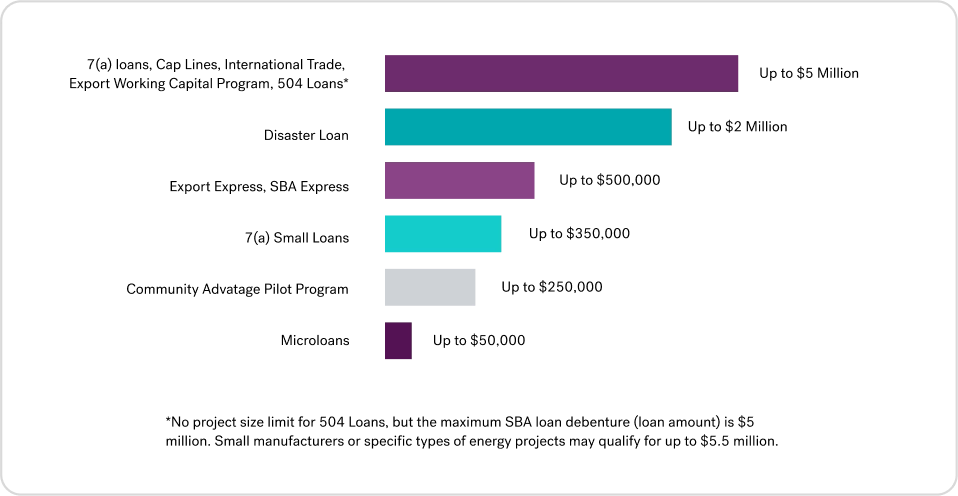

How much you can borrow

Here’s an overview of the maximum amount business owners can borrow through various SBA loan programs:

Who is eligible for an SBA loan?

To qualify for an SBA loan, there are basic requirements you generally must meet:

- Own a qualifying small business: Check out the SBA’s free Size Standards Tool at SBA.gov/size-standards to see if your business qualifies based on the size of your business. This varies by industry.

- Operate a for-profit business located in the U.S: Certain types of businesses are prohibited from getting SBA loans. An example would be a business primarily involved in gambling. The SBA website provides a complete list of ineligible businesses.

- Have good credit: Lenders will check personal credit for all owners with at least 20% ownership. Some loans (such as larger EIDL loans) check business credit. Certain SBA loans require the lender to prescreen the application using a FICO® Small Business Scoring Service℠ (SBSS℠) score. That means this score will be one of the first things the lender must consider. This credit score can evaluate data from the owner’s personal credit as well as business credit and even include financial data. Where the FICO SBSS score is required, the SBA requires a minimum score of 140 or 155 (out of 300). But lenders are free to require higher scores, and many require 160-165 or above. When personal credit scores are used, many lenders require minimum scores of 650-680, though some programs, such as the microloan program, are more credit flexible. Other than the FICO SBSS, the SBA does not require specific minimum business credit scores.

- Exhaust other financing options: These loans are generally designed for small businesses who can’t get credit at similar terms elsewhere. That doesn’t mean you need a stack of rejection letters from other lenders, though; your lender will work with you to understand whether you meet this requirement. These loans are generally designed for small businesses who can’t get credit at similar terms elsewhere. That doesn’t mean you need a stack of rejection letters from other lenders, though; your lender will work with you to understand whether you meet this requirement.

- Have the ability to repay the loan: The lender will need to document that you’ll be able to repay the loan from future cash flow. Your lender can help here, but understand that financial documentation can be extensive.

- Have invested equity into the business: The lender will be required to demonstrate that you have invested your own time or money into the business. These are often referred to as “equity injection” requirements.

There are other requirements that a business must meet. You don’t have to be a citizen, for example, but undocumented business owners aren’t eligible. And if you’ve ever defaulted on a federal loan (including a federal student loan) it’s going to be much harder to qualify. Those with criminal records aren’t automatically disqualified, but you will have to provide additional information.

Are SBA loans hard to get?

First, don’t let the requirements of SBA loans scare you off from considering one. Think of SBA financing as you would any other conventional loan.

“It’s a regular loan and the entrepreneur never deals with the government,” explains Coleman. “The bank lends out its own money and the loan is serviced by the bank.”

Second, understand that while each lender must meet SBA minimum requirements in order to collect the SBA guarantee if needed, lenders may also have their own requirements. One lender may require two years in business for some loans, while another may not.

“It’s very competitive,” says Coleman. “There are a lot of lenders out there willing to make these loans. The entrepreneur has a lot of choices of which lender to work with.”

How to apply for an SBA loan

You don’t need to know all the ins and outs of the SBA loan program to apply for an SBA loan. All you need to do is to focus on finding an SBA lender to work with. While the SBA sets minimum standards, individual lenders may impose additional eligibility requirements, as long as they don’t discriminate on a prohibited basis. That means, for example, you may find one lender requires higher personal credit scores than another. Or a lender may not work with businesses in certain industries, while another lender will. In other words, you’ll shop for an SBA lender just as you would shop for other types of loans.

How to find an SBA lender

While all lenders who make these loans must be approved by the SBA, “preferred lenders” have demonstrated a thorough understanding of the requirements of various SBA loan programs and can expedite approvals. They get full authority to approve loans. “Certified lenders” are also actively engaged in making SBA loans and they get a faster turnaround on loan approvals, though they must get final approval from the SBA. Either way, your lender will guide you through the SBA loan application process.

Here are a couple of ways to find an SBA lender:

- Nav's marketplace: Nav is not a lender. Instead, it partners with lenders and lending partners, including some that make or facilitate SBA loans. With a free or paid Nav account, you will be matched to financing options based on your credit data and other qualifications. This is one of the most effective ways to narrow your search without impacting your credit scores.

- Local advisors: A Small Business Development Center (SBDC) advisor or SCORE mentor will often be familiar with local lenders and the types of small business owners they fund. Your advisor can also help you understand how much you need to borrow and the best way to use loan proceeds. Find your loan advisor through the SBA Locator Tool. The SBA also offers a free tool called Lender Match.

Top lenders for SBA loans

The U.S. Small Business Administration regularly publishes SBA lending data on the “most active” SBA 7(a) lenders in the country. This list is updated quarterly. Here are popular lenders as of the end of 2021:

Popular SBA lenders by number of 7(a) loans approved*

Lender | Loans Approved |

1. The Huntington National Bank | 974 |

2. Wells Fargo Bank, N.A. | 473 |

3. U.S. Bank, N.A. | 416 |

4. Newtek Small Business Finance, Inc. | 334 |

5. TD Bank, N.A. | 302 |

6. Manufacturers and Traders Trust Co. | 249 |

7. Live Oak Banking Company | 223 |

8. United Midwest Savings Bank, N.A. | 182 |

9. Cadence Bank, N.A. | 157 |

10. KeyBank, N.A. | 133 |

*Source for both charts: U.S. Small Business Administration FY2021 volume through Dec 31, 2021.

Popular SBA lenders by total 7(a) loan approval amounts

Lender | Approval Amount |

1. Live Oak Banking Company | $307,149,100 |

2. Newtek Small Business Finance, Inc. | $219,101,500 |

3. The Huntington National Bank | $137,704,600 |

4. Celtic Bank Corp. | $106,125,900 |

5. Wells Fargo Bank, N.A. | $78,413,700 |

6. Enterprise Bank & Trust | $59,027,500 |

7. Cadence Bank | $57,017,800 |

8. KeyBank, N.A. | $55,938,600 |

9. U.S. Bank, N.A. | $50,156,200 |

10. Byline Bank | $47,329,000 |

Source: U.S. Small Business Administration, as of Dec. 31, 2021

5 SBA lending options to consider

1. SmartBiz

SmartBiz’s motto is “SBA loans made easy.” They are not a lender but a bank marketplace with the goal of matching you to lenders for SBA loans and bank term loans. They will help you prepare your loan application to match you with the bank most likely to fund your business. You can pre-qualify without impacting your credit score. (Note: SmartBiz is a Nav partner.) If you are looking for someone to help you find a lender that’s a good fit for your business, SmartBiz is a good choice.

2. Celtic Bank

Celtic Bank makes SBA loans nationwide. What makes Celtic Bank stand apart is its ability to work high leverage opportunities. Celtic Bank often finances 85-90% of business acquisitions, ground up construction, equipment financing and more. Therefore, its borrowers need to put less down, and can keep more capital on hand to help grow their businesses post-closing. Celtic Bank is a preferred lender and an Industrial Bank, which means it doesn’t hold deposit accounts or focus on consumer loans and doesn’t need the SBA’s permission to make credit decisions. The end result is a faster underwriting process with an average funding time of around 60 days.

3. Wells Fargo

Wells Fargo is often one of the top SBA lenders by both loan amounts and number of loans approved. They offer 7(a) and 504 loans and you do not have to be a Wells Fargo customer to apply. If you are looking for a national lender with significant experience in these types of loans, Wells Fargo can be a good choice.

4. United Midwest Savings Bank

United Midwest Savings Bank specializes in SBA Loans of $150,000 or less but also offers larger SBA loans. It provides a quick, initial credit decision—usually the same day as application. Loans can be funded in as little as 10 business days from application.

5. The Huntington National Bank

Huntington is the #1 lender nationwide for SBA loans in terms of number of loans made. It makes 7(a), SBA Express and 504 loans. Its primary focus is in its SBA footprint states of OH, MI, IN, WV, PA, KY, IL, WI, and FL and it is expanding into MN and TN in 2020. Huntington also offer SBA Practice Finance Loans in all states east of the Mississippi for dental, veterinary and medical customers. It has dedicated teams who specialize in the intricacies of SBA programs and all customers follow an identical triage process to be placed in the best product for them based on where they are in their business lifecycle, making Huntington a good choice for borrowers looking for an experienced SBA lender.

Are there SBA loans for you?

Business owners often wonder if there are SBA programs for their individual situations. Here are some common inquiries from entrepreneurs looking for this type of financing.

SBA loans for women

While there are no SBA loan programs specifically for women, the U.S. Small Business Administration does have a number of programs to support women-owned businesses. Female entrepreneurs can certainly apply for SBA loans and they may also want to explore the 8(a) Business Development Program for disadvantaged businesses. In addition, free resources and help for growing your business is available through Women’s Business Centers.

SBA loans for veterans

The Patriot Express program and 7(a) Veteran’s Advantage, loan programs specifically for veterans and other members of the military have expired, but the SBA continues to support veteran-owned businesses. Veterans can apply for SBA loans, of course, and receive free support and training through Veteran Business Outreach Centers. If an SBA loan isn’t the right fit, it is worth exploring other loan programs for veterans.

As part of the CARES Act, Congress permanently waived guaranty fees for certain SBA loans. For all SBA Express loans to veteran-owned small businesses approved on or after March 27, 2020, the upfront guaranty fee will permanently be zero.

SBA loans for minorities

While there are no specific SBA loan programs for minorities, those business owners can take advantage of free mentoring and educational programs through Small Business Development Centers (SBDCs) and SCORE. Consider the SBA loan programs detailed here and explore the 8(a) Business Development Program for disadvantaged businesses.

SBA loans for start-ups

Most SBA loan programs do not have a time in business requirement, but the borrower must demonstrate the ability to repay the loan which can be difficult for new businesses. In addition, it is not unusual for individual lenders to require two years in business to qualify. That means you may have a harder time finding an SBA loan for a startup. If your business is young, you may want to investigate the SBA Microloan program, which may have more flexible time in business requirements. Also consider other startup financing options such as business credit cards.

And of course, start building business credit as soon as possible so you’ll have more financing options available as your business grows!

SBA loans for business expansion

Virtually any SBA loan can be used to fund business expansion, but the SBA 7(a) and CDC 504 loan programs are the two types of loans most commonly used for that purpose. However, even an SBA Microloan can assist in business growth.

SBA debt relief program

Part of the CARES Act, the SBA Debt Relief Program authorized SBA to pay six months of principal, interest, and any associated fees for all 7(a), 504, and Microloans reported in regular servicing status (excluding Paycheck Protection Program loans). This was extended to loans approved by September 27, 2020. It also offered additional debt relief for borrowers beyond that initial six-month period.

SBA deferral on existing business loans

Deferment for Disaster Loans, including Economic Injury Disaster Loans (EIDL) was also offered due to the pandemic. With deferment the borrower can continue to make monthly payments but does not have to, and interest continues to accrue.

In March 2022, the SBA Administrator announced another deferment extension for all COVID-EIDL Loans approved in calendar years 2020, 2021, and 2022. Loans now have a total deferment of 30 months from the date of the Note. Interest will continue to accrue on the loans during the deferment.