Compare business loans for women: Funding options in 2026

Summary

- While you won’t likely find business loans exclusively for women, there are a number of loan programs that are available to small businesses.

- A variety of women-focused grants, microlenders, and support programs can help you find funding and options to grow your business.

- Your best funding option will depend more on factors such as your credit profile, time in business, revenue, and industry than on your gender.

- This guide walks you through the main types of loans, what lenders look for, how to compare offers, and where to find grants and other resources built for female entrepreneurs.

Editorial note: Our top priority is to give you the best financial information for your business. Nav may receive compensation from our partners, but that doesn’t affect our editors’ opinions or recommendations. Our partners cannot pay for favorable reviews. All content is accurate to the best of our knowledge when posted.

There are over 13 million women-owned businesses in the U.S. today, and that number is growing. From 2019 to 2023, women-owned businesses grew at a rate 94% higher than businesses owned by men. Despite that momentum, accessing business financing can still feel like an uphill battle.

Here's something important to know before you start searching: Business loans aren’t typically reserved exclusively for women. Typically loans don't come with a gender requirement — you qualify based on factors like your credit, revenue, time in business, and ability to repay. What does exist are programs and resources that specifically improve access to capital for women.

This guide will help you cut through the confusion. Here's how to use it: first, identify your funding goal. Then, compare the loan types that fit your situation. Next, prepare your documents. Finally, review costs before you accept the offer.

Whether you're just getting started, growing a business that's already generating revenue, or trying to bridge a cash flow gap, there's likely a path forward. It may not always be straightforward or smooth, but your goal is to take the next step.

Compare business loan options for women

When female entrepreneurs search for "business loans for women," they're often hoping to find a loan set aside just for them. The reality is a little different, and once you understand it, you'll have a clearer picture of where to focus your energy.

Most business lenders — banks, credit unions, online lenders, and the U.S. Small Business Administration — don't offer loans exclusively for women. In many types of lending, gender-based discrimination is not allowed, and small business loans are available to any qualified business owner, regardless of gender.

But organizations and lenders do sometimes realize there is a funding gap for women business owners. So some have developed programs to help women who qualify get loans, grants, and training to apply for funding.

This includes Community Development Financial Institutions (CDFIs), who are mission-driven lenders certified by the U.S. Department of the Treasury that often have more flexible criteria and pair their loans with coaching and technical assistance.

It includes Women's Business Centers (WBCs), which provide free counseling and can help you prepare for the application process. And it includes grant programs — money you don't have to repay — that are specifically open to women-owned businesses.

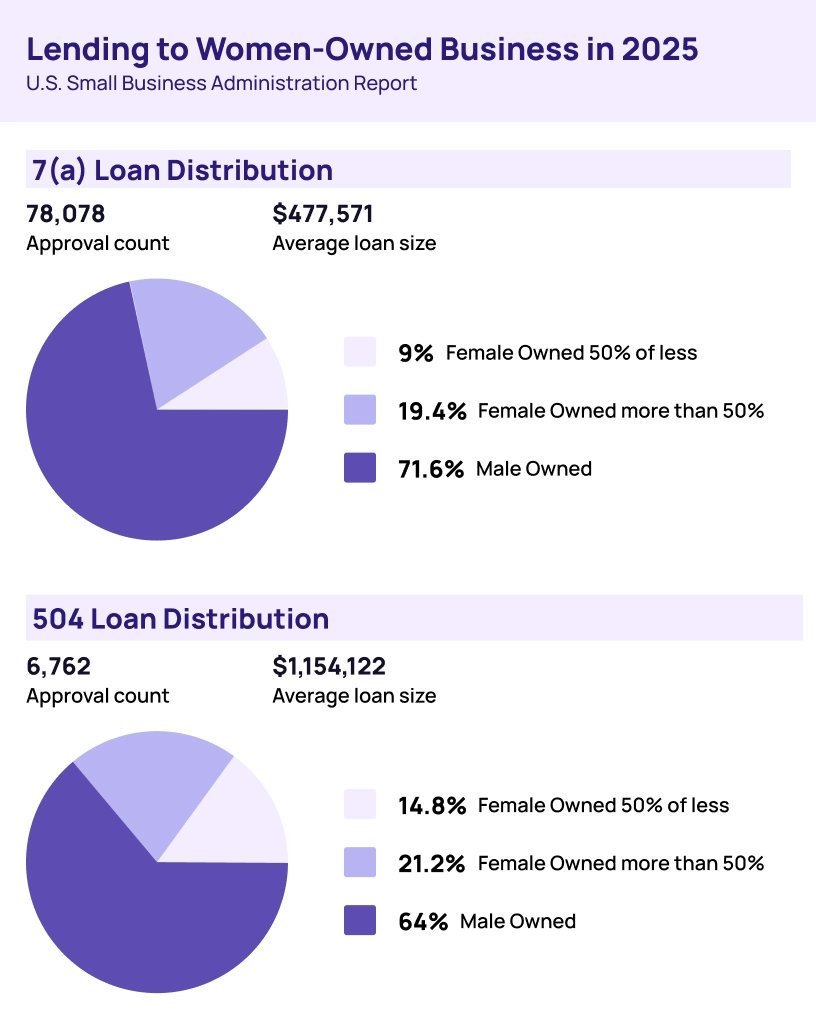

The SBA tracks lending to women-owned businesses and has made increasing that access a priority. Just over 19% of SBA-backed 7(a) and almost 15% of 504 loans went to women-owned businesses (51% or more) in fiscal year 2025. Women-owned businesses have also been major beneficiaries of federal contracting, receiving $30.9 billion in federal contracting dollars in the 2025 fiscal year.

Your best strategy is not likely to search for a women-only business loan. It's to find the right loan for your business, build the financial profile to qualify, and take advantage of the programs and resources available to support you.

Types of business loans for women-owned businesses

Before delving into the details of the main types of small business financing, here is an at-a-glance look at common funding goals and which types tend to fit best for different profiles.

Compare financing options by situation

Here are some common features of different lending types. Individual lender qualifications and requirements will vary. All financing options are subject to credit approval and eligibility requirements.

Goal | Common loan type | Typical funding speed | Typical requirements | Key tradeoffs | May be a good fit if... | Watch out for |

Lowest-cost financing | SBA loan | Weeks to months | Good credit, 2+ years in business, strong cash flow (or projections for start-ups) | Best terms; slower process; heavier documentation | You're well-qualified and can wait for funding | Lengthy approval timeline |

Fast funding | Online term loan or line of credit | 1-3 business days | Documented revenue, at least 6-12 months in business | Speed and accessibility; higher cost | You need money quickly and have strong revenue | High rates; frequent repayment schedules |

Startup or early stage | SBA loan, microloan loan, business credit card, crowdfunding | Weeks | Varies; more flexible than traditional banks | Smaller amounts; may include coaching | You need smaller amounts and traditional lenders have said no | Limited loan amounts |

Bad credit | CDFI loan, microloan, equipment financing | Weeks | Lower credit thresholds; mission-driven lenders | More flexibility; often smaller amounts | Your credit is limited but your business has potential | Higher-cost products from less reputable lenders |

Small loan amount | SBA microloan, CDFI loan, crowdfunding | Weeks | Varies by intermediary lender | Paired with technical assistance | You need smaller amounts and lenders have said no | Slower process than online lenders |

Equipment purchase | Equipment financing or leasing | Days to weeks | Equipment details; basic business financials | Equipment serves as collateral; accessible approval | You need specific equipment and prefer secured lending | Tied to equipment value; depreciation |

Working capital or cash flow gaps | Business line of credit | Days to weeks | Revenue history; credit score | Flexible access; interest only on amount drawn | Your cash flow is seasonal or uneven | Revolving debt if not managed carefully |

The process is fairly straightforward: identify your goal, investigate loan options that match, gather your documents (tax returns, bank statements, and business financials), compare total repayment cost across more than one lender, and confirm the repayment schedule that best fits your cash flow.

Bank term loans

Bank term loans refer to a loan for a fixed amount of money with a set repayment period made by a traditional financial institution like a bank or credit union. These loans often offer more predictable payments and lower rates than some online loans.

Traditional bank loans often require strong financials (revenue and enough cash flow to cover debt payments, including the new loan), a good credit profile (personal and/or business credit), and two years in business. (There are some bank loans for startups that have other strong qualifications.)

The application process can also take a few weeks or even a couple of months depending on the size and type of loan.

SBA loans and microloans

SBA loans can be among the most attractive financing options available to small business owners who qualify, but they're often misunderstood. Except for SBA Disaster loans, the SBA doesn't lend money directly to borrowers. Instead, it guarantees a portion of the loan to protect the lender, which reduces the risk for participating lenders and allows them to make loans to businesses that might otherwise not get access to similar financing.

The SBA's primary loan program is the 7(a) loan, which can be used for working capital, equipment, real estate, and other business expenses, with a maximum loan amount of $5 million. The 504 loan program is designed for major fixed asset purchases — like real estate or large equipment — generally with a maximum of $5 million for the SBA debenture. Both programs offer competitive rates and longer repayment terms than many conventional loans.

For newer or smaller businesses, the SBA microloan program offers loans up to $50,000. Microloans come through nonprofit intermediary lenders and are often paired with technical assistance, which means you may receive mentorship or business coaching alongside your funding. This makes SBA microloans especially useful for women earlier in their business journey.

The tradeoff with SBA loans is the application process. These loans often require more documentation than online options and take longer to close. Additionally, personal guarantees are required.

But for women-owned businesses that qualify, the terms can be hard to beat. In fiscal year 2025, SBA 7(a) and 504 lending to women-owned businesses totaled over $6.3 billion. To be eligible, your business generally needs to be for-profit, U.S.-based and owned by U.S. citizens, and unable to obtain credit on reasonable terms elsewhere.

Learn more about SBA loan requirements here.

SBA Loan by SmartBiz

For high cost projects with long repayment. No immediate funds needed.

Pros

- APR as low as 11.25% with monthly repayment plans up to 10 years

- Ability to be pre-approved and review terms and conditions before needing to provide a full list of financial documents.

Cons

- Lengthy application process (30-60 days) with lower approval odds

- Requires more documents than other Bank Loan products.

Funding Amount

Cost

Repayment Terms

Funding Speed

Business lines of credit

There will often be times when your business needs short-term financing, or smaller amounts of money, to smooth out cash flow or to take advantage of opportunities as they arise. A business line of credit may be the solution.

Once you’re approved for a business line of credit, you can access funds when you need them. You’ll get approved for a certain amount (your credit limit), borrow the amount you need, and only pay interest on the amount you borrow. There may be other fees such as annual fees or draw fees when you borrow from the credit line.

Banks, credit unions and online lenders may offer lines of credit, and costs and eligibility requirements can vary a lot depending on the lender and your qualifications.

Business lines of credit are the third most commonly used type of financing for small businesses without employees, according to 2025 Federal Reserve research, and that flexibility is probably the reason why.

Online term loans and lines of credit

Online lenders have expanded access to small business financing for businesses that are earlier in their business journey, have less documentation, or need money faster than a bank can offer.

These lenders can offer different types of financing such as lines of credit, term loans, invoice factoring, or business cash advances. If you're approved, funding may land in your bank account in as few as one to three business days.

That speed may come with tradeoffs. Online lenders may charge higher rates and may require more frequent repayment (including daily or weekly payments), though terms can be quite different among lenders.

When you borrow (and especially when you need money quickly), pause to review and understand the costs of the credit line.

Line of Credit by OnDeck

Monthly Payments and extended repayment terms (18 and 24 month terms) available. A line of credit can be a great asset to businesses who need capital on hand- fast. It allows you the flexibility to draw funds when you need it, and you only pay interest on what you use. Once approved, you can draw available funds quickly and easily without having to provide additional documentation.

Pros

- ○ Receive your money within seconds when you make a withdrawal — 24/7, even on nights and weekends.* ○ Withdraw what you need, when you need it

- You'll only be charged interest on the funds you draw.◊ ○ Only apply once and funds automatically replenish with timely payments.

Cons

- Not available in all states.

Funding Amount

Cost

Repayment Terms

Funding Speed

CDFI loans and community lenders

Community Development Financial Institutions, or CDFIs, are mission-driven lenders certified by the U.S. Department of the Treasury. Their main purpose is to expand access to capital in underserved communities — which often includes women-owned businesses, minority-owned businesses, and small businesses in lower-income areas.

CDFIs may be a strong fit for women-owned businesses that don't meet the requirements of traditional banks. They may offer more flexible underwriting criteria, looking at the full picture of your business rather than relying solely on traditional qualifications like credit scores and cash flow. With these loans, many CDFIs also provide technical assistance such as business coaching, financial counseling, and business education.

In 2023, CDFI program awardees originated more than $28.6 billion in loans and investments to businesses. To find a CDFI in your area, search the CDFI Fund's directory of certified institutions at cdfifund.gov.

Microloans

Microloans are smaller loans often created to help newer, smaller, or underserved businesses access capital when larger products aren't a fit, or when businesses have trouble getting access to capital.

The SBA microloan program, for example, offers loans up to $50,000 for working capital, inventory, supplies, furniture, fixtures, machinery, and equipment. The maximum repayment term is seven years, and proceeds can't be used for existing debt or real estate.

Beyond the SBA, many CDFIs and nonprofit organizations also offer microloans, sometimes with even more flexible terms. Amounts and terms vary by lender. Many programs pair their funding with mentorship and business education, which can be as valuable as the capital itself, particularly for early-stage businesses.

If you need a smaller amount and you're building your borrowing track record, a microloan can be a smart first step. Successfully repaying one may build your credit history (if the lender reports to credit bureaus) and can help position your business for larger financing down the road.

Equipment financing and leasing

If your business needs equipment — whether small like kitchen appliances or laptops, or large like vehicles or heavy machinery — equipment financing may be worth considering. The equipment itself typically serves as collateral, which can make approval more accessible than unsecured loans, even with imperfect credit.

With an equipment loan, you own the asset outright at the end of the repayment term. Equipment leasing works more like renting; you use the equipment for a set period and may have the option to purchase at the end. Leasing can work well for equipment that becomes outdated quickly, or when you want to preserve cash flow.

When evaluating equipment financing, start by getting a quote from the equipment vendor. Lenders will typically want to see documentation of the specific equipment you're purchasing along with your basic business financials.

Business credit cards

Business credit cards are the most popular type of financing and credit with more than half (55%) of businesses with no employees reporting that they use them, according to the Fed’s 2025 Report on Nonemployer Firms.

A business credit card helps keep your business and personal spending separate, which makes it easier to track business expenses and may help with managing short-term expenses, earn rewards, and even help business credit.Most cards offer a grace period that lets you pay the balance in full each month and avoid interest.

Business credit cards with 0% introductory APRs might be a good fit for planned, short-term purchases where you know you can pay off the balance before the promotional period ends.

And many small business credit cards report to commercial credit reporting agencies. If you pay on time and keep balances low, a business credit card can help you establish business credit.

Overall, business credit cards can work in your favor if you can keep your balances low and pay on time. Carrying a high balance can be expensive, and may affect your business credit scores.

One of the highest cash back rates available for small business cards.

Pros

- Attractive intro financing offer

- High rates of cash back for business spending

- No annual fee.

Cons

- No rewards bonus for initial spending

- Foreign transaction fees.

Intro APR

Purchase APR

Annual Fee

Welcome Offer

How to qualify for a business loan

Understanding what lenders look for helps you prepare before you apply, and gives you a realistic picture of which products may be in reach right now — and what you may want to look for in the future. Here's a breakdown of the main factors lenders often consider:

Credit reports and credit scores

Personal credit will often be checked for small business financing, especially if your business is newer and doesn't yet have a strong business credit profile. Most SBA and traditional bank loans require good to excellent personal credit scores. Some online lenders and CDFIs work with lower scores, but costs tend to be higher.

Business credit score typically matters more as your business grows. Lenders reviewing your business credit are evaluating your track record of on-time payments and responsible credit use. Building business credit takes time. Opening accounts that report to the business credit bureaus, like a business credit card or a net-30 trade account, is one place to start.

Business age

How long your business has been operating (time in business) can affect what options may be available. Many traditional bank loans require at least two years of operating history, though there are some traditional loans available to startups. Online lenders and CDFIs often work with newer businesses, though typically at higher costs or with smaller loan amounts. And crowdfunding may be an option at any stage of your business.

Revenue and cash flow

Revenue and cash flow are how lenders evaluate whether your business can cover existing debt payments plus the new loan payment. Some programs may work with businesses with limited revenue, particularly for startups with a credible business plan showing projected revenue that will cover the loan payments.

Profitability matters beyond revenue. Lenders want to confirm your business isn't spending more than it earns, and that a new loan won't push you into a position where you can't cover your costs.

Industry risk

Some industries are considered riskier than others. Beyond that lenders may have industries they prefer to lend into, and ones they don’t want to lend into. It is important that your business is properly categorized with the right NAICS or SIC codes to avoid programs that aren’t available. These codes are also used to calculate size standards for SBA loans.

Collateral

Some loans may require collateral. A secured loan requires you to pledge assets — business or personal — that the lender can go after if you default.

Another way lenders may help reduce their risk is by requiring a personal guarantee (PG) where you agree to pledge personal assets if your business can't pay back the debt. Not all loans require collateral or PGs— many online loans and CDFIs offer unsecured options — but traditional bank loans and many SBA lenders will require you to pledge collateral if it’s available.

Common small business loan requirements by loan type

Loan type | Typical credit profile | Business age | Revenue/ cash flow | Collateral/ pg | Notes |

Bank term loan | Good to excellent | 2+ years preferred | Strong; sufficient to repay comfortably | Often required | Stricter requirements; lower costs |

SBA 7(a) loan | Good to excellent | 2+ years preferred but startup funding is possible | Must demonstrate ability to repay from cash flow | Collateral required if available | Good loan terms; longer approval timeline |

SBA 504 loan | Good to excellent | 2+ years preferred | Must demonstrate ability to repay from cash flow | Required (fixed asset collateral) PG required | Real estate and major equipment purchases |

SBA microloan | Fair to good | Startups may qualify | Varies by intermediary lender | Varies by intermediary lender | Paired with technical assistance |

Business line of credit | Good to excellent (varies widely by lender) | 1+ year preferred | Steady revenue may be required | Unsecured but PG may be required | Good for managing uneven cash flow |

Online term loan | Fair to good (varies widely by lender) | 6+ months | Minimum monthly revenue often required | Usually not required | Faster; higher cost |

CDFI loan/microloan | Somewhat flexible | More flexible | Flexible but cash flow or projections should demonstrate ability to repay | Varies by lender | Mission-driven; technical assistance often available |

Equipment financing and leasing | Fair to good | Varies by lender or lessor | Basic business financials | Equipment serves as collateral | May be accessible even with fair credi |

How to compare business loan offers

While it may be tempting to just go with the first option you can get, choosing the right financing is key for the financial health of your business. It’s easy to just think about the monthly payment or the interest rate alone, but those may not be the only factors worth evaluating. Here’s what to look for:

Total repayment cost

Add up everything you'll pay back — principal, interest, and fees. This helps give you a true apples-to-apples comparison across offers.

Rates

Annual percentage rate (APR) is a standardized way to express borrowing cost and includes fees as well as interest. Some lenders — particularly online lenders offering short-term products — don’t disclose an APR and use a factor rate or other terminology instead.

A factor rate is not directly comparable to an APR. Research from the Federal Reserve confirms that many small business owners struggle to evaluate factor-rate pricing because it differs substantially from the standardized disclosures they're used to seeing.

Fees

Other fees to look for include origination fees, loan packaging fees, and any other upfront costs; draw fees or servicing fees on lines of credit; late payment fees; and prepayment penalties if you want to pay your financing off early.

Repayment terms

You want to match the term length to the way you’ll use the funds. A five-year term loan would be an expensive option if you just need a short-term loan to cover cash flow while you collect payment from a customer, for example. But it could be the right choice to finance an expensive piece of equipment.

Some types of financing like business cash advances may require you to make payments every week or even every business day. That may be a fit for quick short-term funding, but can put a strain on cash flow over time.

Funding speed

If you need money quickly, an SBA loan or traditional bank loan may take too long. But watch out: fast funding usually costs more.

Building credit

This may not be your prime concern, but it's worth asking whether the lender will report on-time payments to the business credit bureaus. If so, paying on time may help you build the credit profile you'll need to get different types of financing in the future.

Loan offer scorecard: Evaluate options

Feature | What good looks like | Questions to ask | Watch out for |

APR and total cost | Clear and disclosed upfront | What is the equivalent APR? What is the total repayment amount? | Confusing terms; discussion of payment amounts only |

Origination fees | Reasonable fees fully disclosed upfront | Are there origination, prepayment, or draw fees? | Fees revealed only at closing |

Repayment frequency | Monthly; or if weekly/daily adjusted for revenue | How often are payments due? For advances, will my payments be lower if revenue is lower? | Daily or weekly payments that may strain cash flow when sales are slow |

Term length | Appropriate for the loan purpose | What is the full repayment term? | Very short terms on large loan amounts |

Prepayment penalty | None or minimal | Can I pay off early without a penalty? | Large penalties for early repayment for a significant life of the loan |

Funding speed | Matched to need | How quickly will funds arrive after approval? | Pressure to decide before reading the full terms |

Credit reporting | Reports on-time payments to business credit bureaus | Does on-time payment get reported to business credit bureaus? | No reporting; repaying this loan won't help build your credit profile |

How to apply for a business loan

Applying for a business loan doesn't have to be overwhelming if you set aside the time to shop around.

Know what you need

Start by clarifying your goal. How much do you need, and what will you use it for? Lenders will ask, and a specific, well-thought-out answer signals that you've done your homework.

Check your credit

Review both your personal credit reports and scores and your business credit profile. If there are errors, dispute them.

Knowing your numbers helps you target the right lenders and avoid unnecessary hard inquiries from lenders whose minimums you don't meet. Nav's Credit Health tool lets you monitor business and personal credit in one place. Nav is not a lender or a credit bureau. Credit information is provided by third-party sources.

Gather your documents

Many lenders will ask for recent business bank statements (three to six months). Others may also ask for a combination of personal and business tax returns (typically two years), a profit and loss statement, and/or a balance sheet.

You may also need a business license and legal formation documents, and a description of how you'll use the funds. SBA loans require additional documentation, and your lender will specify exactly what their program needs.

Research your options

Use the comparison table earlier in this guide to identify two or three loan types that may fit your situation.

Apply and compare offers

Don't stop at the first offer you receive. If possible, apply to multiple lenders and compare total repayment cost — not just the monthly payment. Use the loan offer scorecard above to evaluate each one.

Make sure you carefully review the full terms before signing. Confirm the repayment frequency, total cost, and any penalties before you commit. Don’t be afraid to ask questions: legitimate lenders will be happy to answer them.

Grants and alternative funding for women entrepreneurs

Loans may not be the only path to funding. Depending on where your business is and what you're trying to accomplish, grants, crowdfunding, or equity financing may be worth exploring — either instead of or alongside a loan.

Women-owned business grants

A grant is money you don't have to repay. Grants for women-owned businesses can come from private foundations and corporations. Unlike a loan, there's no interest rate and no repayment schedule.

Don’t expect this to be an easy source of funding. Most grant programs fund only a handful of recipients per cycle, and applications can be time-intensive. Most programs define a women-owned small business as one that is at least 51% owned and controlled by one or more women. Beyond that, eligibility varies widely by location, industry, business stage, and revenue level all factor in.

Examples of some of the more accessible recurring programs include the Amber Grant (WomensNet), which awards $10,000 monthly and $50,000 in year-end grants, and the HerRise Microgrant, which awards $1,000 monthly to U.S.-based businesses with under $1 million in revenue. For growth-stage businesses with stronger revenues, competition-based programs like the Cartier Women's Initiative offer $30,000 to $100,000 for impact-driven businesses.

Read: Grants for women-owned businesses

True federal grants for for-profit small businesses are less common than you may expect. Most federal funding is tied to specific programs such as research and development, agriculture, defense, or particular industries. That said, the federal government funds resources like Women's Business Centers and Small Business Development Centers, which can help you identify local or state-level opportunities. Grants.gov is the official federal grant database and is free to search.

Watch out for scams. Legitimate grant programs publish their eligibility rules, past winners, and application process transparently. Be wary of any program that guarantees an award, requests large upfront fees, or asks for sensitive financial data through an application form.

Crowdfunding and community funding

Crowdfunding may be an effective path for women-owned businesses.

There are three main types of crowdfunding small business owners may want to consider:

- Rewards-based crowdfunding on platforms like Kickstarter let you raise money in exchange for early access, products, or recognition. You don’t take on debt or give up equity.

- Lending-based crowdfunding offers a loan you must repay. Kiva.org offers 0% interest loans no interest, though eligibility requirements apply and funding depends on crowdfunding participation) up to $15,000 in the U.S. with no fees, making it one of the most accessible funding options for businesses that don't qualify for traditional loans.

- Equity or investment-based crowdfunding (Regulation crowdfunding) allows businesses to raise money online from investors within specific limits.

According to RegulationCF data from Crowdfund Capital Advisors, LLC from May 15, 2016 to March 22, 2026:

- Offerings: 42% of all RegCF offerings had at least one woman and/or minority founder

- Capital: 36.5% of all the investments went to issuers that had at least one woman and/or minority founder

- Checks written: 40.6% of all the checks written went to issuers that had at least one woman and/or minority founder

And of the 578 online Reg CF and Reg A deals in 2023, 157 raises, (27% of them) featured at least one female founder, according to Kingscrowd.

Crowdfunding campaigns are more likely to succeed when there's a clear offer, proof of concept or traction, a marketing plan to promote the campaign, and a realistic timeline. Solid preparation, including building an audience before you launch, can dramatically increase your chances of success.

Investors and accelerators

If your business is high-growth and scalable, equity financing — bringing in investors in exchange for ownership — may be worth exploring. This is fundamentally different from debt: you don't repay investors directly, but you do give up a portion of ownership and, often, some decision-making control.

Options may include angel funding, venture capital (VC) funding, or Regulation CF or Regulation A crowdfunding mentioned earlier.

According to PitchBook's 2025 All In report on female founders in the VC ecosystem, female-founded companies raised a record $73.6 billion in U.S. venture capital in 2025, with female-founded companies accounting for 27.7% of total U.S. VC deal value — the first time this metric has topped 25%. Even so, all-female-founded companies continued to see declines in both deal count and deal value, and decision-making roles at VC firms with $50 million or more in assets under management remain at 82% male.

Investors typically look for businesses with strong traction, scalable margins, and a clear path to significant growth. Accelerator programs — which often include mentorship, education, and a small amount of funding in exchange for equity — can be a good entry point if your business is in an earlier stage but you have a compelling idea.

Equity financing isn't the right fit for every business. If you're building a stable, sustainable small business rather than a high-growth startup, then loans, grants, or CDFIs are likely a better match.

High-cost options: proceed carefully

Not all funding options are created equal, and some can trap you in a cycle that's hard to escape. Merchant cash advances (MCAs) and factoring are two of the most common higher-cost products small business owners turn to when other options aren't available.

A merchant cash advance gives you an upfront sum in exchange for a percentage of your future sales, typically repaid through automatic daily debits from your bank account. It can be fast and easy to get approved and funded, but also expensive. MCAs typically state a factor rate rather than an APR, which makes it easy to underestimate what you're actually paying.

Factoring works somewhat similarly. You get advanced an amount based on your outstanding invoices, and then the factoring company often collects and takes their cut. It’s common in certain industries such as trucking, healthcare, and certain types of manufacturing.

Before considering these products make sure you understand the total amount you'll repay and how payments will impact your cash flow. A business loan calculator can help you translate the cost to an Annual Percentage Rate (APR) so you can compare it to other types of financing, such as a line of credit or even a business credit card.

Women-owned business resources and certification

Don’t feel like you have to navigate the funding process alone. Federally funded resources across the country help women-owned and underserved small businesses build their financial foundation, prepare for financing, and connect with the right opportunities.

On the certification side, the WOSB Federal Contract Program is worth understanding if your business could potentially work with the federal government. Women-owned businesses received a historic $30.9 billion in federal contracting dollars in the most recent fiscal year. To compete for contracts set aside under the program, your business needs to be certified. Apply at no cost through the SBA's MySBA Certifications portal.

Organization/program | How it helps | Who it's for | What to prepare |

Women's Business Centers (WBCs) | Free and low-cost counseling, training, access to capital guidance | Women entrepreneurs at any stage | Business overview; questions about financing or business planning |

Small Business Development Centers (SBDCs) | One-on-one counseling, loan preparation, financial education | All small business owners | Business and financial documents |

SCORE | Free mentorship from volunteer business advisors | All small business owners | Business questions or a draft business plan |

WOSB Federal Contract Program | Access to federal contracts set aside for certified women-owned businesses | At least 51% women-owned, for-profit, U.S.-based businesses | Business documentation; apply at certifications.sba.gov |

CDFI Fund locator | Find mission-driven lenders with flexible underwriting in your area | Underserved businesses; women-owned businesses | Basic business information and financials; search CDFIfund.gov |

Grants.gov | Search federal grant opportunities by eligibility, agency, and industry | Businesses meeting program-specific eligibility requirements | EIN; SAM.gov registration for federal grant applications |

Nav can help

Save time researching and access your best lending options from Nav’s portfolio of 25+ trusted partners. Apply for funding options with confidence.

Frequently asked questions

Rate this article

This article currently has 18 ratings with an average of 5 stars.

Gerri Detweiler

Education Consultant, Nav

Gerri Detweiler has spent more than 30 years helping people make sense of credit and financing, with a special focus on helping small business owners. As an Education Consultant for Nav, she guides entrepreneurs in building strong business credit and understanding how it can open doors for growth.

Gerri has answered thousands of credit questions online, written or coauthored six books — including Finance Your Own Business: Get on the Financing Fast Track — and has been interviewed in thousands of media stories as a trusted credit expert. Through her widely syndicated articles, webinars for organizations like SCORE and Small Business Development Centers, as well as educational videos, she makes complex financial topics clear and practical, empowering business owners to take control of their credit and grow healthier companies.

Robin Saks Frankel

Managing Editor

Robin has worked as a personal finance writer, editor, and spokesperson for over a decade. Her work has appeared in national publications including Forbes Advisor, USA TODAY, NerdWallet, Bankrate, the Associated Press, and more. She has appeared on or contributed to The New York Times, Fox News, CBS Radio, ABC Radio, NPR, International Business Times and NBC, ABC, and CBS TV affiliates nationwide.

Robin holds an M.S. in Business and Economic Journalism from Boston University and dual B.A. degrees in Economics and International Relations from Boston University. In addition, she is an accredited CEPF® and holds an ACES certificate in Editing from the Poynter Institute.