Summary

- SBA microloans may provide up to $50,000 to qualified small businesses.

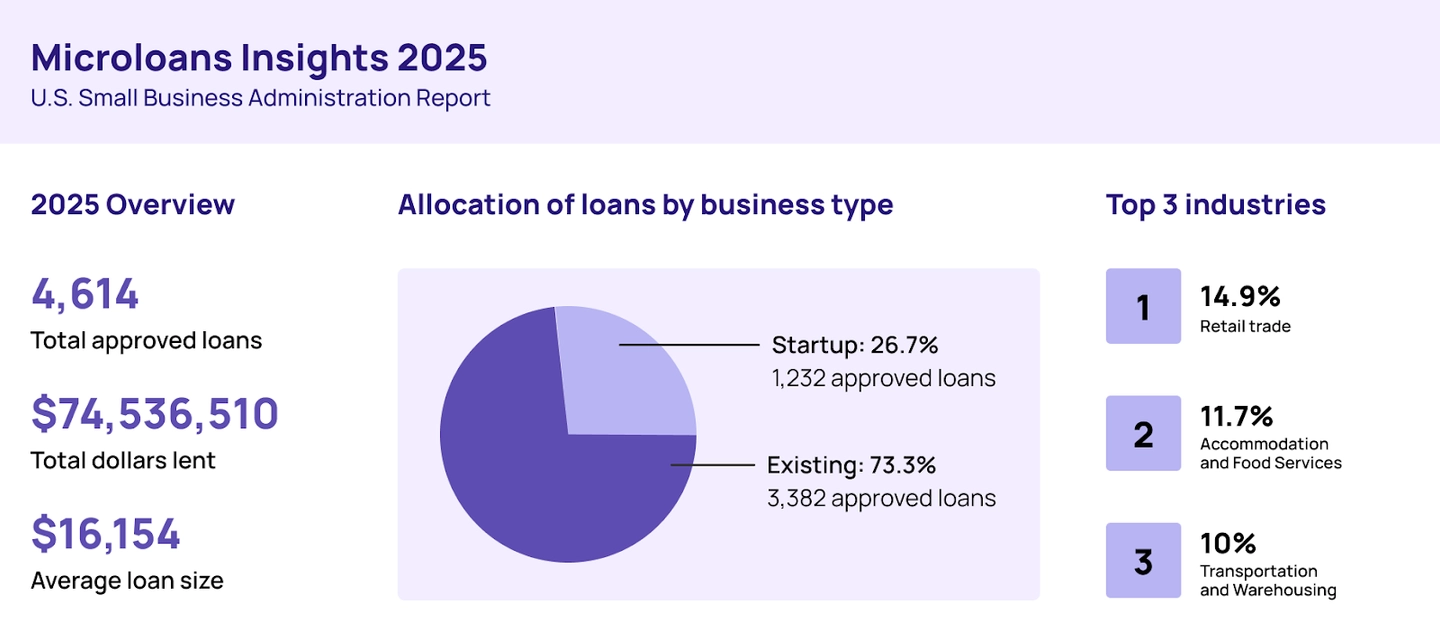

- The average loan was about $16,000 for Fiscal Year 2025, according to the SBA’s Microloans Segment Report.

- Free business training and technical assistance is part of the program.

- Loans come from intermediary lenders, not directly from SBA.

Editorial note: Our top priority is to give you the best financial information for your business. Nav may receive compensation from our partners, but that doesn’t affect our editors’ opinions or recommendations. Our partners cannot pay for favorable reviews. All content is accurate to the best of our knowledge when posted.

SBA microloans might be your answer if you’re a small business owner who needs a relatively small amount of capital who is having trouble finding a lender willing to work with you.

These loans may offer up to $50,000 and come with something many lenders don't provide: assistance to help your business succeed. Created specifically for entrepreneurs who struggle to find funding elsewhere, the SBA microloan program helped over 4,500 businesses access financing in FY 2025.

What are SBA microloans?

SBA microloans are small business loans funded through SBA-approved intermediary lenders. The SBA provides funds to specially designated nonprofit organizations — usually community-based groups focused on economic development such as Community Development Financial Institutions (CDFIs). These intermediaries then loan that money to qualified small businesses in their service areas.

The program launched in 1991 as a demonstration project to help underserved entrepreneurs. Women business owners, minorities, veterans, and low-income individuals often face barriers when seeking traditional financing. Microloans were designed to help fill that gap and support small business growth.

SBA microloan calculator

SBA microloan amounts, rates & terms

Loan amounts

The maximum SBA microloan program is $50,000 but the average loan amount across all industries was $16,131 for the 2025 fiscal year.

If your business needs to borrow more than $50,000, you may want to explore other SBA loan programs, such as 7(a) or 504 loans.

Interest rates

SBA microloan rates are set in two steps. One depends on the intermediary (lender), and the other depends on the loan size.

Step 1: SBA sets the rate charged to the intermediary

The SBA starts with the 5-year U.S. Treasury rate, rounded to the nearest 1/8 of 1%.

The SBA then applies a discount based on the intermediary’s historical average loan size:

If the intermediary’s average loan size is $10,000 or less, the rate is discounted by 2%.

If the intermediary’s average loan size is more than $10,000, the rate is discounted by 1.25%.

Step 2: Set the maximum rate the borrower can be charged

The maximum borrower rate is the intermediary’s SBA rate, plus a fixed markup that depends on the loan amount:

- Loans of $10,000 or less: intermediary rate + 8.5%

- Loans over $10,000: intermediary rate + 7.75%

See current SBA microloan rates here.

*Data sourced from publicly available U.S. Small Business Administration reports. This content is not affiliated with or endorsed by the SBA.

Repayment terms

Your microloan term may be able to be extended up to seven years maximum. No balloon payments are allowed.

Funding timeline

The process will often take 30–90 days, but timelines vary by intermediary, documentation, and workload. Several factors can affect how quickly you'll receive funds: lender workload and staffing, how complete your application is, whether you need additional documentation, and your qualifications.

Need funds faster? Online lenders can fund in days, but you may pay higher rates. An SBA Express Loan might offer a middle ground. If you qualify, a credit card with a 0% intro APR may be another option for short-term funding.

SBA Loan by SmartBiz

For high cost projects with long repayment. No immediate funds needed.

Pros

- APR as low as 11.25% with monthly repayment plans up to 10 years

- Ability to be pre-approved and review terms and conditions before needing to provide a full list of financial documents.

Cons

- Lengthy application process (30-60 days) with lower approval odds

- Requires more documents than other Bank Loan products.

Funding Amount

Cost

Repayment Terms

Funding Speed

SBA microloan eligibility requirements

To qualify for an SBA microloan, your business must be a for-profit small business (startup, newly established, or growing) or a nonprofit childcare center. You need to qualify as small under SBA size standards for your industry and operate in the same area as the intermediary handling your loan. You can’t operate in an ineligible industry.

For loans over $20,000, microborrowers must pass a "credit elsewhere" test. This means you can't get similar financing from non-federal sources on reasonable terms. The lender will help you navigate this requirement.

Credit score requirements

The SBA doesn’t publish a minimum score for the program, but intermediaries have their own requirements and will review credit. This is one of the program's potential advantages. Microloan borrowers may have a limited credit history or lower scores than typical commercial loan applicants.

If you have credit problems in your history, be prepared to explain what happened and what you've done to improve your situation. The lender wants to try to ensure your loan will be successfully repaid.

Collateral requirements

Collateral is required if available, but lenders can be flexible.

SBA guidelines encourage microloan lenders to "be creative in their definitions of acceptable collateral." Since many microborrowers don't have traditional assets to pledge, lenders may accept equipment, inventory, or other business assets you're purchasing with the loan.

What can you use SBA microloans for?

Allowed uses

Microloan proceeds can fund working capital to cover payroll, rent, utilities, and day-to-day operating expenses. You can purchase equipment like machinery, computers, or tools you need to operate.

The loans may be used for furniture and fixtures such as desks, shelving, displays, or other furnishings. You can stock inventory or buy supplies and raw materials.

If you operate a home-based business, you may renovate or improve the portion of your home dedicated specifically to your business. The lender may even allow you to use the proceeds to refinance debt in limited circumstances, as permitted under SBA SOP guidance if it puts your business in a better financial position.

Prohibited uses

You cannot use microloan funds for real estate purchases. You can't make payments to business owners or associates except for fair compensation for actual work performed. Paying delinquent taxes is prohibited with limited exceptions if you have an IRS approved payment arrangement.

Pros and cons of SBA microloans

Pros

- If you've been turned down for traditional business loans, this program may help you get the funding your business needs. It was created specifically for borrowers who struggle to find other funding sources.

- Longer repayment terms (up to seven years) can help too. Lower monthly payments mean you can invest more cash back into growing your business.

- Interest rates compare favorably to many alternatives. Business credit cards and online loans for newer businesses may charge significantly more.

- Every microloan comes with free business training and technical assistance. You may get help with business planning, marketing, bookkeeping, and or management.

Cons

- The $50,000 maximum loan amount may not be sufficient for businesses that need larger loans to expand. (Also keep in mind the average microloan amount is less than half the maximum amount.)

- Not all business owners may want to participate in required business training.

- Finally, the biggest hurdle is that it can be hard to find a microlender that is a fit for your business. The intermediaries who make these loans tend to be smaller organizations and may not serve all communities or industries.

How to apply for an SBA microloan

1. Find an SBA microloan lender

Start by searching the SBA lender directory at SBA.gov. Enter your zip code to find intermediary lenders serving your area.

Geographic limitations matter here. Each intermediary operates in specific regions. You might need to expand your search or consider other loan options if no lender serves your location.

Contact multiple lenders if possible. Rates, requirements, and services vary between organizations.

2. Prepare your application

Unlike other SBA loans that carry very specific requirements, under this program, the lender (intermediary) is responsible for deciding whether the borrower qualifies. Since

requirements vary by lender, ask your specific intermediary what they need before you start compiling documents.

As with all small business loans, though, it’s often helpful to have your accounting up to date and to use a dedicated business bank account (rather than a personal bank account) so you can clearly document business income and expenses.

3. Complete required training

Your lender may require business training before or after loan approval.

This isn't busy work. The technical assistance helps ensure you're ready to manage the loan and grow your business successfully. Topics might include cash flow management, basic accounting, marketing fundamentals, and industry-specific guidance.

4. Submit and follow up

Turn in your complete application package and stay in contact with your lender.

During underwriting, the lender may review your credit, business plan, and ability to generate enough revenue to repay the debt. They may request additional information or clarification. And if they do, be prepared to respond right away.

How SBA microloans work

The SBA doesn't loan money directly to you with a microloan. Instead, SBA provides funds to nonprofit intermediary lenders — usually community development organizations — who then make loans to small businesses.

This model exists for good reason. Local nonprofits understand their communities and know the challenges entrepreneurs face in their regions, as well as the local business landscape.

Flexible underwriting

Your intermediary lender reviews your application and makes the lending decision. They set the specific interest rate (within SBA guidelines) and determine any collateral requirements. The lender provides required business training and technical assistance throughout your loan, services your loan, and collects payments.

The SBA backs the loan, which allows the intermediary to take on borrowers traditional banks won't. But that doesn’t mean they can fund everyone who wants a loan. Funds are limited, and intermediaries with high losses won’t be able to continue in the program.

Creative collateral

While many small business loans require collateral, especially for newer businesses, here lenders can be more flexible. Program guidelines acknowledge that many microborrowers lack traditional collateral. Lenders are encouraged to think creatively — accepting equipment you're purchasing with the loan, inventory, or even personal guarantees in some cases.

Help for your business

Every microborrower must receive business training and technical assistance. Some lenders provide training for non-borrowers, too.

Your lender provides this free of charge. Expect help with business plan development, financial management, marketing, and ongoing counseling throughout your loan term.

This mentoring relationship can help make microloans successful. Many borrowers are new to self-employment or business ownership. Regular guidance can help them avoid common pitfalls.

SBA microloan alternatives

If you can’t find a microloan program that is a fit for your business, you’ll need to consider other options. Here’s where to start:

Other SBA loan programs

The SBA's primary loan program, the 7(a), offers up to $5 million with longer terms (up to 25 years with extensions). Requirements are stricter than microloans, but businesses that qualify access significantly more capital.

SBA Small Loans offer up to $350,000 and SBA Express loans max out at $500,000. They can be a good middle ground if you need more than a microloan can provide but want reasonable rates.

For purchasing fixed assets like real estate, buildings, or major equipment, SBA 504 loans often work well. Loan amounts start where microloans end.

There are a number of different SBA loan programs that serve different purposes:

7(a) loan program | Maximum loan amount |

7(a) standard | $350,001 to $5 million |

7(a) Small Loan | $350,000 |

SBA Express | $500,000 |

Export Express | $500,000 |

Export Working Capital | $5 million |

International Trade | $5 million |

Manufacturers’ Access to Revolving Credit (MARC) | $5 million |

CDC 504 loans | $5 million (SBA debenture) |

Microloan | $50,000 |

For more information, read Nav’s guide to SBA loans.

Non-SBA small business financing

There are other types of financing you may want to consider, including:

Vendor terms: Suppliers may let your business buy now and pay later. Vendor terms typically range from net-10 to net-180 (net-30 gives you 30 days to pay). Personal credit checks are rarely required.

Lines of credit: A business line of credit gives you access to a set credit amount that you can borrow against as needed. As you repay funds, they become available to borrow again—similar to how a credit card works. Lines of credit work well for short-term financing needs.

Business credit cards: Business credit cards offer quick access to credit, often with rewards and perks. They're frequently available to newer businesses as long as the owner has good personal credit and sufficient income. Many business credit cards also report to business credit bureaus, helping you build your business credit score.

Crowdfunding: Several types of crowdfunding are available to small businesses, including loan-based (you repay investors with interest), rewards-based (backers get products or perks), and investment-based (investors get equity in your company). Each type offers unique advantages depending on your business needs.

Equipment financing or leasing: Get equipment — from computers to heavy machinery — while preserving cash flow. You may also qualify for tax benefits depending on how it’s structured.

Frequently asked questions

Rate this article

This article has not yet been rated

Gerri Detweiler

Education Consultant, Nav

Gerri Detweiler has spent more than 30 years helping people make sense of credit and financing, with a special focus on helping small business owners. As an Education Consultant for Nav, she guides entrepreneurs in building strong business credit and understanding how it can open doors for growth.

Gerri has answered thousands of credit questions online, written or coauthored six books — including Finance Your Own Business: Get on the Financing Fast Track — and has been interviewed in thousands of media stories as a trusted credit expert. Through her widely syndicated articles, webinars for organizations like SCORE and Small Business Development Centers, as well as educational videos, she makes complex financial topics clear and practical, empowering business owners to take control of their credit and grow healthier companies.