CREDIT HEALTH

Get clear on your credit

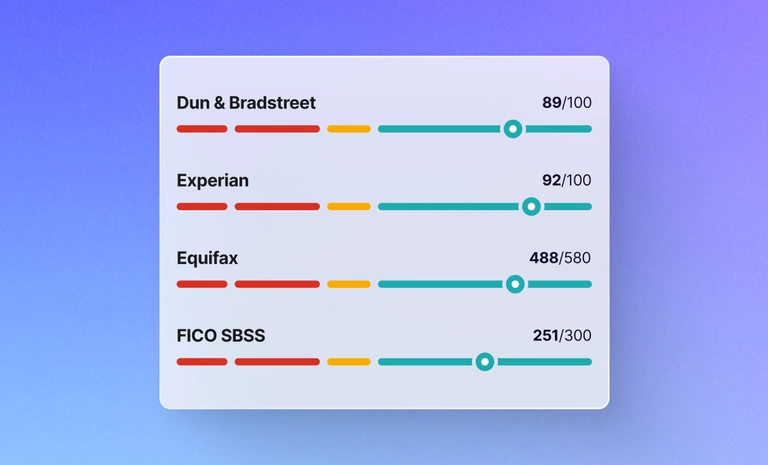

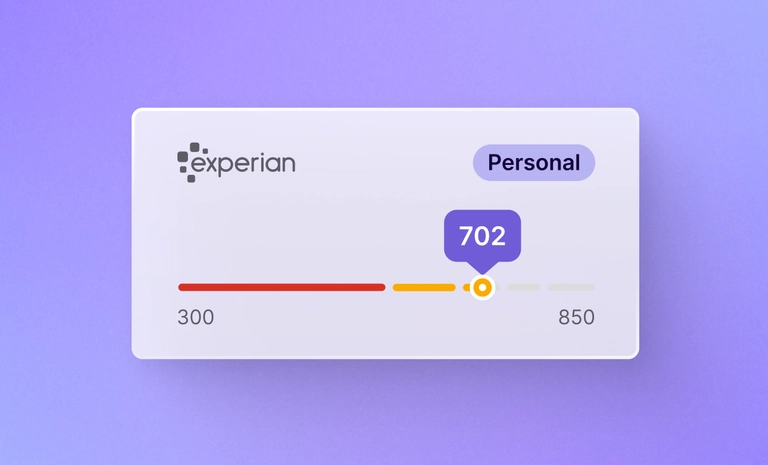

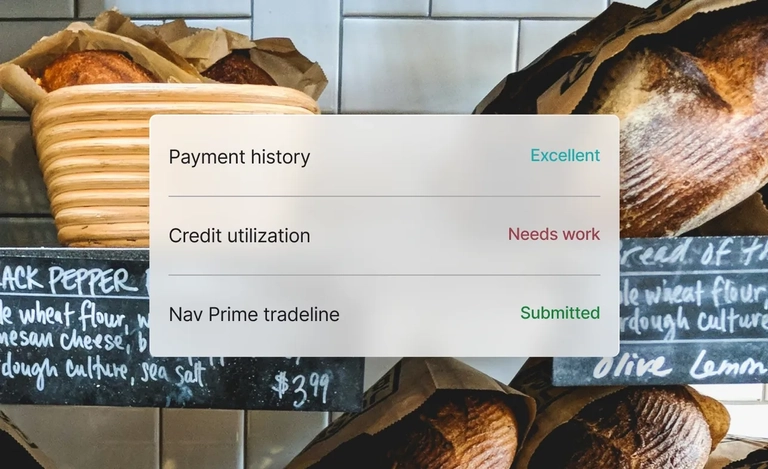

Nav has given 2.7 million business owners the credit details they need to build and grow. See where you stand with the major bureaus for free.

Join Nav prime

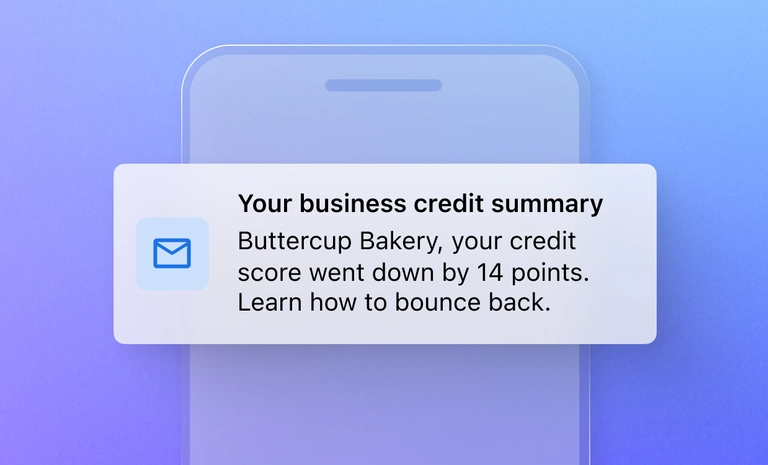

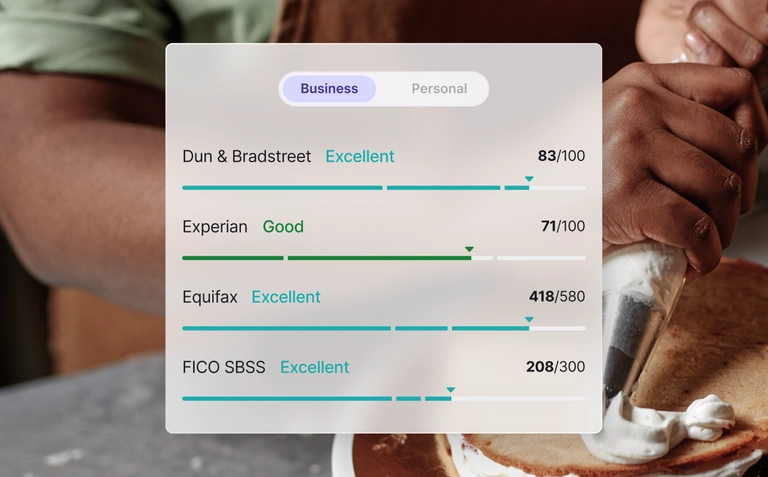

Unlock your scores and start building business credit

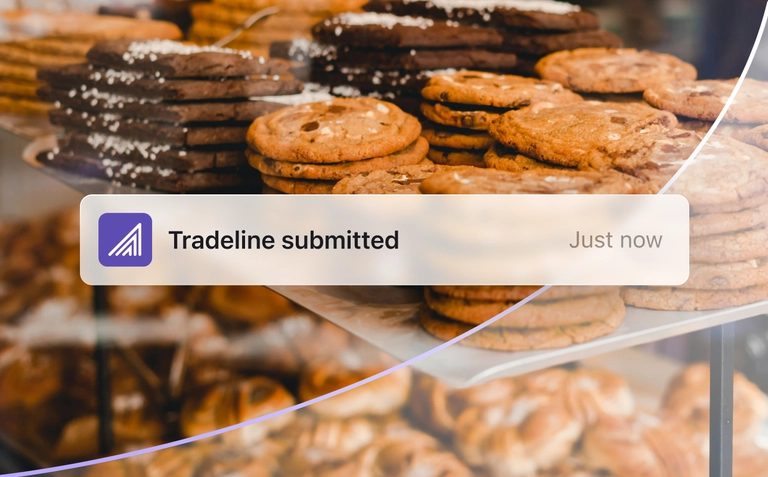

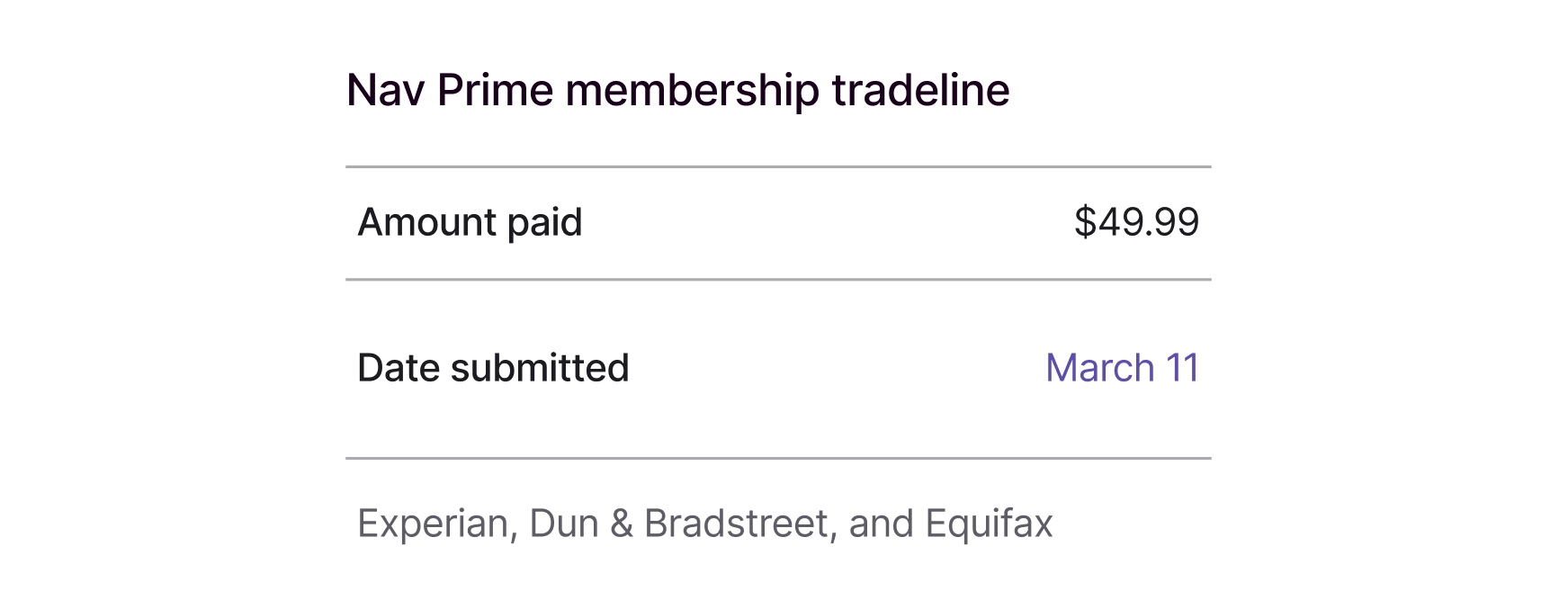

Get enhanced insights and clear next steps to help you build business credit with confidence, all in one membership. Plans start at $39.99.