Small business credit cards offer myriad benefits: rich rewards and flexible credit lines with credit limits that are often higher than on personal cards. Plus, there’s an added bonus that small business owners don’t always recognize at first: A business credit card may help you build business credit.

Getting one of these cards may help put your business on the map when it comes to building business credit, provided the card issuer reports information to commercial credit agencies. Not all cards have the same policy when it comes to reporting to business credit bureaus, though, and it’s important to understand how each one works. (In a separate article, we explain how business credit cards may affect a business owner’s personal credit.)

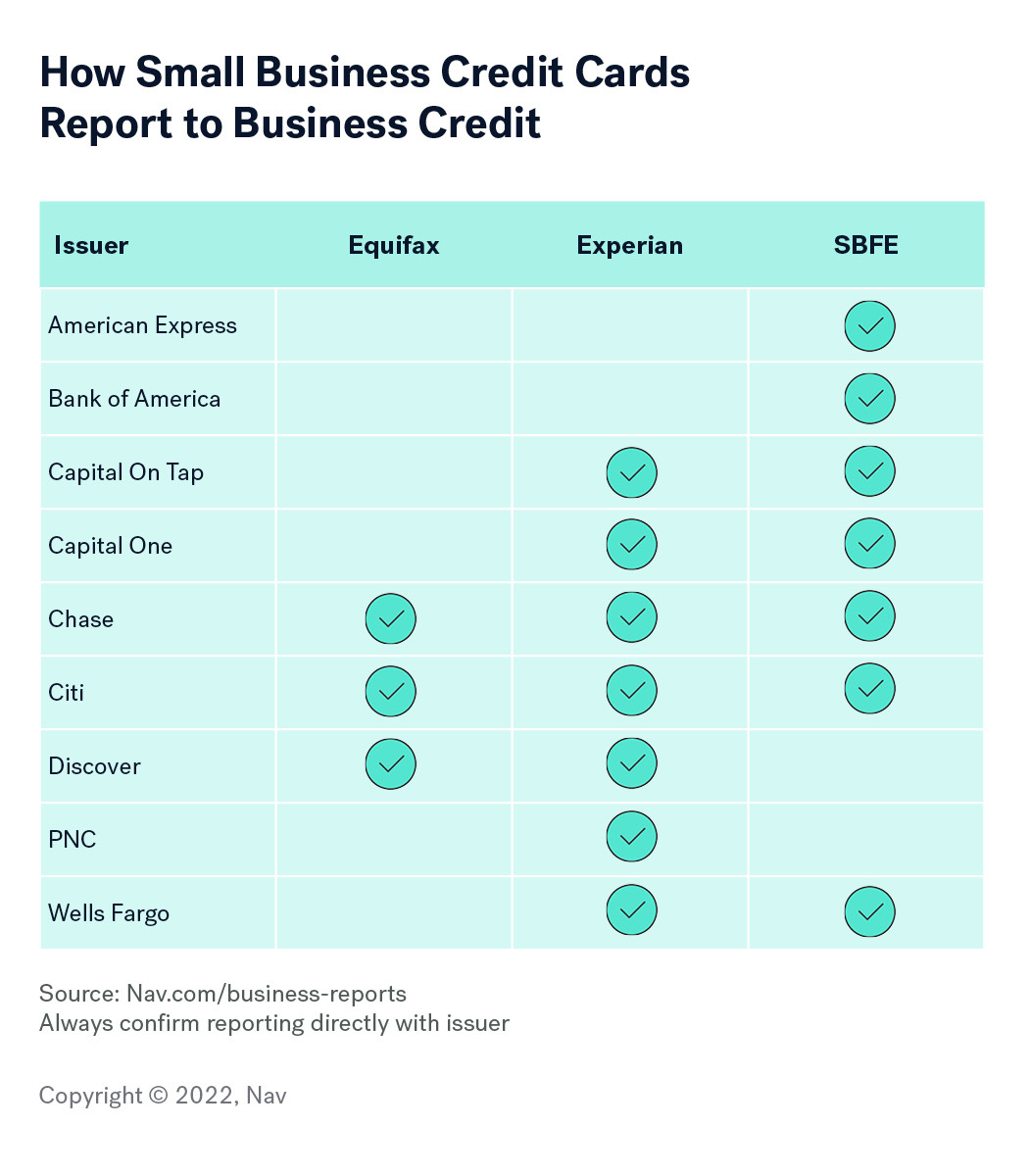

How Business Credit Cards Report to Business Credit

There are a number of commercial credit reporting agencies in the U.S. Separately, the Small Business Financial Exchange (SBFE) serves as a repository of business credit information for its members, which include major financial institutions and lenders of all types that provide financing to small businesses.

The SBFE doesn’t compile or sell credit reports. Instead, it works with SBFE Certified Vendors, which are credit reporting agencies that are permitted to include credit information reported to the SBFE exchange in the reports they sell to members of the SBFE. SBFE Certified Vendors currently include major business credit bureaus like Equifax and Experian.

Credit reporting is entirely voluntary. No issuer is required to report information to credit bureaus, whether it’s personal or commercial credit information. And with business credit in particular, it can be difficult to find lenders and vendors that report. That’s why having a credit card that reports can be so helpful.

We reached out to major business credit card issuers for details on where they report small business credit card payment history. The chart below summarizes findings.

Information may also appear on credit reports from bureaus not listed below. One reason is due to the SBFE Certified Vendor model. Information reported to SBFE may also be included in reports compiled by SBFE Certified Vendors.

Issuer policies may change. Be sure to check with the issuer for current information on credit reporting policies.

How to Get a Business Credit Card to Build Credit

Small business credit cards are available to small business owners with good personal credit scores and sufficient income to meet the issuer’s minimum income requirements. A few important qualifiers to keep in mind:

- You will almost always need to provide your social security number when you apply, and there will be a personal credit check. Most issuers require at least a good personal credit history to qualify, and that usually means you need a FICO score of 650-680 or above to qualify. Some cards require excellent personal credit scores to qualify.

- There is almost always a personal guarantee required as well. You may be asked for some basic information about your personal finances (such as income).

- Startups, freelancers, contractors and sole proprietors may qualify as long as you meet the issuer’s requirements.

- It’s a good idea to get an Employer Identification Number before you fill out a credit card application to help ensure your new card gets reported properly under the name of your business.

What to Look For in a Credit Card to Build Credit

Business owners looking for a credit card have many choices. If your primary goal is to build business credit, then you’ll want to find a card that reports to multiple business credit bureaus. On-time payments can help your business build credit.

Other secondary goals to consider:

Rewards: Think of all the money you spend in your business, then think about all the credit card perks you may earn if you use a credit card to pay for those business expenses. For many businesses, it adds up quickly.

Cash back rewards are universally popular, as business owners can always use cash! Some cards offer bonus cash back for spending in bonus categories (such as office supply stores) so it’s helpful to review your typical business purchases before you choose a card. Points are also popular, and are most often used for travel, but can be redeemed for other rewards such as gift cards.

Financing: Don’t overlook the fact that a business credit card is essentially a line of credit your business can use when needed. Unlike a business loan, no one will question why you need financing. Some cards even offer balance transfers or introductory APRs of 0% for a year or longer. That low-cost financing can be very helpful to new businesses or any business that is experiencing tight cash flow.

It’s essential, though, that you use this financing for essential business spending. Otherwise you may find your business with a credit card balance at a high interest rate once the introductory rate expires.

5 Best Business Credit Cards & Charge Cards to Build Business Credit

If your goal is to build business credit, while enjoying the benefits small business credit cards offer, here are several options to consider:

1.

Capital on Tap reports to two the major commercial credit reporting agencies, making it a good choice if you want to build business credit. The is a particularly attractive card. It offers a sign-up bonus: for a annual fee.

Ongoing reward points are solid as well:

2.

Divvy reports to the SBFE and a major business credit bureau. streamlines spend management by combining corporate cards with free expense management software. It gives admins complete control over employee spending with spending limits that can be adjusted in seconds. Divvy can help your business eliminate expense reports, spend within your budget and build business credit.

The annual fee is . And the rewards program is competitive:

3.

If you’re looking for a straightforward cash back rewards card, the is a solid choice. American Express reports business credit cards to the SBFE, which means that information may appear on multiple business credit reports, depending on the report purchased by a lender.

You can get which make this card appealing for businesses looking for low-cost financing. There’s also a welcome offer:

Rewards come in the form of cash back.

Amex cards require excellent credit to qualify.

4.

Capital One reports to the SBFE and Experian Small Business. (It should be noted that it may report activity to the cardholder’s personal credit. Learn more here.) If you decide a Capital One Spark Card is right for you, this is a great pick for businesses that want to carry a balance with an introductory APR.

There’s annual fee and it offers an intro APR of with APR after that. You can also earn unlimited Good credit is required.

Nav Prime Card

A charge card, the Nav Prime Card* is exclusive to Nav Prime users. Transactions are reported as a monthly tradeline to all the major business credit reporting agencies. Unlike a secured credit card, there’s no security deposit required, and your personal credit score will not be checked.

With Nav Prime and the Nav Prime Card, you can double your tradelines since both report to business credit bureaus monthly.

Secured vs. Unsecured Credit Cards

If you can’t qualify for a small business credit card due to bad credit, you may want to consider a secured credit card. These cards require a security deposit as collateral. Pay on time and can build credit, eventually qualifying for an unsecured card.

However, there are not a lot of issuers offering secured business credit cards. Bank of America is one of the few major issuers that does so. Learn more about business secured cards here.

Tips for Building Business Credit With Credit Cards

If one of your goals is a good business credit rating, consider getting a business credit card. Many entrepreneurs think their business has to be well-established and profitable to qualify, but that is not always the case. Card issuers are often more interested in the personal credit score of the owner who applies, and will often consider income from a variety of sources, not just the business itself.

To build strong business credit using a business credit card, make sure you:

- Pay your credit card on time. Payment history is the most important factor in personal credit scores and can be an even greater factor with business credit scores. Some business credit scoring models rely almost entirely on payment history.

- Keep balances low. Business credit reports are different from personal credit reports in several ways. One is that issuers don’t typically report credit limits. Unlike personal credit scores, where debt usage is based on the balance compared to the credit limit, with business credit the balance may be compared to the highest balance reported. Your business may appear “maxed out” more easily this way. Not all commercial credit scoring models will evaluate debt usage, but when they do, lower balances can be a benefit.

- Check credit often. Another way business credit reports are different than personal credit reports is that they do not list the name of the lender (or card issuer). As you begin to build business credit, keep track of your business credit reports to identify when one of these accounts reports. You’ll then be able to track how various accounts impact your credit history.

Credit cards can be a flexible and relatively low-cost way to borrow for your business and can offer lucrative rewards that provide additional value at no cost when you pay your balances in full. As with all types of credit, you want to be careful and cautious so you don’t put your business finances at risk.

FAQs

Can a personal credit card build business credit?

No. A personal credit card will not build business credit because it will not appear on business credit reports. To build business credit, you’ll want to choose a small business card that reports to business credit.

Can you get a business credit card with a 600 credit score?

Most business credit cards require good or excellent credit to qualify. If your credit scores are below 650, you may need to consider a secured credit card to build personal scores. There are also many business tradeline options (like Nav Prime) to build business credit.

How can I build my business credit fast?

The fastest way to build business credit is to establish accounts with companies that will report your payment history, including business credit cards, business loans and vendor accounts. (Not all of these companies will report, so be sure to check before you apply.)

Nav Technologies, Inc. is a financial technology company and not a bank. Banking services provided by Blue Ridge Bank, N.A., and Thread Bank, Members FDIC. The Nav Visa® Business Debit Card is issued by Blue Ridge Bank, N.A. or Thread Bank, and the Nav Prime Charge Card is issued by Thread Bank pursuant to a license from Visa U.S.A. Inc. and may be used everywhere Visa cards are accepted. FDIC insurance is available for your funds on deposit, up to $250,000 through Blue Ridge Bank, N.A. or Thread Bank, Members FDIC. See Cardholder Terms for additional details.

This article was originally written on February 6, 2018 and updated on April 20, 2024.

I’ve had Chase Ink, Amex Blue, and Capital One Spark business cards for 2 years and my LLC still does not have business credit.

Cecille – Those issuers do report to at least some major credit bureaus though you won’t see them on all your reports. If they are missing from reports, I’d check with the issuer to make sure the information they have about your business is correct. In addition, you may want to look into vendor accounts.

I read the article and thought it provided great info. Based on the info Provided, I applied for the chase business credit card believing it reported to all 3 bureaus. Needless to say, I was approved and just found out (directly from a Chase Agent) that they don’t report to business bureaus at all unless you’re 60 days delinquent. The exact opposite of being helpful when trying to build business credit.

Toni – I don’t believe that’s correct. My understanding is they only report to the cardholders personal credit if they are 60 days delinquent. Maybe that’s what the rep had in mind? It’s not my understanding that’s the case for business credit. Are you monitoring your business credit reports to see if they report? (I personally have a Chase business credit card that is reporting.) Also please keep in mind that policies do change. We try to keep this up to date but in the past some major issuers have changed how they report.

I also have a Chase Business Credit Card and I called customer service today 11/09/2021 and they told me they only report negative inquiries NOT on time payments which does not help me build my business credit.

I personally have a Chase small business credit card that reports to business credit. I’ll see if anything has changed but I’m not aware that it has.

I just got a Wells Fargo business credit card with a 5000.00 limit I don’t have any trade lines at all what can I do to get a trade line that reports

Congrats on the credit card! This list should help with establishing tradelines that report.

I applied on the Nav site today and was declined on a card after having other business cards with perfect payments for the last 3 years. (2 with $500 limit and one with 3K limit) After I applied for the Amex blue business card and was approved for 21K. Business credit really doesn’t make sense to me.. ps. Personal credit score ranges 705-720

I was also rejected for a business line of credit thru my bank and my rep couldn’t understand why. Can you explain?

Matt – Have you tried calling the card issuer that declined you to find out why, and to ask for reconsideration? Most major issuers will allow you to talk to someone to have the decision re-evaluated. In addition, they should send you information about the top reasons you were declined. Most major card issuers make their decision based on personal credit score, income from all sources and a variety of other factors, some of which are public information and many which are not. My suggestion is to reach out to them to find out more. (You may need to specifically ask to speak to someone about reconsideration.)

As for the business credit line, it’s impossible for me to say why you were turned down as every lender has its own underwriting rules. This article talks about what lenders must tell you when you are turned down for business loans. It may be helpful.

Finally you can always set up time to talk with one of Nav’s Credit & Lending Specialists to find out what types of loans you may be qualified or to better understand possible hurdles. Nav works with a variety of lenders so they may have some insights that will be helpful.

Hello,

How long do I have to have business credit in order to apply for a credit card for my business? Because I don’t want applying for credit cards that I’m not going to get approved of damage my credit.

Most business credit cards make the decision based on personal credit scores, not business credit. If you have a Nav account, Matchfactor can help you narrow down choices. It’s not full pre-approval but our customers who use Matchfactor are 3.5x more likely to get approved.

I’ve been in business for 6 years and I’m just trying to establish my business credit,I have really good personal credit, and I’m just trying to get a card that will for sure start to build my business credit…can you give me the cards that will report to the business report please

Yes, scroll up to the chart in the article that shares which business credit bureaus many issuers report to. When you go to apply, Nav can help. If you have a free Nav account look in your account for matches. It’s not full pre-approval but Nav customers who use MatchFactor are 3.5 times more likely to get approved for a business credit card. And if you have any questions, feel free to reach out to customer support: support@nav.com.

Hi I been in business over 15 yrs but have no business credit.what can you help me with to get business credit and credit card.

Greg – In addition to this article, we have a guide on how to build business credit. You’ll find it here.

Where do you go to apply for a business credit card?

Juanita – Nav can help. If you have a free Nav account look in your account for matches. It’s not full pre-approval but Nav customers who use MatchFactor are 3.5 times more likely to get approved for a business credit card. And if you have any questions about what you’re seeing (or not seeing), feel free to reach out to customer support: support@nav.com.

How do I get my Wells Fargo secured business card to report

It is our understanding Wells Fargo reports to SBFE though I can’t comment specifically on the secured card. Unless you are getting a report that includes SBFE data you won’t see that. I would suggest you reach out to them to confirm they are reporting your account.

How to get my three business tradelines reporting to Experian and Equifax small business. Also get them to report to my dun’s number.

That should happen automatically if they report to that bureau. Keep in mind that sometimes the report you see may not include all accounts as these credit bureaus may sell different types of credit reports.

Requesting a REFUND, not seeing any results for an enhance business profile.

Tanya – Please feel free to reach out to Nav’s customer support team and they will be happy to help.

Tring to get my business credit started

I’m just curious ? If applying 4 a business credit card…. In addition 2 checking one’s personal credit, which business credit report will the top banks pull from ? We currently have a business charge card with AMEX which your chart say’s reports to SBSE. So my question is will Chase also use SBSE and personal credit 4 approvals ?

Thanks

Not necessarily Rob. For the most part these issuers make the decision based on the applicant’s personal credit. While they help build business credit by reporting they generally don’t rely on business credit reports to make the credit decision.

Gerri, I incorporated on 5/19/2020, and as of today I have Net 30 accounts with Grainger, Uline, Zoro, Crown Office Supplies, Summa Office Supplies, Pilot/Flying J Axle Fuel Card and a few more. Also I have a Amazon Business Credit Line $4000, Home Depot Pro Account, Exxon/Mobil, Chevron/Texeco, Phillips 66/76 fuel cards. As well as a direct bill account with Motel 6 and I’m missing a few but is this a good start? All accounts I did NOT sign a Personal Guaranty. And personal credit score is 500 and 530 horrible. I have a D&B 80 Paydex, Experian 44 and Equifax 441.

Cody that is a Great start!!! I have a question for you about your net 30’s

Teach me your ways! That’s awesome though!

Hey buddy how did you do all this? I keep getting denied for net 30s

Hi Cody may I ask how you could pull getting all those with that credit score please fill me in I have the same credit score and am afraid they will all deny it? Thanks for your help! Desperate

?!

I signed up with Nav in order to get matched for a business credit card, but it’s not been very helpful. I have bad personal credit, I’m trying to find a secured business credit card to help me build my business credit without having to rely on my personal credit. I was guided towards the secured Wells Fargo business card but I was hoping for some more customized options & guidance. (I’m having difficulties with Wells Fargo because you must have a checking account with them, and I wasn’t approved yet, presumably because of my personal credit)

Charles – there are limited options for secured business secured credit cards. Have you considered vendor accounts? That might be a better option while you work on your credit.

I have horrible personal credit. I have been using NAV for approximately 6 months now. I have a NET 30 account with ULINE, tradeline reported by Nav.com, and utilities reported through eCredable (providing three more tradeline accounts). I just applied for a Capital One small business credit card and was approved for a $1,000 limit! My first business credit card!! It’s been a slower process than I would like, but following Nav’s advice has thus far worked for me!

Great to hear! Congratulations!

congrats! My personal credit is horrible. Can you share how you got approved for your business credit card?

The reporting section of this is misleading. Chase only reports past due payments not ontime payments. It is unfortunate that business credit does not have the same requirments as personal

I have two net 30 account.

And good business credit. My credit is low. I have been in business for 5yr . How do i apply for credit card. On business only

Barbara,

I’m not sure I understand your question. All small business credit cards from major issuers will check your personal credit. As this article describes, some report to only business credit and others report to both personal and business credit. You can find business credit cards through Nav’s Marketplace.

How do you begin the process of only using your business credit when applying for any type of credit & not using personal credit in conjunction? My business is 3.5 yrs old. I had a Kiva loan that’s since been paid in full. I also have a business Cap 1 card which I cant remember if its connected to my Personal Credit or not. I believe it is. I want to start moving my bus credit to stand alone. What else shld I do besides continue to build solid business credit? How do you ultimately make that jump where creditors will reply strickly on your business credit?

Holly, It sounds like you are off to a great start. Generally, lenders will look at 3 main factors: time in business (3.5 years is pretty good), revenues and credit (business and/or personal). You will rely at least somewhat on personal credit while you continue to build your business. Have you looked into vendor accounts to help build business credit? This article may help: Easy Approval Net-30 Accounts

I noticed you have American Express listed as reporting to D&B, however they only report if there is negative activity. Do you know of any business cards that report on a monthly basis to D&B positive or negative?

Thanks Kadian – we’re updating that post. The other issuers listed as reporting to D&B should be both positive and negative information. However, not all Dun & Bradstreet credit reports will list bankcards.

Hi Gerri,

Thank you for all the information. Based on the info in the chart above, does this mean that Chase and Citi Bank are more advantageous because they report to more credit agencies?

It’s really your call Nathan. If you’re building business credit it may be helpful to have accounts that report to multiple bureaus.

I have a chase business credit card and i called to see if this was reporting as a business credit card and they said no it only reports to personal. Is this fraud? it actually says Chase INK business credit card and i use is soley for business. Chase does not report to Dunns I am not sure why this website says it does.

That information came directly from Chase corporate public relations. Have you checked your business credit to see if it’s reporting? You can do so for free at Nav.com.

With only a handful of banks on the list is there a simple way to to get this information for banks not on the list? I have tried calling some banks but the CSR do not seem to know what business credit agencies their cards report to.

For example would I be able to find out by contacting Experian or Equifax directly?

Good question. Unfortunately there is no easy way to get this information. The credit reporting agencies won’t be able to tell you. (And business credit reports don’t list the names of card issuers.) However this list encompasses the top small business card issuers which together issue the large majority of business credit cards available. Keep in mind that these issuers often have multiple cards with different rates, fees, and rewards – so there’s a good chance there is something on that list that should be a fit!

I’ve read plenty of places that the Wells Fargo Secured credit card reports to DnB and the other credit agencies. I cant find any information about that unsecured bussines card though. Does the unsecured Business Platinum report to DnB or the other agencies? Logic would suggest it would, but I cant seem to find any info on this.

Hi Joe,

As indicated in the chart above, Wells Fargo reports their business credit cards to the SBFE. That means that data may be available on certain credit reports purchase through Certified Vendors which may include D&B, Equifax, Experian and LexisNexis. This article may help: What is the SBFE?

My daughter is interested in applying for a business credit in the near future. Her Business is new (less than 6 months), but she has established (3) vendor credit accounts which are paid, and in good standing, will that qualify her business for a unsecured business credit card?

Most major small business credit card issuers base the decision on the owner’s personal credit scores and income from all sources included in the application.

I’m interested in a business card to start.

Is there a secured deposit type card available.

I’d like to deposit 1000.00 dollars to start.

Wells Fargo offers a secured business credit card. Before you go that route you may want to get a free Nav account and check whether you have high MatchFactor scores for any of the unsecured business credit cards.

I have a Nav account! How do I go by checking to see if I can get approval for Wells Fargo Secured Card???

The Wells Fargo secured card is not currently available in the Nav marketplace. I believe you need to go into a branch to apply for it.

Let us know how your experience with it goes. I’m sure other small business owners will be interested.

Hi – after having such a difficult (slow) time building business credit – and having much luck with Secured cards building my personal credit, I researched (for a long time actually) and found that only Wells Fargo is the only secured business card out there. I have now, just opened a business checking account at Wells Fargo, and read thier brochures and online information about this card – you can apply for a card by depositing $500 – $25000. Now after discovering on NAV, I see Wells Fargo ONLY reports to the SBFE report. After reading NAVs info on SBFE….it just doesn’t sound attractive enough for me to go for their card – – which is surprising because WELLS FARGO, is up there with CIti, Chase, and Discover….and should be reporting to all. I wish you could point me in the right direction or better yet, which business cards report to ALL 3 of the credit reporting agencies. Ironically – your chart also shows American Express reports to D&B (only negative – strange, is this correct) and then only to SBFE….I only have tradelines at the moment – but I want to get business credit card(s) – that guarantee reporting. As I said, I have business checking at Wells Fargo and business checking at Chase…when you have an account at their bank, that can be like more of a foot in the door, to be approved for their card – now, I am not sure if the Wells Fargo card will be helpful in building credit. I know this is a lot of info / but do hope you can summarize and reply to the main issues. thanks!

Hi Paul,

Yes, business credit reporting is much less standardized than personal credit reporting as you’ve learned. Since it is a voluntary system there’s no requirement that an issuer report to all three major bureaus, and many don’t. You’ll see in the chart on this page that some issuers do report to all the major commercial credit reporting agencies but since you are looking for a secured card I assume you are having trouble qualifying for an unsecured card (?) Unfortunately there are also few unsecured business credit cards. I still think there is value in a card that reports to the SBFE as that data can be accessed by lenders through multiple bureaus. But as you continue to work on your credit you may want to check back in your Nav account to see what other business credit cards are coming up with a high MatchFactor score and consider one that offers the reporting you’re looking for. I wish I could offer you the perfect solution but as you’ve learned business credit is not the same as personal!