Business credit, made better

Monitor and build business credit with all three major bureaus so you can unlock your brightest business days. You can check your credit standing for free.

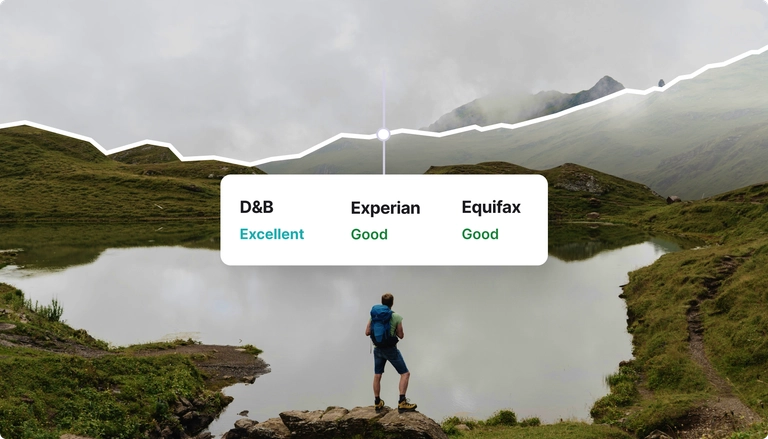

Meet Nav

You didn’t start your business because you love business credit

But that’s why we started ours. Nav isn’t just a powerful suite of financial tools — we’re part of your team.

credit health

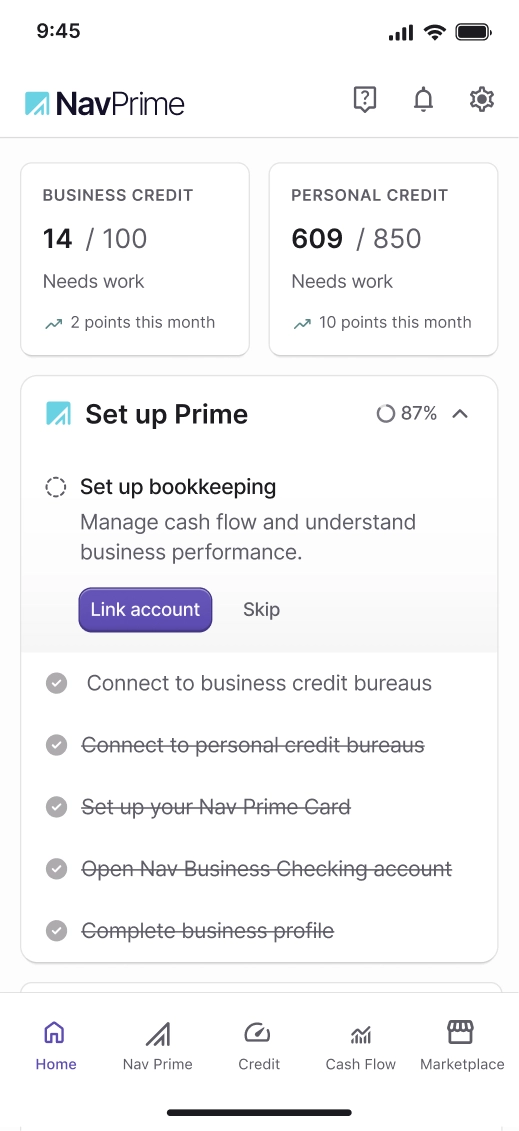

Track your business and personal credit side by side

See the factors that impact your credit the most and take control with real-time alerts. Get your general credit standing for free, or unlock exact scores and detailed reports with Nav Prime.

Nav Technologies, Inc is a financial technology company and is not an FDIC-insured bank. Banking services provided by Thread Bank, Member FDIC. The Nav Prime charge card is issued by Thread Bank, Member FDIC, pursuant to a license from Visa U.S.A. Inc. and may be used anywhere Visa cards are accepted. See Cardholder Terms for additional details. All other features of the Nav Prime membership are not associated with Thread Bank.

financial health

The credit and financial health platform built for small business owners

Understand where your business stands today, what your options are, and how to move forward.

Monitor credit score progress

Watch your business and personal credit health side by side.

Access credit for your business

Get matched to a loan, credit card, or line of credit that fits you and your needs.

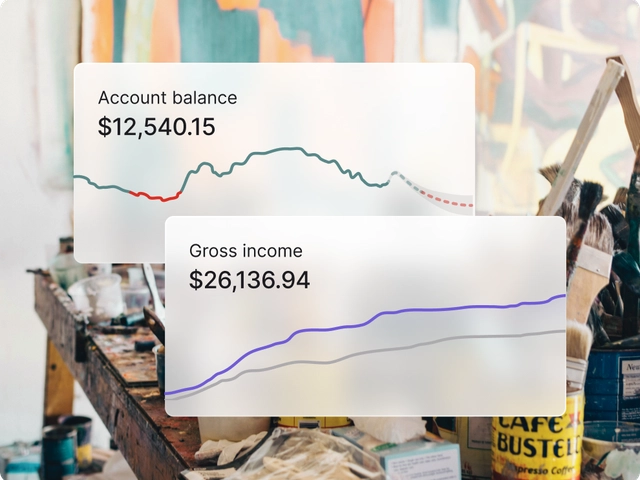

Track your cash flow

Understand your full financial health snapshot so you can be ready for anything.

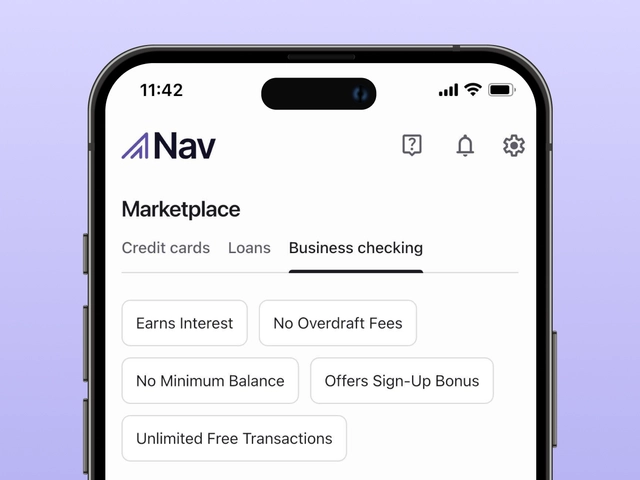

Get essential business tools

Scale with financing calculators, business checking, insurance, tax prep, and more.

join nav prime

The simpler way to build business credit

Break plateaus, not the bank. Monitor and build your scores, get 1-on-1 guidance, and simplify your path to funding opportunities — for an incredible price.

Pay monthly

Pay quarterly

save 20%

Track

$39.99

/ mo

For new business owners looking to monitor credit, or established ones who want to protect it

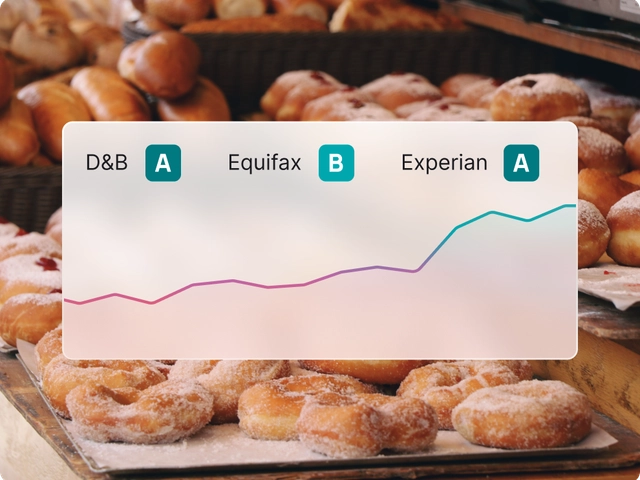

Track with Prime5 credit scores, alerts, and reports from D&B, Experian, Equifax, and TransUnion

One tradeline to build business credit (membership payment)

Build

Popular$49.99

/ mo

For growing business owners looking to build business credit¹ with up to two tradelines

Build with Prime5 credit scores, alerts, and reports from D&B, Experian, Equifax, and TransUnion

One tradeline to build business credit (membership payment)

Second tradeline to build business credit history (Nav Prime Card)²

Bookkeeping tools to manage cash flow and simplify taxes

Expand

$74.99

/ mo

For business owners seeking one-on-one guidance from an expert to reach their next level

Expand with Prime5 credit scores, alerts, and reports from D&B, Experian, Equifax, and TransUnion

One tradeline to build business credit (membership payment)

Second tradeline to build business credit history (Nav Prime Card)²

Bookkeeping tools to manage cash flow and simplify taxes

Dedicated business credit coach

FICO SBSS score to track eligibility with 7,500+ lenders — and the SBA

Nav Technologies, Inc is a financial technology company and is not an FDIC-insured bank. Banking services provided by Thread Bank, Member FDIC. The Nav Prime charge card is issued by Thread Bank, Member FDIC, pursuant to a license from Visa U.S.A. Inc. and may be used anywhere Visa cards are accepted. See Cardholder Terms for additional details. All other features of the Nav Prime membership are not associated with Thread Bank. With regard to credit history building features: results will vary, some users may not see improved scores – improvement not guaranteed. Scores are calculated from many variables. The Nav Prime Charge Card is a business financing product and may not be used for personal, family or household transactions.

by the numbers

Nav helps your business reach new heights

We’ve helped small businesses all over the US take their business from idea to reality.

2.5M

small businesses have trusted Nav with improving their financial health

40

avg. point increase1 across business credit bureaus within the first 3 mos. of Nav tradeline reporting

90%

of small business owners who use Nav have been in business for up to 13 years

$92M

in financing provided to small business owners through Nav’s partners in 2024

join nav prime

The simpler way to build business credit

Get the roadmap your business has been looking for. Up to 2 tradelines is just the start.

The reviews are in

Meet the small business owners who are redefining their business journey with Nav.

“Their credit reports are extremely helpful, very clear, and informative, and they are all offered at a fraction of the cost that it would be if a business purchased individual business memberships from each credit bureau. And on top of it, they consistently report a credit line to the business credit bureaus once a month.”

Sergio C.

ENERGY COMPANY

“Nav is the guide indisputably in aiding and guiding businesses to WIN. When 10 banks turned my brand down for credit or loans, Nav came through with a solution.”

Jonathan C.

420XAA BY JCOLE

“After being denied for funding, I downloaded Nav and found things on my business credit report that I didn’t even know existed. This app is far more in depth than any of its competitors... Nav shows you what the lenders are actually seeing. I’d give it 10 stars if I could.”

Tyler J.

PACKAGING COMPANY

“I’m new to the whole business scene, so it helps to have an app that has so much all in one! Nav Prime is definitely a must-have for your new business.”

Edward Y.

BGG LOGISTICS

Made on Main Street:

Where to shop this holiday season

Discover gift ideas and inspiring stories from small businesses that help shape their communities.