Compare daycare loans and child care business funding options for 2026

Written byLyle Daly

Reviewed by Robin Saks Frankel

Summary

- Demand for quality child care is growing due to the increasing number of dual-income and single-parent households. Meeting this demand can be difficult for daycare owners, as child care businesses come with significant startup and expansion costs.

- If you need funding for your business, multiple options are available, including daycare loans from the SBA, grants, and lines of credit.

- This guide will help you identify the best funding path based on your business stage and needs.

How much does it cost to start or expand a daycare business?

Startup costs typically range from about $5,000 to $50,000 for home-based daycares and $50,000 to $500,000 for commercial daycare centers. The main costs of starting a daycare business include:

- Licensing fees: Your daycare business needs to meet the licensing requirements set by your state. Licensing costs may include an application fee, annual fee, background checks for all staff, facility inspections, and training and certifications.

- Insurance: Most states require general liability insurance and workers’ compensation at a minimum, and you’ll need commercial auto insurance if your daycare transports children. You may also want to add professional liability insurance, commercial property insurance, and abuse and molestation insurance.

- Facility costs: Commercial daycare centers will need to lease or buy a building and ensure it meets state licensing requirements. Home-based daycares are the far more affordable option, but there are still costs to meet zoning and safety requirements.

- Equipment: This includes furniture, playground and climbing structures, office products, kitchen appliances, and safety equipment.

- Supplies: This includes toys, child care products, educational materials, office supplies, and hygienic items.

- Staffing: The number of employees determines a daycare’s maximum capacity, as every state has maximum child-to-caregiver ratios. A small home-based daycare can be a solo operation, although you may want to have at least one employee to assist you. Commercial daycare centers generally have 10 to 30 staff members, although it depends on the size of the daycare.

The table below provides a general breakdown of costs for home-based and commercial daycares. Exact costs will vary depending on the size and location of the daycare.

Category | Home-based daycare | Commercial daycare center |

Licensing fees | $500-$2,000 | $2,000-$10,000 |

Insurance | $1,000-$5,000 | $3,000-$15,000 |

Facility costs | $1,000-$5,000 | $25,000-$200,000 |

Equipment | $1,000-$5,000 | $20,000-$80,000 |

Supplies | $500-$2,000 | $3,000-$15,000 |

Staffing* | $0-$6,000 | $10,000-$60,000 |

*Staffing is shown as a monthly operating cost. All other rows are startup costs.

How daycare financing can help your business

Financing for your child care business can provide much needed funds to grow. There are many expenses involved in starting up a child care business, or expanding a current one. Cash flow may be uneven as enrollments fluctuate.

Overall, however, the outlook for daycare businesses is promising. Total revenue for the daycare industry is estimated at $62.1 billion in 2026, according to a May 2026 IBISWorld analysis.

Daycare business funding may be used to:

- Acquire an existing daycare business

- Purchase a daycare franchise

- Purchase real estate for your daycare facility

- Renovate or retrofit a location

- Purchase supplies

- Manage cash flow

- Cover payroll

- Market your daycare business

Types of financing options for child care businesses

Loan type | Typical amount | Best for | Credit requirements* | Time to fund |

SBA loan | $500-$5 million** | Buying or building a daycare facility, major expansion, buying an existing daycare | 620-680+ | 30-90 days |

Business line of credit | $10,000-$150,000 | Working capital, bridge financing during seasonal dips | 600+ | Same day to 2 weeks |

Term loan | $10,000-$1 million | Large one-time project, such as a renovation | 600+ | Same day to 2 weeks |

Equipment financing | $10,000-$5 million | Expensive equipment, such as a playground or furniture | 580+ | As soon as 24 hours |

Business credit card | $1,000-$100,000 | Everyday expenses, earning cash back or points | No minimum for some cards, 670+ for standard business cards | Can be approved instantly, card arrives in 7 to 10 days (some issuers offer temporary card number upon approval) |

Commercial real estate loan | $150,000-$5 million | Buying, building, or refinancing your daycare facility | 660+ | 30-90 days |

*Credit score requirements are estimates as lenders generally do not publish this information

**Daycare businesses are not NAICS 31-33 manufacturers and are subject to the $5M standard limit

SBA loans for daycare businesses

- Excellent rates and terms

- Good credit generally required

- May be available to startups

The U.S. Small Business Administration (SBA) guarantees small business loans made by participating lenders. These SBA loans are popular for their low interest rates and affordable repayment terms. There are three loan programs: SBA 7(a) loans, SBA 504 loans, and SBA microloans. Note that as of March 1, 2026, all direct and indirect owners must be U.S. citizens or U.S. nationals with a U.S. principal residence to qualify for SBA loan programs.

See the current SBA loan rates here.

SBA 7(a) loans are the most popular SBA lending program. Standard SBA 7(a) loans range from $350,001 to $5 million, but there are several types of SBA 7(a) loans available, including 7(a) Small loans for up to $350,000. Funds may be used for working capital, real estate, equipment, or refinancing current business debt. While lenders set the interest rates, the SBA sets maximum allowable rates, which have ranges from 9.75% to 14.75% depending on the loan amount as of June 2026. Note that these are the caps and many borrowers will receive rates lower than the maximum allowable rate.

SBA 504 loans are financing for major fixed assets that promote business growth and job creation. These loans are often used to acquire or expand real estate, and they may be helpful for daycare businesses looking to acquire or expand a facility. They typically involve a loan for 50% of the project cost from a third-party lender, 40% from a Certified Development Company (CDC) and a 10% owner equity contribution. Loan amounts of up to $5.5 million are available, and interest rates range from about 5.6% to 6.1% as of June 2026.

SBA microloans are up to $50,000, with the average amount being about $13,000. Funds can be used for a range of expenses, including working capital, inventory, supplies, and equipment. The smaller size of these loans make them well-suited for home-based daycare businesses, although commercial daycares with modest funding needs could also use them. Interest rates generally range from 8% to 13%.

Business lines of credit

- Flexible

- Only pay interest on amount borrowed

Every established daycare business owner should consider a line of credit. It can provide much needed cash flow when unexpected expenses arise, or when revenues temporarily fall short. With a line of credit, you only borrow the amount you need (up to your credit limit) and pay interest on that amount. If you have been in business for at least a year (ideally, two), can demonstrate healthy revenues and have good credit, consider lining up a line of credit before you need it.

Credit limits typically range from $10,000 to $150,000, although there are smaller and larger options. On the high end, some lenders offer business lines of credit for up to $500,000. Median interest rates were about 6.5% to 7.5% at the end of 2025, according to data from the Kansas City Fed.

Term loans

- Good for specific projects

- Periodic payments

- Rates vary

Need to add new playground equipment? Buy supplies for expanded enrollment? A term loan could help you pay for those items over time. These loans are good for financing specific projects. Similar to a line of credit, you’ll likely need to show at least a year or two in business, good credit, and solid revenues. But if you do, a term loan can offer predictable payments for expansion. If you’re looking for a short funding timeline, online lenders are a faster alternative to traditional banks.

Equipment financing

- Tied to specific equipment

- Periodic payments

- May have more flexible approval requirements

Another way to pay for playground equipment, classroom furniture, kitchen equipment, vehicles, and other big-ticket items is equipment financing. The equipment you buy serves as the collateral on the loan, reducing the risk for the lender. The lower level of risk means that it’s often easier to get approved for equipment financing than a business loan or line of credit, and you may qualify for a lower interest rate.

Business credit cards

- Available to startups

- Only pay interest on amount borrowed

- May help build business credit

Business credit cards can be a safe and convenient way to pay for items you need and to earn rewards in the process. But they can also offer an affordable line of credit that can be especially helpful to child care providers who can’t qualify for a small business line of credit, including startups. Don’t worry if your business doesn’t have strong revenues yet. If you’re self-employed, you may generally include income from all sources on your application.

Credit cards generally aren’t as good for long-term funding, because they have higher interest rates than other financing options. However, some business cards have 0% intro APR offers that last six to 12 months or longer. These work extremely well for short-term financing, as you can potentially pay no interest on your purchases if you pay off your balance during the 0% APR intro period.

Commercial real estate loans

- Larger funding amounts for real estate acquisition

- Strong borrower qualifications required

If your business is looking to acquire, renovate, or retrofit property, you may need a commercial real estate loan. The terms of these loans will vary greatly by lender.

Grants for daycare and child care businesses

Before you take on debt, it’s worth checking if your daycare qualifies for any grants. Grants don’t require repayment, but for that reason, they’re competitive. They also come with restrictions on how you can use them and some may have other requirements, such as being earmarked for certain populations or geographies. Still, grants for child care businesses could help cover some of your operational expenses.

Child Care and Development Fund (CCDF) grants

The CCDF is the largest federal funding source for child care, and it’s designed to help low-income workers afford care for their children. CCDF funds are distributed to states, territories, and tribal governments, each of which must have a lead agency to manage the funds.

The majority of CCDF funding goes toward child care subsidy payments. Qualifying low-income families receive CCDF-vouchers that they can use at state-approved child care programs. If your daycare is approved, you can enroll families with CCDF-vouchers.

States can also use a portion of their CCDF funding to offer child care grants for specific purposes, such as daycare expansion, startup costs, or renovations. To see available grants and apply, check with your state’s lead agency, either on its website or by phone.

State-specific child care grants

Your state may have child care grant programs available, either through its CCDF funds or other funding sources. The best place to find out is your state’s lead agency. You could also get in touch with your local Child Care Resource & Referral (CCR&R) organization, as these organizations partner with state lead agencies.

USDA Child and Adult Care Food Program (CACFP)

The CACFP is a federal reimbursement program for providing nutritious meals and snacks to eligible children and adults. It’s not a traditional grant that you receive upfront, but it can help cover your daycare’s food costs.

If you want to join the CACFP, you can find a CACFP sponsor or contact your state agency directly. Check out the National CACFP Association’s “Join the Food Program” page to learn more.

Reimbursement amounts depend on multiple factors, including the income level in the area and the household income of your daycare’s enrolled families. Daycares that serve primarily low-income families can get a significant amount of food costs reimbursed through the CACFP.

Small Business Innovation Research (SBIR) grants

SBIR grants provide early-stage technology funding for small businesses and entrepreneurs. Most daycares won’t qualify, and these grants can’t be used for opening a daycare or working capital. However, if you also plan to develop a technology product related to child care or early childhood education, then SBIR grants could be worth a look.

Private foundation grants for child care

Many private foundations offer grants for child care, but most of them award funding to nonprofits. If you have a for-profit daycare, it won’t qualify for a large portion of these grants. You may have better luck with grants from smaller, local foundations, so keep an eye out for funding opportunities in your community.

If you have a nonprofit daycare, then you’ll have far more funding options available. Some of the biggest private foundations that offer child care grants are the Buffett Early Childhood Fund, W.K. Kellogg Foundation, and Bainum Family Foundation.

How to qualify for a daycare loan

Most lenders focus on three main factors when evaluating your application for child care center financing: credit, revenue, and time in business. Your business structure and licensing also play a role in loan approval and how much you can borrow.

Credit score requirements

Lenders may check your personal credit as the owner-operator of the business, the business credit of your daycare business, or both. In general, here’s the estimated personal credit score you’ll likely need for different types of business loans:

- SBA 7(a): 650+

- SBA 504: 680+

- SBA microloan: 620+

- Online business loan or line of credit: 600+

These are general guidelines, but exact requirements vary by lender, and lenders normally don’t make this information public. A high credit score can help you get approved for a daycare loan, but there are options for borrowers with low credit scores available. They just tend to have higher interest rates.

Revenue and time in business requirements

Lenders usually ask for your most recent yearly revenue and your time in business during your loan application. Here’s what minimum revenue requirements might look like depending on the type of loan:

- SBA 7(a): $100,000+

- SBA 504: $100,000+

- SBA microloan: No fixed minimum

- Online business loan or line of credit: $50,000-$100,000+

Once again, these are general guidelines and vary by lender. Time in business requirements are typically at least two years for SBA 7(a) and 504 loans, and six months to a year for online business loans. SBA microloans don’t have a minimum time in business requirement, making them a potential option for starting a new daycare.

Required documentation

The application process for a daycare loan is much smoother when you have all your paperwork in order. Here’s a checklist for the documents lenders often request:

- Personal and business tax returns for the last two to three years

- Business bank statements for the last three to six months

- Profit and loss (P&L) statements

- Balance sheet

- State child care license and other required business licenses

- Insurance certificates

- Business formation documents

- Business plan

- Government-issued ID for all business owners

Business structure and licensing

The business structure of your daycare impacts your financing options, as some lenders won’t lend to sole proprietorships. You’ll want to operate under a formal business entity, such as an LLC or S corp. You could have more financing options this way, and it’s also extremely important from a liability perspective.

An LLC or S corp creates legal separation between your personal assets and your business, which is crucial for child care businesses. If someone ever files a lawsuit against your daycare, your personal property is generally protected from a judgment.

Since daycares need to meet licensing requirements to operate, lenders typically only approve applications from licensed daycares. If your license is still pending, then a lender may offer a conditional loan approval contingent on approval of your child care license. Your daycare’s licensed capacity can also affect the size of the loan you qualify for, because this limit is a key factor in your daycare’s maximum revenue.

How to apply for daycare business financing

Once you’ve decided that daycare financing is the right move, here’s how to apply, step by step.

Step 1 - Assess your funding needs

Run the numbers on how much money you need to borrow, and decide if you want a one-time loan or a line of credit that you can use and reuse as needed.

If you’re opening a new daycare, add up all your expected startup costs. You can use the estimates provided earlier and adjust them based on the size and location of your daycare. It’s also a good idea to add six to 12 months of expenses so you have a working capital cushion. Most child care businesses take some time to reach profitability, so keep that in mind when applying for daycare startup loans.

If you’re expanding or renovating, you can base your funding needs on the estimated project cost. You may want to add a cushion or go with a line of credit with a higher limit than what you need, in case the project goes over budget.

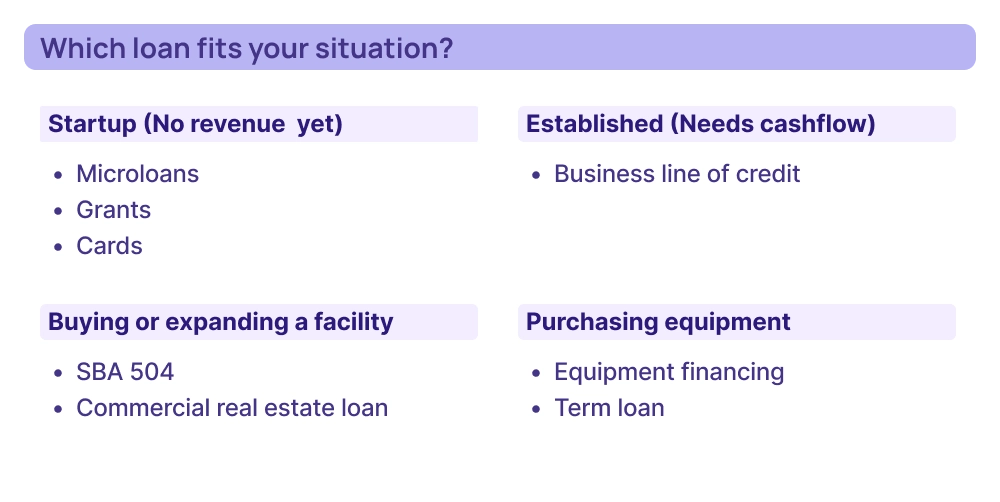

Here are some of the most common funding needs and the appropriate loan type:

- Buying or building daycare facilities: SBA 7(a) or 504 loan, commercial real estate loan

- Expensive equipment: Equipment financing

- One-time project or renovation: Term loan

- Working capital: Business line of credit

- Everyday expenses: Business credit card

Step 2 - Check your credit and financials

Find out which types of child care business loans are realistically on the table for you by checking your personal credit, business credit, and revenue. It’s easy to check your personal credit, as there are many free resources are available online to check your personal credit scores, including through your bank, credit card issuer, or services like Nav.You can get your business credit scores from all three major bureaus with Nav.

If you have good personal and business credit, you should have plenty of loan options, potentially including SBA loans and business loans from traditional banks. If you haven’t established high credit scores yet, you may need to focus on loans from online lenders.

Review your daycare’s most recent annual revenue, as well. Most types of loans are on the table with revenue of $250,000 or more, and $100,000 is often enough to qualify for SBA loans and some online business loans.

Step 3 - Compare lenders and loan options

Shop around and see what kind of loan offers you get from different lenders. The main criteria to compare are:

- APR: The annual percentage rate (APR) is the total annual cost of a loan, including interest plus loan fees. The lower your loan’s APR, the less you pay per year to borrow money.

- Term: The term is the length of the loan. A shorter term means you make a higher monthly payment but pay less interest overall. A longer term means a lower monthly payment but more interest paid over the life of the loan. As a general rule, go for the shortest term with a monthly payment amount you can afford.

- Fees: Business loans can charge a variety of fees, including origination fees and prepayment penalties. Get a full list of fees with any loan offers you’re considering to see what all the costs are and if the lender will penalize you for paying off your loan early.

- Funding speed: This may be a crucial consideration or unimportant, depending on how urgent your funding needs are. Online lenders are normally the fastest, with many funding loans in one to five business days. SBA loans can be much slower, in some cases taking 30 to 90 days.

Step 4 - Gather documentation and apply

Organize a folder with all the documentation you may need, including tax returns for you and your daycare, business banking statements, licenses, insurance certificates, and all other required documentation.

Highlight anything that demonstrates your child care business is a good candidate for a loan, such as a waitlist, growing revenue, or consistent positive cash flow. Be prepared to explain any issues, and consider pointing these out upfront to get them out of the way immediately. For example, if your daycare went through a seasonal dip, you may want to let lenders know during the application process so they don’t need to discover it themselves.

Choosing the right financing for your daycare business

To choose the right type of financing for your daycare business, you’ll first need to assess how much you need and how you’ll use the funds. Long-term financing, such as SBA loans or certain term loans, is best suited to larger projects with a high ROI over time. Short-term financing is best suited for cash flow gaps where you can repay the funds quickly.

Of course, it’s also important to understand what types of financing you qualify for. Startups will have more limited loan options than those that have been in business for at least two years with strong revenues, for example. Daycare business owners with good credit will have more options than those with bad credit.

How to create a daycare business plan for loan approval

If you’re thinking about owning a daycare, it’s essential that you create a detailed business plan. A business plan is where you can organize the goals for your daycare business and your roadmap to achieve them. It’s also something lenders ask for and evaluate when you apply for a loan.

Local SBA resource partners, including Small Business Development Centers, SCORE Business Mentors, and Women’s Business Centers, can help with your business plan and other parts of your business for free. You can also make one on your own. Here are the key components lenders will want to see.

Executive summary

The executive summary is the most important part of your business plan. It provides a one-to-two-page overview of your daycare, including the:

- Name

- Location

- Capacity

- Age range

- Funding needs

- How you’ll use the funding

- Competitive advantages

Lenders should be able to read the executive summary and immediately understand your business and why it will succeed. Since this is a summary of your business plan, write it last.

Market analysis

Explain where your daycare will operate, which community it will serve, the main competitors in the area, and what competitive advantages your daycare offers. Competitive advantages for a daycare include:

- A higher carer-to-child ratio for more personal attention

- Extended hours with earlier opening times and/or later closing

- Transportation services

- More affordable rates

- Specialized educational curriculum

The goal of market analysis is to demonstrate the demand for your business and why parents will choose your daycare over other options. You may want to include the number of families with young children in the area and how many of them have both parents working. If you have a waitlist or enrollment commitments already, make sure to mention that.

Services offered

Provide details on your daycare’s services and pricing. Include the ages you’ll serve, the maximum capacity (in total and for each age range), your hours, and any extra services your daycare will offer, such as meals or transportation.

All the services should have dollar amounts attached. This shows lenders how much revenue your daycare can generate to reach profitability and repay its loan.

Financial projections

Your financial projections show lenders that your daycare has the potential to be a profitable business. This section should have the following:

- Projected startup or expansion costs

- Monthly operating expenses

- Monthly cash flow forecasts

- Three years of financial projections with revenue, expenses, and net income

All your projections need to be realistic and defensible. Include the data behind your financial forecasts. For example, when forecasting payroll costs for your operating expenses, you should include the number of employees you’ll have and the average salaries for their positions.

Licensing and compliance plan

Explain how your daycare will obtain the required child care licensing and remain in compliance with all state regulations. Include your current license status, which should ideally be approved or pending approval. Also, cover your background check process for staff and the checks you have done on anybody you’ve hired already.

A child care business can be extremely rewarding and fill a crucial need in the community. Affordable financing can help you focus on what you do best: helping to nurture and grow the next generation.