You might not think to refinance a merchant cash advance (MCA), but it might just happen to you if you are carrying a balance from an advance and decide to take out another. If you are considering or will ever consider taking out a MCA, this article is a must read!

When dealing with non-traditional financing options, it’s really important to understand what you’re giving and what you’re getting. This is especially true when it comes to taking out a second advance or loan from some of these alternative finance options. We’ve seen Merchant Cash Advance (MCA) and Cash Flow Loan providers follow a weird practice that results in deeply hidden fees charged to the business owner.

First we’ll talk about this practice with MCAs

Like loans, with MCAs you get a set amount of cash up front, called the advance. But instead of getting charged an interest rate, you agree to pay back the advance amount plus a good chunk more, e.g. – 1.25 times (125% of) the advance amount (the multiple varies, but it’s typically 1.2-1.5X). Instead of regular fixed payments, you pay back your advance by agreeing to pay a fixed percent of your future credit/debit card sales. This continues until you’ve paid off the balance owed. Assuming you have consistent monthly card sales, it typically takes 3-9 months to pay off your balance.

An MCA example

You get a $30,000 advance and agree to pay it back with a 1.33 multiple ($30,000 × 1.33 = $39,900). The way that you pay it back is that 15% of your credit/debit card sales will go to the MCA provider. So if your monthly card sales are $45,000, you pay $6,750 each month until you’ve paid back the owed amount, $39,900. In this case it would take about 6 months to pay back what you owe.

The APR for this comes out to 123%. That’s steep. And once you’ve taken out the advance, you’re typically locked in to pay that interest rate, even if you pay down the loan in advance. In this case, it wouldn’t matter if you paid the advance back in 3 months or 9 months, you’d have to pay back the full $39,900.

Unexpected Refinancing When Taking Out 2nd MCA

Now suppose that for your first month your card sales were a little below average, and you repaid $5,900. Not a problem. Your remaining balance owed is $39,900 – $5,900 = $34,000. However, now your business needs $15,000 more in working capital so you decide to take out another advance.

The advance provider tells you because of good repayment history they’ll give you a lower rate this time of 1.25. That sounds great and you’d think this would be the same process as before, which means you would owe an additional $15,000 × 1.25 = $18,750, for a grand total of $34,000 + $18,750 = $52,750 owed

You would not think that it has anything to do with your existing advance. That is what we and most others would expect. And we would all be wrong. Instead, your MCA provider will include a refinance of your existing advance in the new advance they provide you. And it will cost you.

What actually happens is that the MCA refinances your original advance using this 2nd advance. In addition to the $15,000 you requested, the MCA also advances you $34,000, which is instantly used to pay off the $34,000 you owe on the 1st MCA. So you actually owe $49,000 × 1.25 multiple = $61,250

The difference between expected and actual amount owed after taking out the 2nd MCA is $61,250 – $52,750 = $8,500.

And your effective multiple for both advances is actually $67,150 / $45,000 = $1.49.

Wait what? How did this merchant end up paying a 1.49 multiple when the advertised multiples were 1.33 and 1.25?

Getting hit with a "Double Fee"

The $34,000 owed for the 1st advance is a portion of your original advance: $25,564 of the $30,000 you were advanced (the rest was paid off with your $5,900 payment after the first month).

The twist here is that you get charged a multiple on the $25,564 amount twice. $25,564 1.33 = $34,000. Then you $34,000 is included in the new advance: ($34,000 + $15,000) 1.25 = $61,250.

This double fee makes your overall multiple balloon to 1.49.

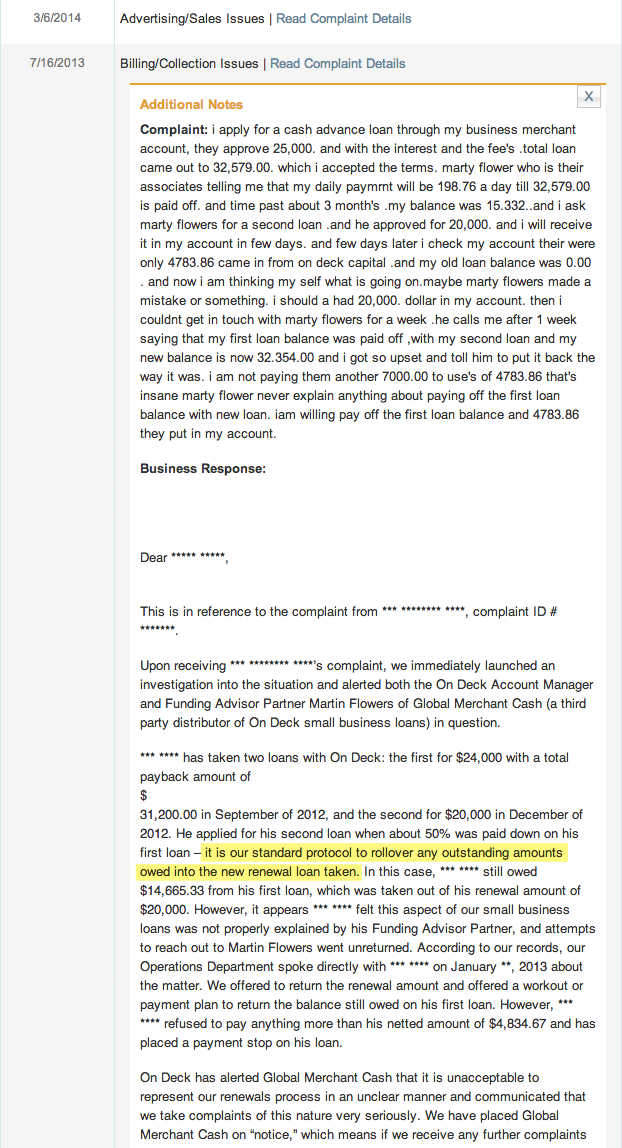

The math here is very unintuitive. But this practice is fairly common. As we mentioned in the beginning of this article, this practice happens with MCAs and Cash Flow Loan providers. Below is a real example of a cash flow loan (OnDeck Capital) customer that got caught up in this situation without having any idea what was going on.

Here is the complaint via the Better Business Bureau(View Here), edited for clarity:

{kind=link}

A few days later, I checked my account and only $4,783.86 came in from OnDeck Capital, and my old loan balance was $0.00. Now I am thinking to myself, ‘What is going on?’ Maybe Marty made a mistake or something. I should’ve had $20,000 in my account. Then I couldn’t get in touch with Marty for a week. He calls me after 1 week saying that my first loan balance was paid off with my second loan, and my new balance is now $22,354 and I got so upset and told him to put it back the way it was. I am not paying them another $7,000 to make use of $4,783.86 — that’s insane. Marty never explained anything about paying off the first loan balance with new loan.”

It’s a similar "double fee" situation where the borrower’s balance of $15,332 was charged against twice. In OnDeck’s response, it said blatantly:

Basically, the double fee is standard protocol for merchant cash advance and cash flow loan providers. When business owners sign the refinance offer, they are committed to paying double fees.

In their world, loans don’t amortize like bank loans or LendingClub / Dealstruck loans do. This is something small business owners absolutely need to pay attention to. The next time you are in a situation to refinance a non-bank loan or merchant cash advance, please re-read this post.

Try our merchant cash advance calculator for yourself:

This article was originally written on May 29, 2014 and updated on November 1, 2016.

Have at it! We'd love to hear from you and encourage a lively discussion among our users. Please help us keep our site clean and protect yourself. Refrain from posting overtly promotional content, and avoid disclosing personal information such as bank account or phone numbers.

Reviews Disclosure: The responses below are not provided or commissioned by the credit card, financing and service companies that appear on this site. Responses have not been reviewed, approved or otherwise endorsed by the credit card, financing and service companies and it is not their responsibility to ensure all posts and/or questions are answered.