The Dun & Bradstreet PAYDEX Score Explained

by Gerri Detweiler

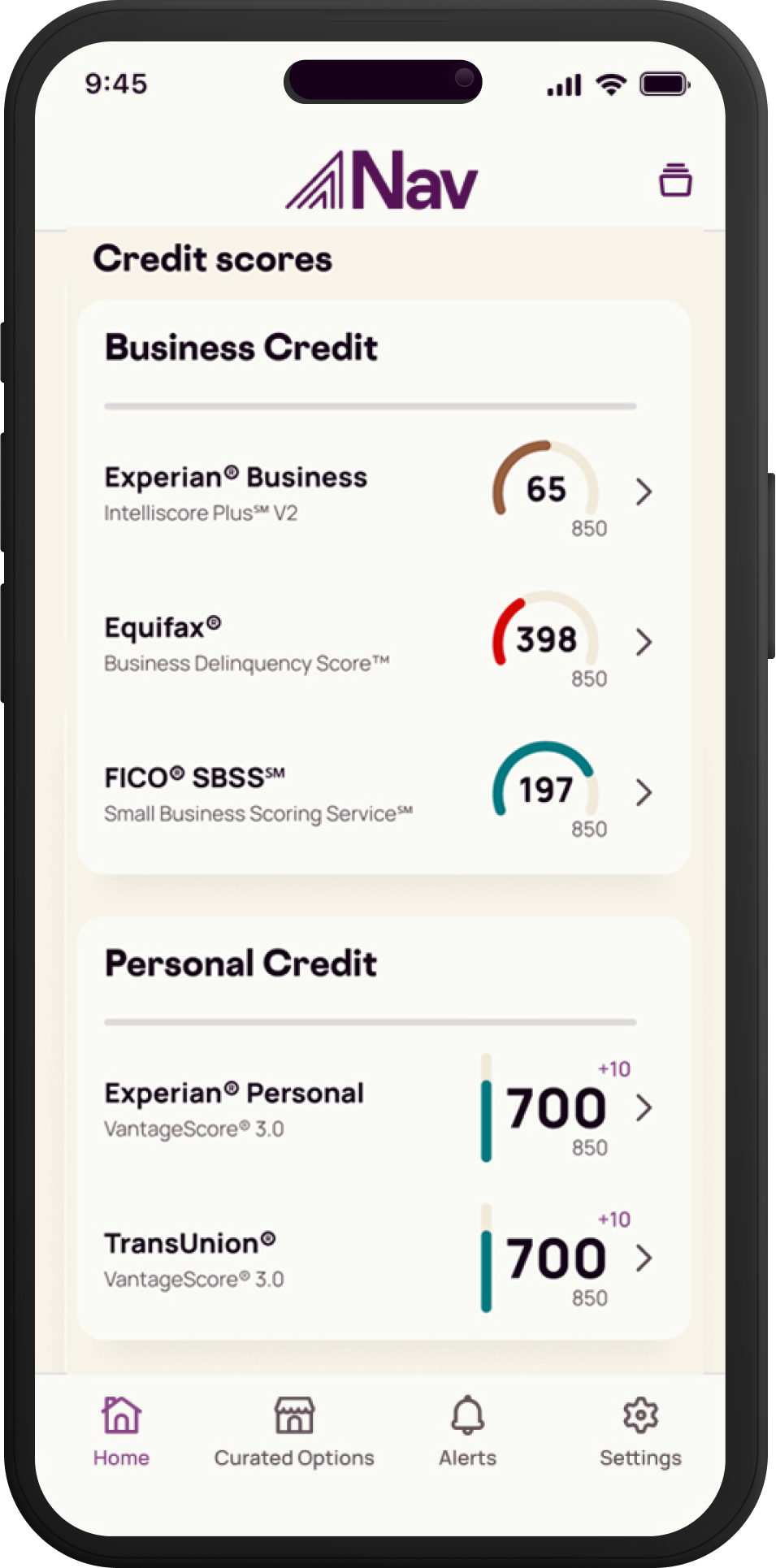

What Is the PAYDEX score?

The PAYDEX® score is a business credit score that’s generated by Dun and Bradstreet (D&B). Their model analyzes a business’ payment performance (i.e., if it pays its bills on time) and gives it a numerical score from 1 to 100, with 100 signifying a perfect payment history.

Just like a consumer’s creditworthiness hinges on a FICO score, a business’s creditworthiness is determined by a scoring system as well. Some lenders and vendors use this score for financial decisioning.

A business’s D&B PAYDEX score is used much like an individual’s FICO score. It helps lenders, vendors, and suppliers determine whether to approve your business for financing and on what terms. Typically, the better the score, the more generous the terms extended. This can save your business a lot of money and give you more time to pay for supplies or services, leveling out cash flow.

In order to establish a PAYDEX score, you’ll need a Dun & Bradstreet number, or a DUNS number.

What Is A Good PAYDEX Score?

The PAYDEX score ranges from 1 to 100. Maintaining a PAYDEX score of at least 75 shows lenders, vendors, and suppliers that you’re relatively low risk and likely to make repayments on time. A score below 75 may indicate you have a high risk of late payments, and a score below 40 is poor.

Read on for more on how scores are calculated and what each score range indicates about your ability to make payments.

How Is My PAYDEX Score Calculated?

To determine your business’s PAYDEX score, Dun & Bradstreet gathers data from the suppliers and vendors with which you do business over a rolling 12-month period. Each supplier/vendor is considered a business tradeline account, and the payments you make to that supplier/vendor is considered a payment experience. According to Dun & Bradstreet, two tradelines with at least three credit experiences are needed for a PAYDEX score.

Dun & Bradstreet analyzes the promptness of your payments against the terms of sale for each payment experience. So, the faster you pay your bills, the better your score.

PAYDEX scoring is dollar-weighted, which means that each payment experience is weighted in terms of the number of transactions and the overall dollar value of those transactions. That means your transactions with your IT vendor, with whom you spend thousands of dollars monthly, comprise a greater percentage of your D&B PAYDEX score than your transactions with the carpet cleaner who comes out to steam your rugs annually for a few hundred dollars, for example.

It’s important to note that a Dun & Bradstreet PAYDEX score of 100 does not indicate that a business has made on time payments — in fact, it indicates that a business has consistently paid suppliers 30 days in advance. Here’s a breakdown of what your Dun and Bradstreet number means:

How Is My PAYDEX Score Used?

PAYDEX is primarily used by some vendors and suppliers to judge your business when determining what terms to extend on trade credit (e.g., net 30, net 60, etc.) This is important because having more time to pay your bills can help you better manage cash flow.

Lenders and creditors may also consider your PAYDEX score before extending lines of credit or loans to your business. If your vendor or lender considers a PAYDEX score, aim to maintain a score of 75 or higher to ensure qualification for these types of financing.

How Can I Improve My D&B PAYDEX Score?

Since your PAYDEX score is based entirely on the promptness of your payments to vendors and suppliers, the only way to improve it is to make sure you are paying on time. Remember: paying on time will only earn you a score of 80. For a perfect PAYDEX score of 100, you need to pay early.

You should also make sure you have at least three open tradelines to generate a PAYDEX score on your business.

If you’re looking to establish or expand your current tradelines, Nav Prime can help. You’ll get two tradelines included in your Nav Prime membership — one with your monthly payment and another with the regular use of your built-in Nav Prime Card.

What Are the Best Lenders for Businesses With Strong Credit Scores?

Businesses with high credit scores are more likely to qualify for small business loans that require good business credit. You’ll find a few options to consider below. To instantly compare all your best options based on your business data, get started with Nav.

What Are the Best Lenders for Businesses With Lower Credit Scores?

For businesses with a low credit score, here are a few loan options to consider. Using Nav is the simplest way to instantly compare all your best options based on your credit score, annual revenue, and other business data.

These are designed for businesses that don’t have excellent business credit, and may request collateral in exchange for funding.

PAYDEX Scores Frequently Asked Questions

How do I establish business credit?

To establish business credit, first make sure your business is registered in your state. Next, obtain a D-U-N-S number by applying with Dun & Bradstreet or by establishing tradelines. Nav Prime can give you up to two tradelines. Once these steps are complete, start doing business with companies or organizations that report payment history to business credit agencies. Examples include vendors, suppliers, credit builder accounts, and business loan offers. You can also build business credit by getting business credit cards.

Now you’re ready to start building your credit profile. Meet payment terms and make payments on your open accounts on time. Make early payments if possible. Remember: Payment history is the single most important factor for building business credit. Timely payments will strengthen your score, while late payments can hurt it.

Nav Prime helps you actively build your business credit history with up to two tradelines.

How do I get a free business credit score report?

The best way to get free business credit summaries is to sign up for Nav. Nav is currently the only online platform that offers this, and it includes information from major commercial business credit bureaus. You also get personal credit score summaries, 24/7 business and personal credit alerts, cash flow alerts and insights, and one-on-ones with credit and lending specialists.

For a full credit score report that lenders see, you’ll want to get Nav Prime.

Do I need a PAYDEX score for my business in order to get a loan?

Some lenders check your business credit score during the business loan application process. Lenders in Nav’s ecosystem most consistently rely on Experian and Equifax when considering a business for funding.

This article was originally written on October 17, 2019 and updated on January 29, 2024.

Rate This Article

Have at it! We'd love to hear from you and encourage a lively discussion among our users. Please help us keep our site clean and protect yourself. Refrain from posting overtly promotional content, and avoid disclosing personal information such as bank account or phone numbers.

Reviews Disclosure: The responses below are not provided or commissioned by the credit card, financing and service companies that appear on this site. Responses have not been reviewed, approved or otherwise endorsed by the credit card, financing and service companies and it is not their responsibility to ensure all posts and/or questions are answered.

I am trying to apply for a Line of Credit for my small business (about 1 year old business). A lender said that they would need to take out a Trade Line / Revenue Purchase Agreement that I could immediately pay back, would spend a few thousand dollars in fees on the exchange. This successful loan and repayment would be reflected on my D&B score to raise my score and get it high enough for the Unsecured Line of Credit. Essentially this lender is asking me to pay a fee up front to unlock the Line of Credit. Is this real? Is it a scam? It feels like a scam but I’ve had several lenders offer it.

There are many vendors that report to D&B that don’t require you to spend thousands of dollars to build a tradeline (credit reference.) We’ve listed a number of them here. We can’t comment about that particular lender. In general, requiring you to spend a lot of money with the later promise of a loan can be a scam. You’ll find warnings in this article: How to Check if a Loan Company Is Legitimate

although I like Nav Prime, I’m disappointed that the Paydex score isn’t part of reporting.When I signed up for Nav Prime, I would see the Paydex, Equifax, and Experian business reports. especially with a business looking to do government contracts and work with a number of suppliers.

My D&B score just disappeared, I still see Equifax and Experian scores but no Paydex score. I pay for reporting from D&B, so I know my scores but I prefer seeing all scores on Nav as its more user-friendly imo. Has Nav discontinued reporting Paydex scores? If so, Id reconsider paying $50/month as I have many other Net-30 tradelines and can access to all my scores elsewhere for the subscription price.Thanks.

Nothing has changed in reporting to the three major business credit bureaus with Nav Prime. At this time, Nav has refocused your experience on the scores our lenders use most for funding decisions. Through our partnerships with 75+ lenders, we’ve collected feedback that Experian and Equifax business credit data is reviewed most regularly.

Do the Nav Prime credit card report back to Dun & Bradstreet?

Yes. Build business credit history with up to two tradelines with Nav Prime, where your Nav Prime payments and Nav Prime Card payments are automatically sent to all major business credit bureaus.

Great insight regarding building my Paydex Score and Business Credit Profile. Very informative!

i don’t understand what you are doing to my business credit. I have no loans for business or lenders or business credit card so why are you hurting my credit by giving me a d and caution on this report?

Are you talking about your Nav account? Nav is not a credit bureau – the information you see is coming from a major commercial credit bureau. Low grades are often due to a lack of accounts reporting. Feel free to reach out to Nav customer support for questions about your Nav account: support@nav.com.

I subscribed to NAV April 28 20222 and it is now July 20222….I see no paydex score increase.

Is their a reason for that?

Antonio – Can you please reach out to Nav customer support so they can review your account? support@nav.com.

I was wondering, does Nav still offer the free DnB reports anymore? I see Experian Business and Equifax Business but I do not see DnB anymore. Am I correct to assume Dun & Bradstreet is not offered as an option with Nav any longer?

At this time, Nav has refocused your experience on the scores Nav’s lenders use most for funding decisions. Through our partnerships with 70+ lenders, we’ve collected feedback that Experian and Equifax business credit data is reviewed most regularly.

I pay for all my parts upfront. So there is no one to pay late. I do not owe anyone. SO why is the score so low.

If there is no negative information on the credit report then a low credit score is typically due to few accounts reporting. This is not at all uncommon with business credit as not all lenders and vendors report.

I have trade lines that’s 30 net and I have paid for and still don’t have a paydex score

It’s hard for me to know what’s going on without more details. If you have a Nav account feel free to reach out to customer support. Otherwise, I’d suggest reaching out to D&B directly.

What does the letters means on my nav account? I have a B. when will I start to see numbers?

Georgia – You are always welcome to reach out to Nav’s customer support team with questions about your Nav account: support@nav.com. In the meantime, a score that’s a B is good but there may be some room for improvement. You will see full reports and scores if you have a paid Nav account.

I can’t view my score, I tried to signup for the free 14 day trial but it keep tryin to sign me into getting a Duns number & I already have one. Why can’t I view my score?

If this is a question about your Nav account please reach out to our customer support team: support@nav.com.

If you are trying to sign up at the D&B site please reach out to them.

How do I find out who I owe so I can get my payday score back to 89

Business credit bureaus aren’t required to list the names of companies that report unfortunately. You may want to reach out directly to D&B for more information.

I am extremely confused about my trades. The only trade lines I have is quill and u line. I don’t have any other tradelines well except for NAV. SO MY REPORT IS WRONG. I don’t who it is. Isthere anybody that can help me

If you have a Nav account, please reach out to Nav’s customer support team: support@nav.com. If not you’ll need to reach out directly to D&B.

I’ve never made a late payment, so why is my score a B ..

When there is no negative information on the business credit report, a lower score is usually due to few accounts reporting or possibly high utilization.

Should not go from a B to an F

Just got my first D&B score on NAV and it shows a grade A. So what does that mean as far as a Paydex score?

The letter grades in your free Nav account do not correspond directly to credit score ranges. One way to think about it is this: if your grade is less than an A there are probably ways to improve. Many business owners have few accounts appearing on their business credit reports. When that’s the case, adding additional references that report – and paying on time – will often be helpful.

My pared shows a grade of A but I don’t see any actual score? Please help me understand this. Thank you.

The letter grades in your free Nav account do not correspond directly to credit score ranges. One way to think about it is this: if your grade is less than an A there are probably ways to improve. Many business owners have few accounts appearing on their business credit reports. When that’s the case, adding additional references that report – and paying on time – will often be helpful.

Why is my score a “C”? I owe no one have very little debt and never miss a payment on anything.

Darren – In most cases when a business has a lower score but no negative information it’s usually due to very few references reporting.

I have a balance on an account that I have no idea who it is. I don’t owe anyone

Is it possible that you use an account you pay in full with a vendor or supplier for example? If so, the balance may be reported before you pay the invoice. If that still doesn’t make sense to you, you can contact Dun & Bradstreet for assistance. (I assume this on your D&B credit report.)

Same here. There is an account that shows I owe $250 to someone that I have no idea who it is and it’s affecting my score. All of my accounts have a zero balance.

Excellent Advise

I have a account. Need to know the name of the company

Business credit reports don’t typically list the name of the companies that report.

how can i see what tradelines I have open?

Business credit reports don’t typically include the name of vendors or companies reporting unfortunately.

How do you dispute incorect information without knowing the name of the business?

You can still file a dispute using the available information and the credit reporting agency will then contact the furnisher.

Why did my score go from a A to a B ?

Olivia – Unfortunately there’s no way we can predict why your credit score changed. You may want to review your detailed credit report to see if you can identify changes.

How do i find my creditor on my Paydex report?

Most business credit reports do not list the names of creditors or vendors unfortunately, and there is no requirement that they do so.

I am disputing my Score. I don’t gVe any past due accounts.

Tammy – We can’t process disputes through the blog. If this is a dispute with D&B you’ll need to reach out to them directly.

I don not understand what company my company owes.

I’m sorry I am not sure I understand your question. Are you reviewing your Dun & Bradstreet credit report and have questions about creditors listed? If you use Nav to check your credit, please contact customer support with questions: support@nav.com.

My PayDex Score is inaccurate. How can I request changes/updates?

If you believe your Dun & Bradstreet credit report contains inaccurate information you may dispute it here.

Is having a NAV business boost account considered a tradeline that will report to D&B?

Yes, paid Nav accounts at the Business Loan Booster and Business Loan Builder levels report. You can learn more here.

Hello, my paydex score dropped from a 85 to a 65 and I paid everything on time, and it doesn’t tell me what’s delinquent, how can I find this out?

Alanna – If you have a Nav account feel free to reach out to customer service. Otherwise you’ll need to contact D&B. Please note that business credit reports typically don’t list the names of creditors.

I would like to know when my trade line going to start reporting show my factor business Score I don’t see anything on my business credit report.

It typically takes anywhere from one to three full billing cycles for accounts to be reported.

How do I find out the trade line number 2 on my report because it says I owe $500, and I know I don’t. I don’t know who to contact thanks

Jeanine the only way to get help with this is to contact the credit bureau directly.

how come my paydex says 50 and i have never missed a payment and i always pay everything way before the due date like 2 weeks before due date..

It’s impossible for me to tell Brian. If you have a Nav account, I’d suggest you reach out to our customer support team to see if they have any insights: support@nav.com.

Why is my score showing a C ive never missed or have been late on a payment? And what acct is my report referring to? It shows from Dun & brad, are they trying to ruin me before I can get started?

Dee dee – It’s very common for businesses not to have high scores, not because there is negative information, but because there is not enough information to provide a high score (which means lower risk). If there is nothing negative information on your credit reports, I suggest you consider building business credit references.

My Trade lines are not reflecting on my business profile And it’s holding me back From proceeding with other ventures?

Mr. Lee – Perhaps this article or this article will help.

Mine says A as in the letter A and not a number

Yes with a free Nav account it shows a letter grade. Congrats on the A! That’s terrific.

Thanks for the information. It is very informative.

Nav says my Paydex scorre is “good” but the number quoted is 14. Which one is right?!

Caroline – please reach out to our customer support team for help: support@nav.com.

Hi, So if I have a Paydex Score of 80, Is that good enough to start applying for a Business Credit Card? or Should I keep working on Net 30 accounts?

Most business credit cards (at least the ones from major issuers) use personal credit to make the decision. Do you have a Nav account? If so you may want to look at your matches in your account.

Hello,

I have a Paydex Score of 14 but I pay my business credit card on time and my balance for that business credit card is $0. Why is my score so low?

Without seeing your reports it’s hard to tell but usually it’s due to lack of reporting. That particular score is heavily based on trade credit so you may want to establish tradelines that report. You’ll find more information here.

I don’t understand why my score went down since I’m current with accounts.

How do I get a refresh to acct I have been paying my accts on time and early even have the nav boost and I’m still not showing paydex score it has been over 30 plus days.

Please reach out to Nav’s customer support team for help: support@nav.com.

I am currently helping a friend build business credit for the past 6mths. I too started 6mths. I only have 3 tradelines and within 3months I received and Paydex/Dun & Brad score. My friend has 6 active tradlines however the Paydex score have not generated… At this point I am clueless. I don’t want them to have to pay to self report to Dun & Brad. Any suggestions beside contacting D&B because they are pushing the credit signal. BTW they have Nav booster

If they have a Nav account I’d suggest you have them reach out to Nav’s customer support team to see if they can figure out why it’s not generating. (I assume they have a paid Nav account to build credit…?)

How do I find out who put a negative payment history on my D&B so I can get it cleared up, Thanks

You will need to contact Dun & Bradstreet to file a dispute.

Am still wondering why Dun and Brad Paydex still reporting my company as F , high risk when we don’t own anyone, both our rental and utilities bills are paid on time and before due dates , it’s really not fair

Typically if your business credit scores are low but there isn’t any negative information it’s due to a lack of accounts reporting. Without account information showing how you’ve paid your bills in the past it’s hard for scores to predict how you’ll pay in the future. You may want to download our free Build Business Credit Checklist for suggestions on how to build business credit.

Why is there nothing reported from my account?

I’m not sure what specifically you’re asking about when you say nothing is reported. If you mean your Nav account, please contact our customer service department: support@nav.com. If you are generally saying that you don’t have any accounts being reported on your business credit then you may want to download our Build Business Credit Checklist.

There is a phantom balance on my account with zero details as how this happened.

I purchase the Nav boost to have it report, I had it for 3 months & it hasn’t reported once. I need a refund, please, Because the only reason for me setting it up was for it to report to D&B

Camella – Please contact Nav’s customer support team for help. You can reach them at support@nav.com.

My biggest mistake I made with truebuild and nav

My business address is not showing correctly after I have attempted to update it

If you have a Nav account please reach out to customer service for dispute instructions. (Just please keep in mind that ultimately, though, Dun & Bradstreet will need to correct it as Nav can’t update your D&B report.)

I have bad credit account on my paydex but it does not belong to my business. How can I remove it?

Paul – Do you have a Nav account? If so our customer service team will provide you information on how to dispute it.

My credit score is very low and I don’t know what business is will open up me account can someone introduce me to what business take a low score using my duns and brad number.

If you don’t have good personal credit then your business will likely need strong revenues in order to qualify for financing.

This does not explain the Ratings as showing in alphabetical list. It reference to a number scale of 1-100, however my rating is by letter form. So, I still do not understand if I am in good standings or poor standings.

My Dnb paused score has been 80 for quite some time. I have always paid early. My goal is 100, how soon should I pay invoices in order to reach that?

80 is excellent. I am not sure what incremental gain you would get at 100. Also D&B doesn’t reveal the details of the scoring formula. So my best suggestion is to just keep on doing what you’re doing and focus on growing your business!

I have a negative account on my business credit report that’s not accurate. I dont owe anyone any money. How do I remove this

That is a good advice as the difference between an 80 PAYDEX score and one of 100 is only that the company that is rated 100 is paying too soon . An 80 is in fact closer to perfect in some ways has it indicates perfect terms. A PAYDEX score of 100 means you are paying sooner than the contractual agreement outlines leaving interest that could be calculated and kept in reserves instead of paying too early ….It is a tricky game!

Regardless ,I think Dunn &Bradstreet are in fact really fantastic to deal with.But as any new business it is hard for some to get a rating.

Edward HC Graydon

Graydon Investments Group LTD

Actually, a Paydex score of 80 simply means that, on a dollar-weighted average, a business consistently pays their bills within terms, whether those terms are Net10, Net30, etc. To achieve a Paydex score above an 80, a company’s suppliers are reporting that they offer discounted terms, such as 2%10Net30, and that the business often/always takes advantage of that offering. Most suppliers offer those terms only to their “best” customers, or to customers who are dealing in high dollar invoices that the supplier would prefer not to carry over a full 30 days.

So, yes, there is an incremental benefit to having a Paydex score over 80. It signifies a level of creditor>customer trust, consistency and reliability. It should be noted, though, that in my 5 years of working at D&B and 8 years of using their products to expand my client’s corporate credit, I can tell you that the highest Paydex score I have ever seen was an 87, and that was due to a million-plus invoice being paid on discounted terms.

MY ADVICE: If you want to be of value to your vendors and suppliers (and keep your Paydex score in tip-top shape) mail your payment 10 days before the due date or make your online payment 3 days before the due date. That way, when the supplier’s computer links to D&B’s computer, it will only have nice things to say about your business!

Soon every score will be a 50 Paydex rating as this economy is going down fast .Until the economy lifts the restrictions on masks and allow’s for free will the economy of North America as a whole is going to take a wicked hit. The trend is not your friend.

For public record given the subject I will now disclose that Graydon Investments Group LTD hold no debt in any way. We do not owe have leans or judgments . The corporation on title with Dunn and Bradstreet hold a paydex rating of 80 based on next to no trades

Edward HC Graydon

Graydon investments group Ltd

Regardless of credit bureau business or otherwise the bureau’s most show accurate if not precise payment history as it is being reported”it is the law” and at this time in history it seems unlikely many people or corporations where not effected by the lockdown to some degree ? Because capitalism was within reason shut down for months at least at the retail and governmental level it seems more likely people did not pay their invoices and credit card statements on time. Along with corporate returns!

When I think about the debt loads that where being held by corporations and individuals before the last part of 2019… I think in reality it will be difficult if not impossible to achieve an 80 paydex rating over the next few years .If the banks and creditors enter into the system the reality of life during the lockdowns and what truly transpired I think it will show. That will be the testing period where the lending industry must look the other way and turn the other cheek to slow payments ,or the credit market ceases up far worse than 2008.

Edward HC Graydon

Graydon Investments Group LTD

Please i am doing a research on Paydex Score. Does the trade reference in this case include lenders. Does bad loan repayment of a business affect thier paydex score.

If you’re talking about a traditional lender like a bank it likely does not impact the Paydex score.

None of my Business Payments have been payed past their due date. They are paid either before receiving an invoice or immediately after receiving an invoice.

My business score should be greater than a B. I have paid all my business accounts either off and on time. Please assist me in getting a higher score.

Shedrick – Since credit scoring models are proprietary it’s impossible to say exactly why your score is exactly what it is. Often when business owners are paying their bills on time the problem isn’t negative information; it’s the number of accounts reporting and payment history. It may be helpful to establish an additional credit reference that reports. Feel free to reach out to Nav’s Customer Support team if you have questions.

How can I see how many trade lines I currently have and with whom?

If those accounts report to business credit, you can see them by viewing your business credit reports. You can view D&B, Experian and Equifax commercial credit reports through Nav with a Nav account (free or paid). However, business credit reports do not list the names of companies that report so you have to figure that out based on when the account was opened, the balance, credit limit etc. That’s not a Nav policy – it’s the credit bureaus policy.

Trying to figure out why I’m at an F? Is it because I haven’t been ordering anything?

It’s hard to tell Chanda without looking at your report. If you are a Nav customer, try reaching out to customer support to see if they can spot something.

Is the score shown by a letter or a number or both. I have a nav account and it says B. I am new to this business credit score. Where can I see the numeric score as well? I have a Nav and a DUNS account..

On a free account it is a letter grade. A paid Nav account shows the numeric score.

I have no business and thing beside a trailer and never have I been late it’s on auto pay

This is bs and tainting me for when if I actually need to have credit.

My capital one has never been late or not paid in full every month

I’m not sure what issue you are experiencing. My guess is your D&B Paydex is low? That may be due to lack of information not negative information FYI. Similar to personal credit scores, business credit scores may be low if there isn’t much information reporting.

Like to know why my score went from a A to a B… ALL of my bills are paid in advance.

Bill – I don’t know. If you are a Nav customer I suggest you reach out to our customer support team for more assistance.

My score should be much higher. At least a B or A because i always pay my bills on time.

John – feel free to reach out to our customer support team: support@nav.com.

I see (my company) had a poor rating all this company need is a chance . I don’t have credit.

Ms. Williams – it is not uncommon to see companies with low business credit scores, not because of negative information, but because they don’t have much in the way of credit accounts reporting. If that’s your situation, you can likely see results simply by adding a few credit accounts and paying them on time. Vendor accounts can be a great way to start. We also have some videos about building credit on the Nav Youtube channel which you may find helpful.

The only thing I have attached to my business is our cell phone account. Which is on autopay. Other than that I have no business credit. Why is my score so low saying I’m more than 60 days behind, which clearly I’m not. I’ve never even paid that $1,500 to start getting credit with D&B.

LaTanya – If Dun & Bradstreet is reporting incorrect information about your payment history you’ll need to reach out to them to dispute it. You can start with their iupdate service.

We ALWAYS pay before or on time! NEVER late! Why is our grade a C???

This is ridiculous.

Usually if it’s not due to negative information it’s due to lack of credit references. Could that be the case for you?

When I established my business credit card with navy fed I didn’t not have a DUNS number yet. It’s been almost one year of having a Navy Federal business account AND business credit card. How to I get my credit account history attached to my DUNS number?

You’ll need to talk with Navy Federal. Find out if they report positive payment history to Dun & Bradstreet (many issuers don’t), and if they do, whether they are reporting it for your card. Keep in mind they could report through SBFE which would not show up on a credit report you are monitoring.

Call DnB and they will link it for you

Is it possible for tradelines to be reported to Equifax business but for them to not reflect in Nav. I have a company telling me to purchase my business credit report from Equifax directly because the information in Nav is not accurate. Currently I’m paying 39.99 a month to Nav to see my business credit reports.

Brandon – Will you reach out to our customer support team? They will be able to see what’s going on with your business credit report.

My company don’t have debt, I don’t have capital or gain not sponsor. I don’t understand “how dunn and Bradstreet can give my company a grade?” I can’t get business credit.

You have to establish a business credit profile in order to get business credit.

How do i get my duns #

Can you steer me in the right direction

It’s easy Stephen. If you have a Nav account, you can do it there (customer service can always help if you’re having trouble). Otherwise you can go to Dun & Bradstreet’s website to apply.

Is paydex Equifax? I’ve seen my business Experien score, but I haven’t seen the business equifax number. Even after trying to search for it.

Paydex is produced by Dun & Bradstreet. Equifax has a variety of scores. The one we display at Nav is the Delinquency Risk Score.

The D&B report being used is not mine

It is for Rich’s Custom Motorcycle seats and upholstery!!!

My company is 1 Fine Auto DBA Rich’s Custom Upholstery

It would be nice for you to get this correct PLEASE!!

Thank You

Moe

Please feel free to call with any questions you may have.

Maurice – If you have a Nav account feel free to contact our customer service department and they will help you with the dispute. If not, you will need to reach out to Dun & Bradstreet directly to file your dispute. (We’re not the credit bureau so we can’t correct it for you unfortunately.)

Who actually uses D and B scores on the other end? I see a lot vaguely that ‘vendors suppliers and creditors’ might use it. But is it common? Anyone know any data on that? What about potential landlords? Or how much does it cost for vendors to get the report?

I am a restaurant – do I really need to monitor this or is it pretty obscure / just for larger businesses?

D&B has been around since the 1800s and their business is selling commercial credit reports and scores. So there is definitely a market for what they sell. However there’s no requirement they tell you who has obtained your credit report and they don’t reveal their proprietary sales information. Yes, we know business owners who have been impacted by information in their business credit reports but whether it will impact you and your business is hard to say.

My dun&Bradstreet report is inaccurate considering my payments with the few Tradewinds I do have are promptly made within 30 days. Im extremely upset with this inaccurate reporting. I need for this to be corrected immediately!

Yvonne Blankenship

Yvonne Mobile Notary Services, Owner

Yvonne – We are not the credit bureau so we can’t correct it for you. If you are a Nav customer, feel free to reach out to customer service for more information on how to file a dispute with D&B. If you are not a Nav customer you’ll need to reach out to them directly.

I just received my D&B number and my Paydex is showing poor. Could that be because I have no tradelines?

Yes that could be the case. You may want to check out this resource: 3 Vendors That Will Help You Build Business Credit

I want the vendors too

I got a Duns # and ein# an I’m using my business address as my home address an my home phone as business phone. I have a quill acct a nav acct an crown office an supply acct dun brad street credit builder acct an im going to open a well fargo bussiness acct these trade lines were open like 03\15\2021 all most a month. Can you see what else i need to do?

It sounds to me like you are on the right track Annie. You may want to consider a business credit card if you qualify.

I pay my Bill’s on time or ahead of time every month!!! I want to know who I can contact to dispute this!!

Pam – for disputes to your Dun & Bradstreet credit report you’ll want to contact D&B directly. They offer an online service called iupdate for disputes.

How do I find more net 30 companies and some net 60 and net 90 companies

It’s harder than you think to identify those because business credit reports don’t list the names of companies that report. A lot of information we’ve seen has been outdated. We will continue to look for additional companies to add to this list.

I have 6 commercial loans on my business since 2018. I have been making timely monthly payments on them but they do not appear on any of the business credit reports. What should I do to include them on the report?

Reporting is voluntary, so if they don’t report you’ll need to get ones that do. It’s also possible they report to other bureaus. Have you checked your other credit reports – Equifax and Experian – through Nav?

They give me a c well lmao been in business over 30 years never been late that I can remember this is a joke !!!!! Do not recommend … have not advertised for work in yrs and they give me a c ??? Information they say about u not true always pay 3,4,5,6 time times the amount due

Howard Seabrook SAME HERE! I have been in business over 12 years, pay all invoices when due or before, all my business is word of mouth and like you have not advertised in years, to the point that I was going to close down all my web and social media sites. I log on to look at my business credit and it a C. Something is really fishy here. How can I tell who and who isnt reporting on my business credit. I can see who is reporting on my personal credit, why can’t I see the same thing on my business credit?

Your question about who is reporting is a valid one. It’s been a tradition for business credit reports not to list the names of companies that report and instead to categorize them only by type of account/industry. The explanation I’ve heard is that because anyone can purchase a business credit report, they are reluctant to make that information available because creditors may use it to try to steal their customers.

You’re right that business and personal credit are very different. One of the main things to understand is there are no regulations covering business credit reporting and each bureau has different practices and policies.

Keep in mind a score range that falls into “C” can be the result of few companies reporting rather than negative information. Credit reporting is voluntary and not all companies report, or not all report to all major commercial credit reporting agencies.

I enrolled the business in the credit builder plus plan. Love it and I have learned a lot. In the last two weeks we got 2 new net 30 tradelines and a business cc that reports to all business bureaus. Paid the new net 30s day after receiving the invoices. First business cc statement closed 5% utilization. We had 2 small tradelines already reported on dun & brad with ppt. When the new credit is reported, will the paydex score be weak because they are new?

Thanks,

ACE

It will take some time to build a strong score but overall it seems to happen more quickly than with consumer credit scores – especially when proactive as you are!

i pay my bills early so why is my grade a c it is never late please recheck with the company and fix my grade please

Lynette,

We translate the score the bureaus provided into a letter grade in our free account. We also update monthly. If your score isn’t strong but you’re paying your bills on time it may be that you don’t have enough accounts reporting. Feel free to reach out to our customer support team if you have more questions.

I pay my bills on time. This company is a scam. They purposely give you a low score to encourage you to sign up and pay outrages fees. Shame on them.

Bradley,

One of the things we’ve noticed at Nav is that many business owners have low scores because they have few accounts reporting. It’s not uncommon for business lenders and vendors not to report to all bureaus (or sometimes not at all.) You may want to check out this article for some suggestions: Easy Approval Net-30 Accounts And of course you can monitor your D&B data at no cost with a free Nav account.

How do I get in touch with someone to fix a negative on my business report. It’s false I don’t owe any money to anyone. I need this removed

Did you view your D&B report through Nav? If so then please reach out to our customer support team support@nav.com. If not, you’ll need to reach out directly to D&B.

I’ve been paying my accounts early and in advance but Paydex is still 76.

That’s not a bad score by any means James. How many accounts do you have reporting?

My paydex score is wrong. I pay my bill on time or early! Not sure where your getting your information. Please make sure you have the correct info before posting and giving a 47 year old company a bad score because they don’t want to use your premium service!

What numerical score is assigned to Nav’s ‘A’ Paydex rating?

The score range for “A” is 80 – 100.

Valuable information when needed nav thanks for your input.

Were it states that Equisure pays late and not according to terms is incorrect and needs to be changed, we have never been late to pay and most of the time early.

Scott,

I’m not sure what report you are looking at. Did you see this in your Nav account? If so feel free to reach out to our customer support team. Their contact info is in your Nav account. If you don’t have a Nav account you will need to reach out directly to Dun & Bradstreet to dispute it.

This information came in extremely handy and was very much appreciated thank you

Thanks for letting us know. We’re glad it helped!

I pay my bills within terms.

Why is it that my paydex is poor upon opening the credit, is this essentially a form on no credit?

I’m not sure I fully understand your question John, but if I do you’re asking whether the fact that you don’t have a credit history with D&B could result in a low score. Is that correct? If so the answer is yes. Barring any negative information on your credit reports, your next step is likely to build positive business credit references that report.

good day, i am new to building credit, anyway i have a few accounts am working with. my main concern is how to understand my credit report. I saw on (A) on my DUNS ACCOUNT not sure if thats good are bad, also how to know how much is your paydex score.

How do you view accounts to find out what is getting reported late?

Same question here. How do you know what vendors are reporting?

John and Linda –

Business credit reports don’t list the name of the creditor so you have to be a little bit of a detective and try to match other factors – such as a recent credit limit – to the information in your report. If you have a Nav account and continue to have trouble understanding it, feel free to reach out to our customer support team and they will do their best to help you understand it.

Also note that when you first start establishing business credit, it can take 30 – 60 days (or more) for accounts to start reporting.

If you’re looking for information on which companies will help you build business credit, you’ll find that in the BusinessLauncher section of your Nav account.

In addition, the following articles may be helpful:

Which small Business Credit Cards Report to Business Credit

3 Vendors That Will Help You Build Business Credit

Makes no sense. I ordered from Quill. Rec’s notice order was rec’d. Sent cc payment 4 days later, and D&B marked as paid day of purchase. I called Quill and they told me to wait at least 14days before paying.

Quill reports all payments 1st business day monthly unless holiday.

D & B agent told me ” their ( D & B ) mistakes can not be corrected until new info from vender. Then she pushed VERY hard to get me to sign up for $8,000.00 Credit Congierge Program I told them no.

No wonder companies have so hard a time getting anywhere.

Thanks for sharing your experience. To clarify – were you reported late?

Thanks for contacting me…My business is a startup…does PAYDEX work

with Startup businesses?

You can start to build business credit as a start up. The sooner you start building business credit, the better.

I’m not late on any of my bills

This is crazy my score with Dunn & Bradstreet is a F. I have been in business for 45 years nd never late on a payment. Hmmmmm just saying

Are you sure the information in your report is correct Joe?

The address for my dun and Bradstreet information is incorrect,

Not cremation business in Whittier ,California

Brian,

If you have a Nav account you can go into your account and reach out to customer service. They will help you understand how to dispute. If you don’t, you’ll have to contact D&B directly.

This is an educational article and we can’t correct your D&B report for you, unfortunately.

I am having a hard time getting D&B to show me how to report my business clients paid off loans. Do you have any tips on what particular department or phone number on who will help me.

It seems every time I get on the phone there I get a sales person pushing Credit Builder and I never get a call back on the info I’m askig for.

Did you see the article that we published on that topic? How to Report to Business Credit Bureaus Let me know if that helps at all.

Thank You for the insight to the Paydex Score and Scoring strategies.

A viable follow up article would be to post National Stores that automatically report trade lines i.e. Retail Chains, Financial Insitutions.to assist startups in maximizing efficiency and opportunities.

Daren –

We provide information on how to build business credit, including companies that report, in our free BusinessLauncher tool. It is included with all Nav accounts, including our free accounts.

In addition, the following articles may be helpful:

3 Vendors That Will Help You Build Business Credit

Which small Business Credit Cards Report to Business Credit

Would a CFPB & OCC Complaint against Wells Fargo for a mislaid commercial acct with accompanying safe deposit box cause a dormant Paydex Score?

I can’t imagine it would be reported.

My paydex is bogus, D&B knows it.

Dunn and Bradstreet does not report accurately. My business has paid back over $1mm in debt, and pays creditors early as part of tax planning. Yet they report my business pays one day late. Unless you pay them money they jack around with their “credit score”. Which means those with A credit paid for the rating. How accurate can that be?

I agree it’s ridiculous to be penalized for paying your bills on time. But we understand it’s the system ratings they use.

umm, you’re not penalized for paying your bills on time. You’re given more credit for paying before the agreed time.

If you negotiate terms and you fulfill the terms then why are you penalized for doing that? To only receive an 80 for doing what you agreed on is a ridiculous way to score this thing.

It certainly is different than what we are used to with personal credit.

How do i see who’s reporting on my business credit

Business credit bureaus don’t typically reveal that and there are no laws requiring they do so.